Bank of America 2001 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

BANK OF AMERICA 2001 ANNUAL REPORT

33

This Annual Report contains certain forward-looking statements that are subject to risks and uncertainties and include information about possible or

assumed future results of operations. Many possible events or factors could affect the future financial results and performance of Bank of America Corporation

(the Corporation). This could cause results or performance to differ materially from those expressed in our forward-looking statements. Words such as

“expects”, “anticipates”, “believes”, “estimates”, variations of such words and other similar expressions are intended to identify such forward-looking

statements. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions which are difficult to predict.

Therefore, actual outcomes and results may differ materially from what is expressed or forecasted in, or implied by, such forward-looking statements.

Readers of the Corporation’s Annual Report should not rely solely on the forward-looking statements and should consider all uncertainties and risks

discussed throughout this report. These statements are representative only on the date hereof, and the Corporation undertakes no obligation to update any

forward-looking statements made.

The possible events or factors include the following: the Corporation’s loan growth is dependent on general economic conditions as well as various

discretionary factors such as decisions to securitize, sell, or purchase certain loans or loan portfolios; syndications or participations of loans; retention of resi-

dential mortgage loans; and the management of borrower, industry, product and geographic concentrations and the mix of the loan portfolio. The level of

nonperforming assets, charge-offs and provision expense can be affected by local, regional and international economic and market conditions, including

the concentrations of borrowers, industries, products and geographic locations, the mix of the loan portfolio and management’s judgments regarding the

collectibility of loans. Liquidity requirements may change as a result of fluctuations in assets and liabilities and off-balance sheet exposures, which will

impact the capital and debt financing needs of the Corporation and the mix of funding sources. Decisions to purchase, hold or sell securities are also depend-

ent on liquidity requirements and market volatility, as well as on- and off-balance sheet positions. Factors that may impact interest rate risk include local,

regional and international economic conditions, levels, mix, maturities, yields or rates of assets and liabilities, utilization and effectiveness of interest

rate contracts and the wholesale and retail funding sources of the Corporation. The Corporation is also exposed to the potential of losses arising from

adverse changes in market rates and prices which can adversely impact the value of financial products, including securities, loans, deposits, debt and

derivative financial instruments, such as futures, forwards, swaps, options and other financial instruments with similar characteristics. The Corporation is

also exposed to potential litigation liabilities, including costs, expenses, settlements and judgments, that may adversely affect the Corporation.

In addition, the banking industry in general is subject to various monetary and fiscal policies and regulations, which include those determined by

the Federal Reserve Board, the Office of the Comptroller of Currency, the Federal Deposit Insurance Corporation, state regulators and the Office of Thrift

Supervision, whose policies and regulations could affect the Corporation’s results. Other factors that may cause actual results to differ from the forward-

looking statements include the following: projected business increases following process changes and productivity and investment initiatives are lower

than expected or do not pay for severance or other related costs as quickly as anticipated; competition with other local, regional and international banks,

thrifts, credit unions and other nonbank financial institutions, such as investment banking firms, investment advisory firms, brokerage firms, investment

companies and insurance companies, as well as other entities which offer financial services, located both within and outside the United States and through

alternative delivery channels such as the Internet; interest rate, market and monetary fluctuations; inflation; market volatility; general economic conditions and

economic conditions in the geographic regions and industries in which the Corporation operates; introduction and acceptance of new banking-related

products, services and enhancements; fee pricing strategies, mergers and acquisitions and their integration into the Corporation; and management’s

ability to manage these and other risks.

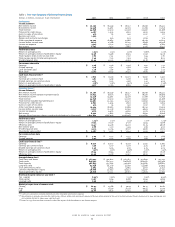

Overview

The Corporation is a Delaware corporation, a bank holding company and a financial holding company, and is headquartered in Charlotte, North Carolina.

The Corporation operates in 21 states and the District of Columbia and has offices located in 34 countries. The Corporation provides a diversified

range of banking and certain nonbanking financial services and products both domestically and internationally through four business segments:

Consumer and Commercial Banking, Asset Management, Global Corporate and Investment Banking and Equity Investments. A customer-centered

strategic focus is changing the way the Corporation is managing its business. In addition to existing financial reporting, the Corporation has begun

preparing customer segment-based financial operating information. At December 31, 2001, the Corporation had $622 billion in assets and approximately

143,000 full-time equivalent employees. Refer to Table One and Table Twenty-Five for annual and quarterly selected financial data, respectively.

Key performance highlights for 2001 compared to 2000:

> Net income totaled $6.8 billion, or $4.18 per common share (diluted), compared to $7.5 billion, or $4.52 per common share (diluted). The return

on average common shareholders’ equity was 13.96 percent.

>Operating earnings, which excluded charges related to the Corporation’s strategic decision to exit certain consumer finance businesses in 2001

and related to restructuring in 2000, totaled $8.0 billion, or $4.95 per common share (diluted), compared to $7.9 billion, or $4.72 per common

share (diluted). Excluding exit charges, the return on average common shareholders’ equity was 16.53 percent in 2001. Shareholder value added

(SVA), excluding exit and restructuring charges, remained essentially unchanged at $3.1 billion.

Management’s Discussion and Analysis

of Results of Operations and Financial Condition