Bank of America 2001 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

|

|

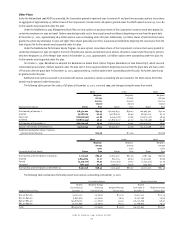

Net periodic pension benefit cost (income) for the years ended December 31, 2001, 2000 and 1999, included the following components:

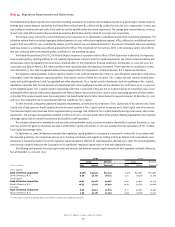

Qualified Pension Plan Nonqualified Pension Plan

(Dollars in millions)

2001 2000 1999 2001 2000 1999

Components of net periodic pension benefit cost (income)

Service cost $ 202 $ 153 $ 115 $22 $10 $ 9

Interest cost 560 519 433 40 39 33

Expected return on plan assets (876) (813) (713) –––

Amortization of transition obligation (asset) (2) (4) (4) –11

Amortization of prior service cost 54 38 20 11 10 7

Recognized net actuarial loss –_– 798

Recognized gain due to settlements and curtailments –(11) – 6––

Net periodic pension benefit cost (income) $ (62) $ (118) $(149) $86 $69 $58

For the years ended December 31, 2001, 2000 and 1999, net periodic postretirement benefit cost included the following components:

(Dollars in millions)

2001 2000 1999

Components of net periodic postretirement benefit cost (income)

Service cost $11 $11 $12

Interest cost 65 58 58

Expected return on plan assets (21) (20) (19)

Amortization of transition obligation 32 37 34

Amortization of prior service cost (credit) 4(3) –

Recognized net actuarial loss (gain) 20 (45) (54)

Recognized loss due to settlements and curtailments –20 –

Net periodic postretirement benefit cost $ 111 $58 $ 31

Net periodic postretirement health and life expense was determined using the “projected unit credit” actuarial method. Gains and losses for all benefits

except postretirement health care are recognized in accordance with the minimum amortization provisions of the applicable accounting standards.

For the postretirement health care plans, 50 percent of the unrecognized gain or loss at the beginning of the fiscal year (or at subsequent remeasurement)

is recognized on a level basis during the year.

Assumed health care cost trend rates affect the postretirement benefit obligation and benefit cost reported for the health care plan. The assumed

health care cost trend rates used to measure the expected cost of benefits covered by the postretirement health care plans was 8.0 percent for 2002,

reducing in steps to 4.5 percent in 2006 and later years. A one percentage point increase in assumed health care cost trend rates would have increased

the service and interest costs and the benefit obligation by $6 million and $52 million, respectively, in 2001, $9 million and $49 million, respectively,

in 2000 and $7 million and $62 million, respectively, in 1999. A one percentage point decrease in assumed health care cost trend rates would have

lowered the service and interest costs and the benefit obligation by $4 million and $45 million, respectively, in 2001, $7 million and $40 million,

respectively, in 2000 and $6 million and $56 million, respectively, in 1999.

Defined Contribution Plans

The Corporation maintains a qualified defined contribution retirement plan and certain nonqualified defined contribution retirement plans. There are

two components of the qualified defined contribution retirement plan: an ESOP and a profit-sharing plan. Prior to 2001, the ESOP component of the

qualified defined contribution retirement plan featured leveraged ESOP provisions. The profit-sharing component allows participants to modify exist-

ing investment allocations on a daily basis. See Note Thirteen for additional information on the ESOP provisions.

Effective June 30, 2000, the BankAmerica 401(k) Investment Plan was merged with and into the Bank of America 401(k) Plan (401(k) Plan). During 2000,

the Corporation offered former BankAmerica plan participants a one-time opportunity to transfer certain assets from the 401(k) Plan to the Pension Plan.

The Corporation contributed approximately $196 million, $163 million, and $191 million for 2001, 2000, and 1999, respectively, in cash and stock

which was utilized primarily to purchase the Corporation’s common stock under the terms of these plans. At December 31, 2001 and 2000, an

aggregate of 45,468,591 shares and 46,010,493 shares, respectively, of the Corporation’s common stock and 1,506,553 shares and 1,684,053 shares,

respectively, of ESOP preferred stock were held by the Corporation’s various savings and profit sharing plans.

Under the terms of the ESOP Preferred Stock provision, payments to the plan for dividends on the ESOP Preferred Stock were $5 million, $6 million,

and $3 million, for 2001, 2000, and 1999, respectively. Payments to the plan for dividends on the ESOP Common Stock were $27 million, $22 million,

and $21 million during the same periods. Interest incurred to service the debt of the ESOP Preferred Stock and ESOP Common Stock amounted to

$0.3 million, $3 million and $5 million for 2001, 2000 and 1999, respectively. As of December 31, 2001, all principal and interest associated with the

debt of the ESOP Preferred Stock and ESOP Common Stock have been repaid.

In addition, certain non-U.S. employees within the Corporation are covered under defined contribution pension plans that are separately administered

in accordance with local laws.

BANK OF AMERICA 2001 ANNUAL REPORT

109