Bank of America 2001 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

19

We offer clients significant advantages: convenient access, a comprehensive product

mix and highly motivated people. Add those competitive strengths to our solid existing

base, and we see significant opportunity for 2002 in the Small Business segment.

There is also opportunity for significant growth among

those small businesses we already count as clients, by

broadening and deepening our relationships with them.

Providing world-class value packages and service, on top of

all the advantages we can already offer the small business

client, will enable us to grow our share of their business.

Finally, we see the opportunity – and the necessity – to

improve client satisfaction. Our focus will be earning satisfac-

tion scores of 9 and 10 on a 10-point scale, which defines the

category of “highly satisfied.” Highly satisfied clients are more

loyal and more willing to give us more of their

business in those deeper, broader relationships.

Customer satisfaction scores will be key bench-

marks for gauging our success as a company.

Executing our Small Business strategy

for 2002, we will address each of these opportu-

nities for growth in the segment, with initiatives

that directly address our determination to attract,

retain and deepen client relationships.

To identify and attract valuable new clients,

we’re expanding our product lines and developing

value packages, as well as more robust information tools and

processes. As with the Consumer Banking segment, we are

placing special emphasis on marketing to multicultural clients

which are so important in our key growth states. Helping them

grow will help us grow, and will make an important contribution

toward the overall Bank of America commitment to diversity.

Enhancing our customer knowledge systems will also

enable us to better understand the needs and opportunities

of our existing clients, so we can better provide the products

and services that are right for them – like online banking, card

services, treasury management and insurance. At the same

time, we will be integrating our sales processes and imple-

menting a disciplined relationship-management model to

provide a more consistent, high level of service to our clients.

To further enhance our clients’ experience, we are imple-

menting new small-business training programs for banking center

associates, so they can provide better, more comprehensive

service. And we are motivating our associates by directly

connecting their rewards, incentives and recognition to their

contributions in helping us achieve our key strategic objec-

tives: attracting new customers, retaining existing

customers, and building stronger, deeper relationships with

all our customers. We’re confident that these steps will be

important parts of our effort to raise client satisfaction

toward world-class levels.

As a further, vital step, we are undertaking intensive efforts

to improve our core processes, which we define as those

processes that directly touch our customers.

Deposit servicing, payment processing and bank-

ing center processes are all areas that our clients

have told us affect their satisfaction. Our intention

is to bring these processes to world class, using

engineering methods that have proven effective in

other businesses. Improving our processes will also

add to shareholder value by enhancing productivity

and thereby reducing expenses.

We are also taking steps to improve our

online banking services for small businesses,

which are already among the best and most innovative in the

industry. We have more than 200,000 active users of online

services among our small-business clients, and we have seen

significant effects. Our online clients are more profitable.

They have higher loan and deposit balances. They are much

more likely to add products and services, and much less likely

to leave the bank. They make fewer calls to call centers for

assistance, making them less costly to serve. When we look

at small-business clients who pay their bills online, those

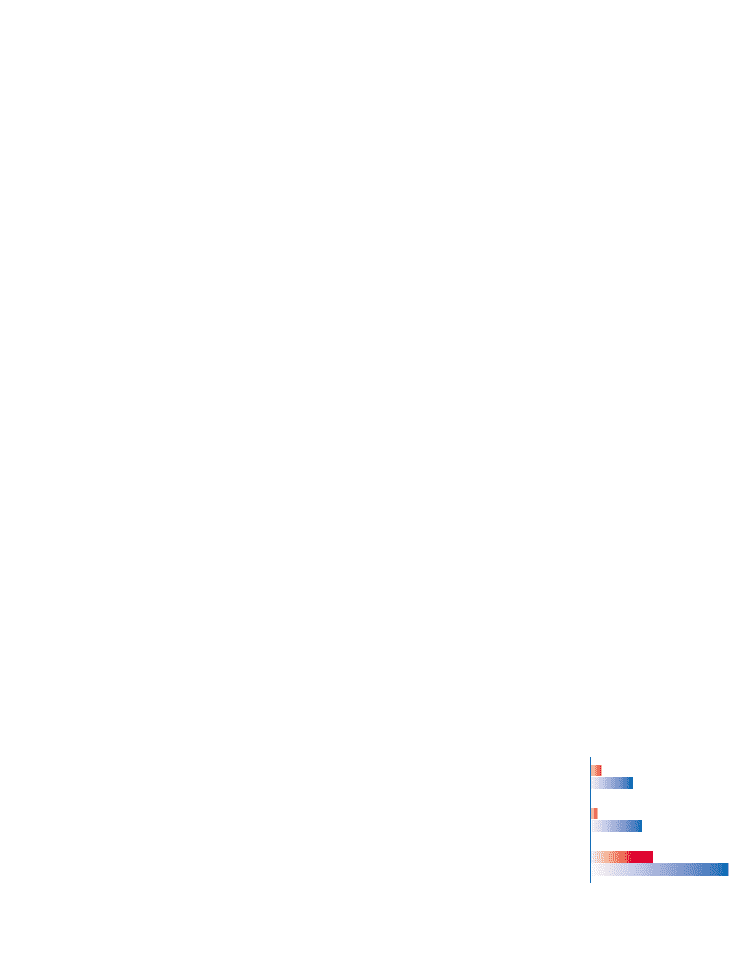

effects are heightened (see graph, this page). As our clients

access a growing array of Web-enabled financial products

and services, our costs to serve them will decline, and cus-

tomer satisfaction will grow.

In sum, we are confident that integrating sales processes

and focusing on customer satisfaction, associate satisfaction

and SVA will help us build deeper, more profitable relation-

ships – across the bank and in the Small Business segment.

THE ONLINE ADVANTAGE

■

Online

■

Online with BillPay

Percentage Gain from

Online vs. Non-Online Customers

0604020 80

*

Measured in account attrition reduction

Loan

balances

Deposit

balances

Customer

loyalty*