Bank of America 2001 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

BANK OF AMERICA 2001 ANNUAL REPORT

39

profits, on certain mortgage banking assets and the related derivative instruments. These increases were partially offset by increased

prepayments on mortgage loans as a result of the declining interest rate environment. Credit card income grew $75 million, or four percent,

due to new consumer card account growth and an increase in purchase volume, partially offset by a decline in servicing income from maturity

of credit card securitizations.

>The $370 million, or 34 percent, increase in cash basis earnings in 2001 was due to the increases in net interest income and noninterest income

discussed above. These increases were partially offset by an increase in the provision for credit losses and higher expenses. Expense growth was

primarily driven by card marketing and mortgage production volume activities.

>

The provision for credit losses increased 74 percent to $915 million primarily due to higher net charge-offs in the bankcard loan portfolio. The

increase in bankcard charge-offs was driven by portfolio growth, an increase in personal bankruptcy filings and a weaker economic environment.

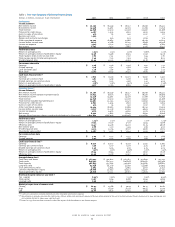

Commercial Banking

Commercial Banking provides commercial lending and treasury management services to middle market companies with annual revenue between

$10 million and $500 million. These services are available through relationship manager teams as well as through alternative channels such as the

telephone via the commercial service center and the Internet by accessing Bank of America Direct.

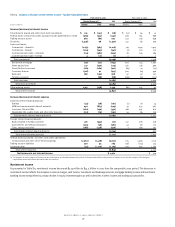

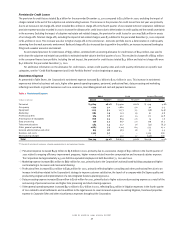

Commercial Banking

(Dollars in millions)

2001 2000

Net interest income $2,592 $ 2,651

Noninterest income 1,033 987

Total revenue 3,625 3,638

Provision for credit losses 606 316

Cash basis earnings 924 1,067

Shareholder value added 386 488

Cash basis efficiency ratio 45.6% 44.7%

>Noninterest income increased five percent and was offset by a two percent decline in net interest income. Total revenue in 2001 remained flat at

$3.6 billion.

>

The $46 million increase in noninterest income was primarily attributable to higher corporate service charges as customers opted to pay

service charges rather than carry excess deposit balances in the lower rate environment, offset by the liquidation of certain commercial

finance businesses.

>

Net interest income declined $59 million, primarily due to a reduction in commercial loans and the liquidation of certain commercial

finance businesses.

>The $143 million, or 13 percent, decline in cash basis earnings was primarily driven by an increase in the provision for credit losses, partially offset

by a tax benefit of $53 million in the fourth quarter of 2001 related to the funding of SSI.

>

The provision for credit losses increased $290 million to $606 million as a result of credit deterioration in the commercial loan portfolio.

>Shareholder value added decreased $102 million as the decline in cash basis earnings was partially offset by lower capital as a result of reductions

in commercial loan levels.

Asset Management

Asset Management includes the Private Bank, Banc of America Capital Management and the Individual Investor Group. The Private Bank’s goal is to

assist individuals and families in building and preserving their wealth by providing investment, fiduciary and comprehensive credit expertise to high-

net-worth clients. Banc of America Capital Management is an asset-gathering and asset management organization serving the needs of institutional

clients, high-net-worth individuals and retail customers. Banc of America Capital Management manages money and distribution channels, manufactures

investment products, offers institutional separate accounts and wrap programs, and provides advice to clients through asset allocation expertise and

software. The Individual Investor Group, which is comprised of Private Client Services and Banc of America Investment Services, Inc., provides investment,

securities and financial planning services to affluent and high-net-worth individuals. Private Client Services focuses on high-net-worth individuals.

Banc of America Investment Services, Inc. includes both the full-service network of investment professionals and an extensive on-line investor service.

One of the Corporation’s strategies is to focus on and grow the asset management business. Recent initiatives include new investment platforms

that broaden the Corporation’s capabilities to maximize market opportunity for its clients. The Corporation continues to enhance the financial planning

tools used to assist clients with their financial goals.

Effective January 2, 2001, the Corporation acquired the remaining 50 percent of Marsico for a total investment of $1.1 billion. The Corporation

acquired the first 50 percent in 1999. Marsico is a Denver-based investment management firm specializing in large capitalization growth stocks.