Bank of America 2001 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

BANK OF AMERICA 2001 ANNUAL REPORT

82

Bank of America Corporation (the Corporation) is a Delaware corporation, a bank holding company and a financial holding company. Through its

banking and nonbanking subsidiaries, the Corporation provides a diverse range of financial services and products throughout the U.S. and in selected

international markets. At December 31, 2001, the Corporation operated its banking activities primarily under two charters: Bank of America, N.A. and

Bank of America, N.A. (USA).

Note 1 Significant Accounting Policies

Principles of Consolidation and Basis of Presentation

The consolidated financial statements include the accounts of the Corporation and its majority-owned subsidiaries. All significant intercompany accounts

and transactions have been eliminated. Results of operations of companies purchased are included from the dates of acquisition. Certain prior period

amounts have been reclassified to conform to current year classifications. Assets held in an agency or fiduciary capacity are not included in the

consolidated financial statements.

The preparation of the consolidated financial statements in conformity with accounting principles generally accepted in the United States requires

management to make estimates and assumptions that affect reported amounts and disclosures. Actual results could differ from those estimates.

Significant estimates made by management are discussed in these notes as applicable.

Recently Issued Accounting Pronouncements

Statement of Financial Accounting Standards No. 133, “Accounting for Derivative Instruments and Hedging Activities,” (SFAS 133) as amended by

Statement of Financial Accounting Standards No. 137, “Accounting for Derivative Instruments and Hedging Activities – Deferral of Effective Date of

Financial Accounting Standards Board Statement No. 133,” and Statement of Financial Accounting Standards No. 138, “Accounting for Certain

Derivative Instruments and Certain Hedging Activities – an amendment of FASB Statement No. 133,” was adopted by the Corporation on January 1,

2001. The impact of adopting SFAS 133 to net income was a loss of $52 million (net of related income tax benefits of $31 million), and a net transition

gain of $9 million (net of related income taxes of $5 million) included in other comprehensive income on January 1, 2001. Because the transition adjust-

ment was not material to the Corporation’s overall results, the before-tax charge to earnings was included in trading account profits in noninterest

income rather than shown separately as the cumulative effect of an accounting change. Further, the initial adoption of SFAS 133 resulted in the

Corporation recognizing on the balance sheet $577 million of derivative assets and $514 million of derivative liabilities.

In September 2000, the FASB issued Statement of Financial Accounting Standards No. 140, “Accounting for Transfers and Servicing of Financial

Assets and Extinguishments of Liabilities – a replacement of FASB Statement No. 125” (SFAS 140). SFAS 140 was effective for transfers occurring after

March 31, 2001 and for disclosures relating to securitization transactions and collateral for fiscal years ending after December 15, 2000. The adoption

of SFAS 140 did not have a material impact on the Corporation’s results of operations or financial condition.

In June 2001, the FASB issued Statement of Financial Accounting Standards No. 141, “Business Combinations” (SFAS 141) and Statement of Financial

Accounting Standards No. 142, “Goodwill and Other Intangible Assets” (SFAS 142). SFAS 141 was effective for business combinations initiated after

June 30, 2001. SFAS 141 requires that all business combinations completed after its adoption be accounted for under the purchase method of accounting

and establishes specific criteria for the recognition of intangible assets separately from goodwill. SFAS 142 became effective for the Corporation on

January 1, 2002 and primarily addresses the accounting for goodwill and intangible assets subsequent to their acquisition. SFAS 142 requires that

goodwill be recorded at the reporting unit level. Reporting units are defined as an operating segment or one level below. The Corporation has determined

its reporting units and assigned goodwill to them. The Corporation has evaluated the lives of intangible assets as required by SFAS 142 and determined

that no change will be made regarding lives upon adoption. SFAS 142 prohibits the amortization of goodwill but requires that it be tested for impairment

at least annually at the reporting unit level. The impairment test will be performed in two phases. The first step of the goodwill impairment test, used

to identify potential impairment, compares the fair value of a reporting unit with its carrying amount, including goodwill. If the fair value of the reporting

unit exceeds its carrying amount, goodwill of the reporting unit is considered not impaired; however, if the carrying amount of a reporting unit exceeds

its fair value an additional procedure must be performed. That additional procedure compares the implied fair value of the reporting unit goodwill with

the carrying amount of that goodwill. An impairment loss is recorded to the extent that the carrying amount of goodwill exceeds its implied fair value.

Management does not anticipate that an impairment charge will be recorded as a result of the adoption of SFAS 142. Based on amortization expense

recorded in 2001, the Corporation estimates that the elimination of goodwill amortization expense will increase net income by approximately

$600 million, or approximately $0.37 per common share (diluted).

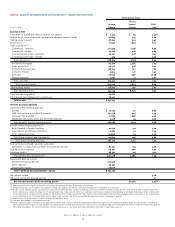

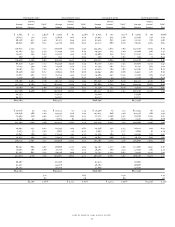

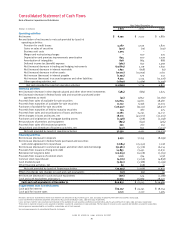

Notes to Consolidated Financial Statements

Bank of America Corporation and Subsidiaries