Bank of America 2001 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

BANK OF AMERICA 2001 ANNUAL REPORT

94

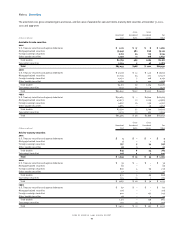

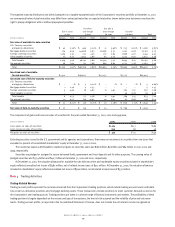

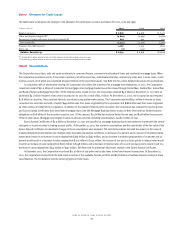

Note 6 Loans and Leases

Loans and leases at December 31, 2001 and 2000 were:

2001 2000

(Dollars in millions)

Amount Percent Amount Percent

Commercial – domestic $ 118,205 35.9% $146,040 37.2%

Commercial – foreign 23,039 7.0 31,066 7.9

Commercial real estate – domestic 22,271 6.8 26,154 6.7

Commercial real estate – foreign 383 .1 282 .1

Total commercial 163,898 49.8 203,542 51.9

Residential mortgage 78,203 23.8 84,394 21.5

Home equity lines 22,107 6.7 21,598 5.5

Direct/Indirect consumer 37,638 11.5 40,457 10.3

Consumer finance 5,331 1.6 25,800 6.6

Bankcard 19,884 6.0 14,094 3.6

Foreign consumer 2,092 .6 2,308 .6

Total consumer 165,255 50.2 188,651 48.1

Total loans and leases $ 329,153 100.0% $ 392,193 100.0%

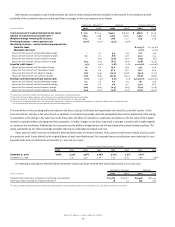

As part of the strategic decision to exit the subprime real estate lending business in the third quarter of 2001, the Corporation recorded a provision

for credit losses of $395 million which, combined with an existing allowance for credit losses of $240 million, was used to write the loan portfolio down

to estimated market value. As a result, charge-offs of $635 million were recorded in the subprime real estate loan portfolio. The entire subprime real

estate loan portfolio of approximately $21.4 billion, which was included in consumer finance loans, was transferred from the loans and leases portfolio

to loans held for sale included in other assets.

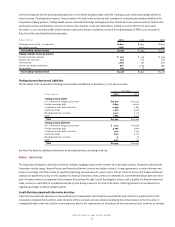

The following table presents the recorded investment in specific loans that were considered individually impaired in accordance with SFAS 114 at

December 31, 2001 and 2000:

(Dollars in millions)

2001 2000

Commercial – domestic $3,138 $2,891

Commercial – foreign 501 521

Commercial real estate – domestic 240 412

Commercial real estate – foreign –2

Total impaired loans $3,879 $3,826

The average recorded investment in certain impaired loans for the years ended December 31, 2001, 2000 and 1999 was approximately $3.7 billion,

$3.0 billion and $2.0 billion, respectively. At December 31, 2001 and 2000, the recorded investment in impaired loans requiring an allowance for

credit losses was $3.1 billion and $2.1 billion, and the related allowance for credit losses was $763 million and $640 million, respectively. For the

years ended December 31, 2001, 2000 and 1999, interest income recognized on impaired loans totaled $195 million, $174 million and $84 million,

respectively, all of which was recognized on a cash basis.

At December 31, 2001 and 2000, nonperforming loans, including certain loans which were considered impaired, totaled $4.5 billion and $5.2 billion,

respectively. Included in other assets was $1.0 billion and $124 million of loans held for sale which would have been classified as nonperforming had

they been included in loans at December 31, 2001 and 2000, respectively. The decrease in nonperforming loans was primarily due to the transfer of

approximately $1.2 billion of nonperforming subprime real estate loans to loans held for sale in 2001 as a result of the decision to exit the subprime

real estate lending business. The decrease was also due to sales of nonperforming commercial – domestic and residential mortgage loans in 2001.

The net amount of interest income recorded during each year on loans that were classified as nonperforming or restructured at December 31, 2001,

2000 and 1999 was $256 million, $237 million and $123 million, respectively. If these loans had been accruing interest at their originally contracted

rates, related income would have been $593 million, $666 million and $419 million in 2001, 2000 and 1999, respectively.

Foreclosed properties amounted to $402 million and $249 million at December 31, 2001 and 2000, respectively. The cost of carrying foreclosed

properties amounted to $15 million, $12 million, and $13 million in 2001, 2000 and 1999, respectively.