Bank of America 2001 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

NO CUSTOMER WANTS a complicated banking

experience. That is why many of our quality and

productivity activities focus on making it easier

to do business with Bank of America.

Our recent efforts to reduce the number

of toll-free phone numbers are a good example

of our focus on “ease of doing business.” When

Bank of America inventoried its toll-free tele-

phone numbers, it found 3,915 separate numbers

for customers to call. Eliminating extra numbers

is an obvious way to simplify the customer’s

experience with us. Through this effort, 2,155

toll-free numbers were being disconnected at

year’s end.

When Bank of America reaches its

24-month goal of having just one toll-free

number per customer language, the volume of

misdirected calls due to customers dialing the

wrong call center or business unit will be reduced

by 59%. Annual cost savings are estimated at

$5.8 million.

15

capture the significant growth of multicultural demographics

concentrated in these areas.

Our delivery network is perhaps our greatest strategic

advantage today. It provides superior convenience

for our customers and greater opportunities to

deepen customer relationships.

Through 13,113 ATMs, 4,251 banking centers

and 2.9 million active online users, our customers

touch Bank of America more than 3 billion times

a year, creating 116 opportunities a second to

deepen relationships.

In 2001, despite a very challenging economic

environment, these customer contacts enabled

us to increase total loans and leases for the con-

sumer segment 14% over the previous year, while

deposits rose 1.7%. For the same period, total

revenue for Consumer Banking increased 7.2%.

Consumer Strategy. Three words describe

our strategy: Attract. Retain. Deepen. We are contin-

uing to attract new customers, retaining more of

those whose business we have earned and deepen-

ing our relationships as customers pass milestones

in their lives that create new financial needs.

Customers will be more highly satisfied with

us, and therefore more likely to retain and deepen

their relationships, if they have a good initial experience with

the bank, if they use more of our products and services earlier

and if they move to the right service level faster.

That requires us to listen carefully to our customers,

finding out as much as we can about their needs and learning

what it takes not just to satisfy their requirements, but to

delight them, so that they give us top ratings on

customer satisfaction surveys.

Research shows that “highly satisfied” cus-

tomers are more likely to stay with us longer, more

likely to buy more products and services from us,

more likely to recommend us to their friends and

colleagues – more likely, in other words, to enable

us to increase both market share and profitability.

Attract. Ours is already one of America’s

most powerful financial services brands, promising

overwhelming convenience across location, chan-

nel, transacting capability, products and services.

But in today’s increasingly competitive environ-

ment, these advantages can’t be taken for granted.

Our customers have more than 16 million

checking accounts, and checking products attract

more new customers than any other product.

The ability of checking products to draw new

customers makes these accounts a valuable

engine of relationship growth for several reasons.

The first is customer interaction. Opening a new

checking account involves spending time with cus-

tomers and creates the opportunity to turn a person walking in

the door into a multi-product customer from the start. Second,

because these customers rely on us for continuous service,

We have a tremendous franchise and customer base. Our job now is to grow net

income

by deepening relationships through our entire range of products and services.

Doing so

represents the largest net-income growth opportunity in the corporation.

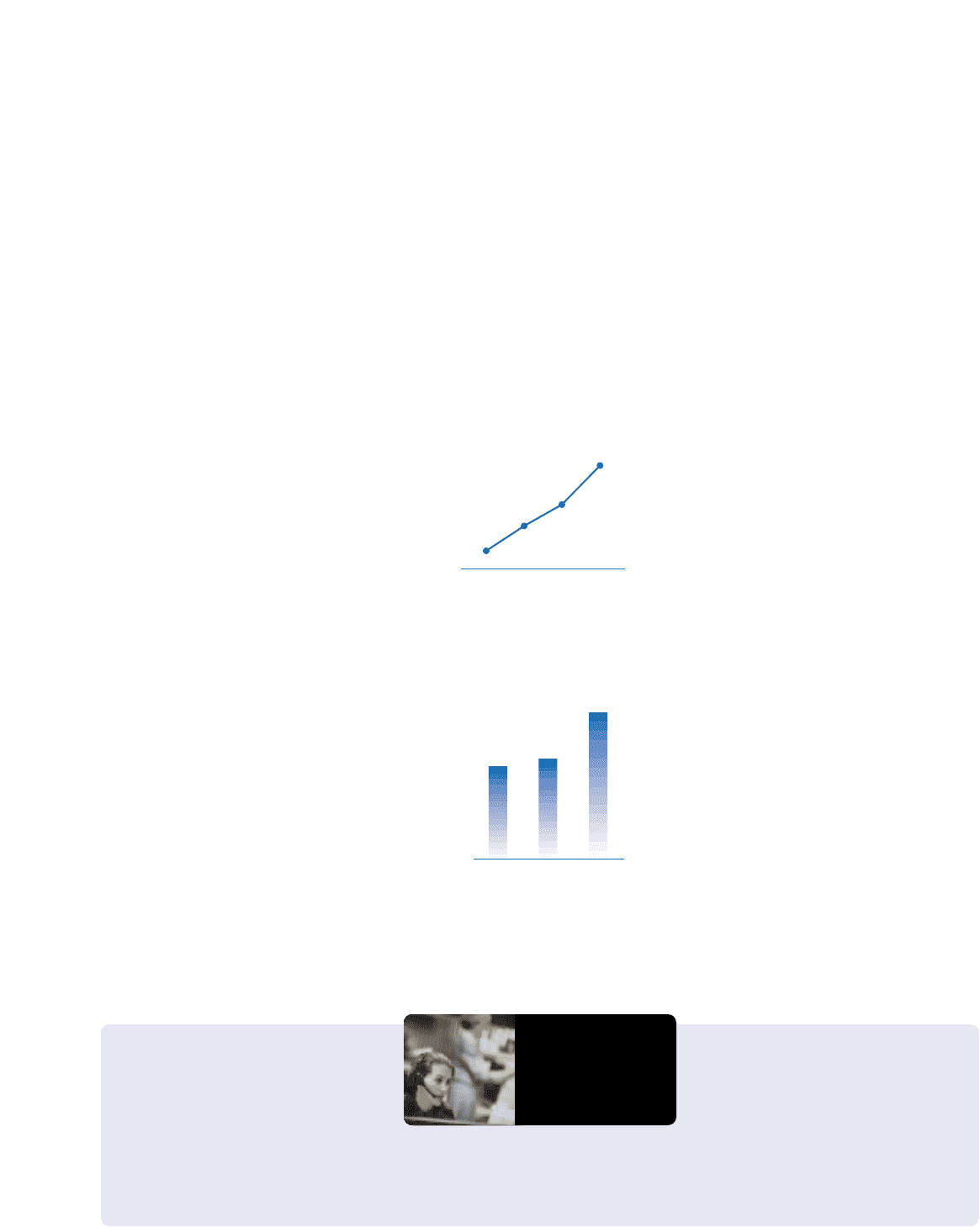

STEADY GROWTH IN

ONLINE BANKING

CUSTOMERS WHO

SAY THEY ARE

“HIGHLY SATISFIED”

Dec

1999 Dec

2000 Dec

2001

42% 43%

49%

40%

30%

50%

Dec

1998 Dec

1999 Dec

2001

Dec

2000

1

0

2

3

Source: Model Banking Center Gallup Results

(Number of active consumer

users in millions)

Getting Customers

the Right

Phone Number