Bank of America 2001 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

29

combined with our array of high-margin, high-return products

and services, supported by our corporate financial strength,

gives us enormous advantages in the marketplace, where we

use the brand name Banc of America Securities.

We are focusing our resources on industry

sectors where we can establish leading positions,

substantially increase fee generation, grow our

market-making and commission revenues and

improve the efficiency of our capital. We expect

to broaden and deepen our targeted client rela-

tionships to include our full array of advisory,

capital-raising, risk-management and treasury-

services capabilities.

Building on our strong momentum from 2000,

we aggressively pursued our growth strategy in

2001. In just three years we have achieved higher

league table rankings and a larger share of lead-

managed deals and total investment banking

fees. We estimate that in 2001 Banc of America

Securities’ share of total U.S. issuer fees grew

to 5.9% versus 4.7% in 2000 and 3.9% in 1999,

evidence of our successful execution. Today,

according to an independent research company,

we are the sixth-ranked U.S. investment bank in

terms of lead relationships among all large U.S.

corporate clients.

We are executing specific strategies related to both

our issuer and investor clients. Our strategy for issuer clients

contains several elements. First, we are building substantial

expertise around eight key industry groups that generate signifi-

cant fees and possess strong long-term growth potential. We are

leveraging relationships in these sectors to win

investment banking mandates and build leading

market positions. Since 1999, we have had an over-

all increase in the market share of estimated invest-

ment banking fees in our targeted industry sectors.

Second, we have created teams within each

industry group that encompass both corporate

and investment banking expertise. Each team

works across product areas, from traditional

bank and loan products to sophisticated capital

raising, advisory and derivatives capabilities, to

deliver a seamless experience for clients and

deepen each relationship. This has resulted in

significantly more diversified revenue streams

earned from our corporate banking client base.

Third, while we have broad client reach, we

are focusing on strategic clients within our key

sectors to expand fee generation and profit

potential. Today there are nearly 400 such clients

who share our commitment to a relationship

that is mutually beneficial. Our broad range of

market-leading capabilities combined with our

in-depth knowledge of each client’s needs provides

ample ways to serve such a relationship. Today, more than

one-third of these clients regard us as their lead investment

Our extensive product array combined with superior financial strength

enables us to create innovative financial solutions for corporate clients who are

increasingly seeking providers with multi-faceted capabilities.

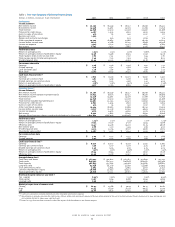

$1.5

$9.2

$1.2

$2.3

$2.6

$1.6

(Dollars in billions)

capital raising and advisory fees

equity sales and trading

debt sales and trading

credit products

global treasury services

GCIB REVENUE 2001

GCIB FINANCIAL PERFORMANCE

■

2000

■

2001

$8.2

$1.8

$0.3

$0.6

$1.9$9.2

Revenue SVANet Income

(Dollars in billions)

IN EXECUTING our originate-to-distribute

strategy, portfolio managers, with authority

over loan underwriting decisions, bring an

investor perspective to discussions to ensure

that loans are attractive for both our portfolio

and the broader market.

While continuing to meet the borrowing

needs of our targeted issuer clients, we have sig-

nificantly reduced corporate loan balances

since mid-2000. We closely examine returns from

each client, seeking to retain and solidify only

relationships that are mutually beneficial. We

also limit concentrated exposure across clients,

industries and geographies, selling loans when

necessary to maintain a maximum threshold. We

have aggressively attacked our problem loan

portfolio through both collections and sales.

Deploying our credit capital resources to our

most profitable relationships while maintaining

lower loan asset levels will lead to higher returns

on credit capital and less risk exposure, driving

growth in shareholder value added.

Portfolio

Management Will

Drive SVA Growth