Bank of America 2001 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

BANK OF AMERICA 2001 ANNUAL REPORT

83

In June 2001, the FASB also issued Statement of Financial Accounting Standards No. 143, “Accounting for Asset Retirement Obligations” (SFAS 143).

SFAS 143 is effective for financial statements issued for fiscal years beginning after June 15, 2002. SFAS 143 addresses financial accounting and report-

ing for obligations associated with the retirement of tangible long-lived assets and the associated asset retirement costs. The Corporation does not

expect the adoption of this pronouncement to have a material impact on its results of operations or financial condition.

In August 2001, the FASB issued Statement of Financial Accounting Standards No. 144, “Accounting for the Impairment or Disposal of Long-Lived

Assets” (SFAS 144). SFAS 144 is effective for financial statements issued for fiscal years beginning after December 15, 2001. The standard addresses

financial accounting and reporting for the impairment or disposal of long-lived assets. The Corporation does not expect the adoption of this

pronouncement to have a material impact on its results of operations or financial condition.

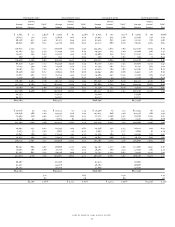

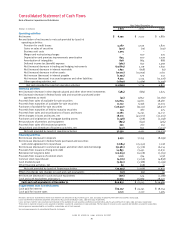

Cash and Cash Equivalents

Cash on hand, cash items in the process of collection and amounts due from correspondent banks and the Federal Reserve Bank are included in cash

and cash equivalents.

Securities Purchased under Agreements to Resell and Securities Sold under Agreements to Repurchase

Securities purchased under agreements to resell and securities sold under agreements to repurchase are treated as collateralized financing transactions

and are recorded at the amounts at which the securities were acquired or sold plus accrued interest. The Corporation’s policy is to obtain the use of

securities purchased under agreements to resell. The market value of the underlying securities, which collateralize the related receivable on agreements

to resell, is monitored, including accrued interest, and additional collateral is requested when deemed appropriate.

Collateral

The Corporation has accepted collateral that it is permitted by contract or custom to sell or repledge. At December 31, 2001, the fair value of this

collateral was approximately $30.4 billion of which $21.5 billion was sold or repledged. At December 31, 2000, the fair value of this collateral was

approximately $25.1 billion of which $22.7 billion was sold or repledged. The primary source of this collateral is reverse repurchase agreements.

The Corporation pledges securities as collateral in transactions that are primarily repurchase agreements, public and trust deposits, treasury tax and

loan and other short-term borrowings. This collateral can be sold or repledged by the counterparties to the transactions.

In addition, the Corporation obtains collateral in connection with its derivative activities. Required collateral levels vary depending on the

credit risk rating and the type of counterparty. Generally, the Corporation accepts collateral in the form of cash, U.S. Treasury securities and other

marketable securities.

Trading Instruments

Financial instruments utilized in trading activities are stated at fair value. Fair value is generally based on quoted market prices. If quoted market

prices are not available, fair values are estimated based on dealer quotes, pricing models or quoted prices for instruments with similar characteristics.

Realized and unrealized gains and losses are recognized in trading account profits.

Derivatives and Hedging Activities

All derivatives are recognized on the balance sheet at fair value, taking into consideration the effects of legally enforceable master netting agreements

which allow the Corporation to settle positive and negative positions with the same counterparty on a net basis. For exchange traded contracts, fair

value is based on quoted market prices. For non-exchange traded contracts, fair value is based on dealer quotes, pricing models or quoted prices for

instruments with similar characteristics. The Corporation designates a derivative as held for trading or hedging purposes when it enters into a derivative

contract. Derivatives designated as held for trading activities are included in the Corporation’s trading portfolio with changes in fair value reflected in

trading account profits.

The Corporation uses its derivatives designated for hedging activities as either fair value hedges, cash flow hedges, or hedges of net investments

in foreign operations. The Corporation primarily manages interest rate and foreign currency exchange rate sensitivity through the use of derivatives.

Fair value hedges are used to limit the Corporation’s exposure to changes in the fair value of its interest-bearing assets or liabilities that are due to

interest rate volatility. Cash flow hedges are used to minimize the variability in cash flows of interest-bearing assets or liabilities or anticipated

transactions caused by interest rate fluctuations. Changes in the fair value of derivatives designated for hedging activities that are highly effective as

hedges are recorded in earnings or other comprehensive income, depending on whether the hedging relationship satisfies the criteria for a fair value

or cash flow hedge, respectively. A highly effective hedging relationship is one in which the Corporation achieves offsetting changes in fair value or

cash flows between 80 percent and 120 percent for the risk being hedged. Hedge ineffectiveness and gains and losses on the excluded component of

a derivative in assessing hedge effectiveness are recorded in earnings. SFAS 133 retains certain concepts under Statement of Financial Accounting

Standards No. 52, “Foreign Currency Translation,” (SFAS 52) for foreign currency exchange hedging. Consistent with SFAS 52, the Corporation records

changes in the fair value of derivatives used as hedges of the net investment in foreign operations as a component of other comprehensive income.