Bank of America 2001 Annual Report Download - page 3

Download and view the complete annual report

Please find page 3 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

1

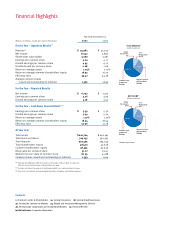

In 2001, your company achieved solid financial results

despite a weak economic environment and took major

steps to accelerate internal growth, improve business

execution and focus activities ever more tightly on the

needs of our customers.

>

Associates accelerated work to attract, retain and

deepen customer relationships and to improve customer and

client service throughout the company.

>

We launched a company-wide Six Sigma

quality and productivity program and continued

to reinvest savings in high-growth opportunities.

>

We installed a new business planning

process and a new approach to risk management

that we believe will bring consistency and pre-

dictability to our earnings.

>

We hired teammates from different indus-

tries who brought new skills to our company.

>

We adopted shareholder value added (SVA)

as a measurement tool to bring more financial

discipline to our business decisions.

>

We continued to invest aggressively in

efforts to build the Bank of America brand.

In short, we are combining our heritage of

ingenuity with an emerging culture based on

focus and discipline, consistent execution and

sustained intensity to serve customers better

while at the same time producing strong growth in total

shareholder returns.

Building Momentum.

Our associates’ hard work in

2001 paid off, as revenue increased 5% to $35 billion,

leading to an operating earnings increase of 2% to $8

billion, both impressive figures taking into account rising

credit costs and the faltering economy. The lion’s share of

earnings growth came from Consumer and

Commercial

Banking, which posted earnings of $4.8 billion, up 6.4%

from 2000, driven mostly by gains in net interest income,

service charges, card services and mortgage banking.

Global Corporate and Investment Banking earnings rose

6.8% to $1.9 billion, reflecting an increase in fixed-income

originations and increased market share in every major

category of capital-raising transactions. Turmoil in the

markets dampened results in the Asset Management Group,

which held revenues steady, but saw earnings fall 11.5%

to $521 million due to increased investments in the busi-

ness. Equity Investments recorded a loss of $94 million.

While our core businesses performed well, we made a

strategic decision in the third quarter to exit the

subprime real estate and auto leasing busi-

nesses, both of which tended to produce volatile

earnings and did not fit our objectives for prof-

itability. We took a $1.3 billion after-tax charge

to cover the costs of exiting these businesses.

Credit costs continued to be our greatest

drag on earnings. N

et charge-offs, excluding

charge-offs related to the exit of the subprime

lending business, totaled $3.6 billion, or .99%

of loans and leases, compared to $2.4 billion,

or .61%, the year before. Deteriorating credit

quality was largely limited to the corporate

sector in the first half of 2001, but spread to

the consumer sector as the

recession deepened.

We expect

credit costs to remain high in 2002.

The bottom line for shareholders, of course,

is our stock price, and in 2001, we stood head

and shoulders above the rest of the class. In a

year in which the average stock price in our

peer group declined 5%, your company’s stock increased

in value 37%.

Two reasons for heightened investor confidence have

been

our disciplined approach to balance sheet management

and

our commitment to returning capital to shareholders.

Throughout the company, we used relationship-banking

and pricing incentives to boost deposits. At the

same time,

we reduced low-returning corporate loans on our balance

sheet. The result is a loan-to-deposit

ratio that today is lower

than 1:1, which reduces inherent

interest rate risk and

enhances our ability to control funding

costs in the future.

We also continued to

return capital to shareholders in 2001,

nearly

exhausting the stock repurchase program of 100

Chairman’s Letter to Shareholders

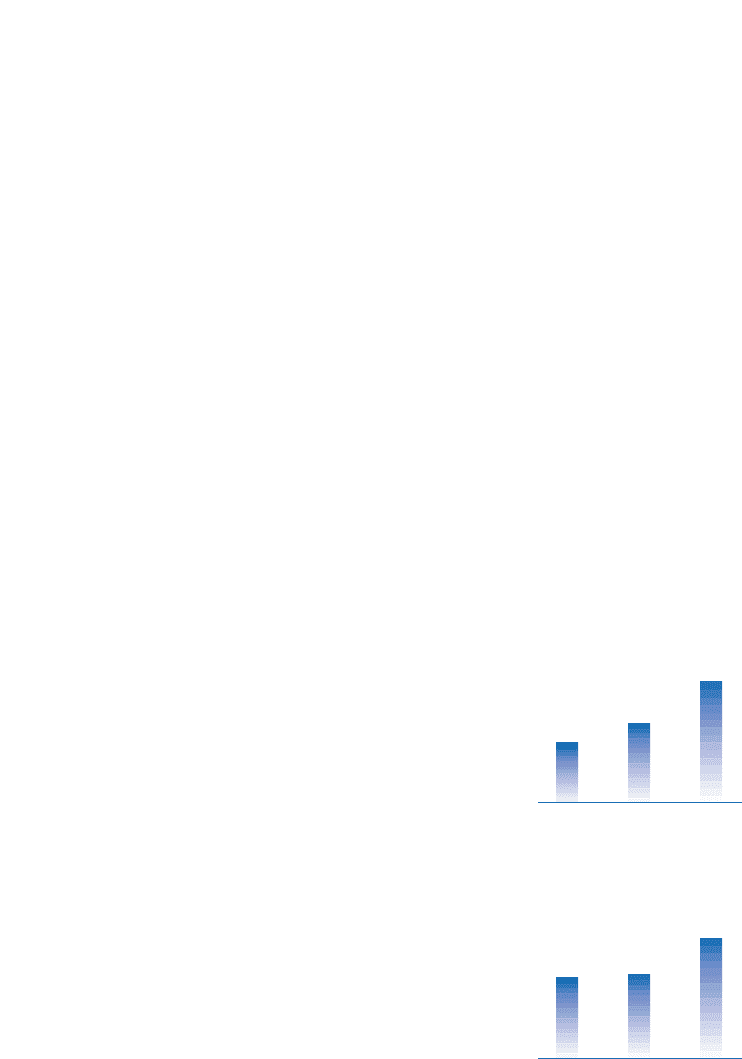

NONINTEREST EXPENSE

(Operating Basis)

1999 2000 2001

(Dollars in billions)

$18.0 $18.1

$19.4

REVENUE

(Taxable Equivalent Basis)

1999 2000 2001

(Dollars in billions)

$32.5

$33.3

$35.0