Bank of America 2001 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

BANK OF AMERICA 2001 ANNUAL REPORT

54

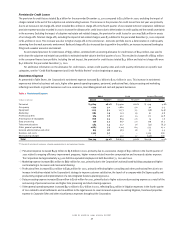

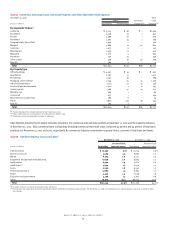

which reduced shareholders’ equity by $4.7 billion and increased earnings per share by approximately $0.08 for the year ended December 31, 2001.

Management anticipates it will continue to repurchase shares at least equal to shares issued under its various stock option plans. See Note Thirteen

of the consolidated financial statements for additional disclosures related to the repurchase program.

On October 24, 2001, the Board approved a $0.04 per share, or seven percent, increase in the quarterly common dividend. This increase brings

the common dividend to $0.60 per share for the fourth quarter of 2001 and $2.28 per share for the year ended December 31, 2001.

The regulatory capital ratios of the Corporation and Bank of America, N.A., along with a description of the components of risk-based capital,

capital adequacy requirements and prompt corrective action provisions, are included in Note Fourteen of the consolidated financial statements.

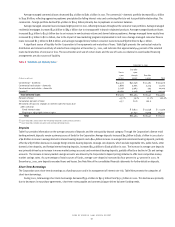

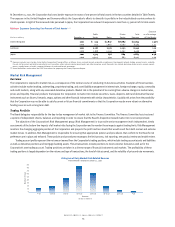

Risk Management Overview

The Corporation’s goal in managing risk is to produce appropriate risk-adjusted returns, reduce the wide volatility in earnings and increase shareholder

value. The Corporation believes it has a governance structure and risk management approach in place in order to reach that goal. Processes are designed

to align the Corporation’s measures for business success with the measures for return, growth and risk. Further, these processes enable the Corporation

to better communicate with its associates the corporate appetite for risk, manage sources of earnings’ volatility and manage appropriate capital levels.

The Corporation manages risk by adherence to the following key principles:

>Emphasize that individual decision-making and accountability are the cornerstone.

>Include risk assessments in all business units.

>Appropriate limits, policies, procedures and measures are in place.

>Independently test, verify and evaluate controls.

>Identify and minimize the sources of earnings’ volatility.

>Use SVA as a key financial measure to evaluate businesses and to direct capital.

Each of these key principles contributes to a more risk/return focused culture. Importantly, the Corporation believes SVA leads to better risk/return

decisioning and to a lower risk profile. Reinforcing the cost of capital among the Corporation’s business segments creates critical assessments of the

Corporation’s uses of capital. The cost of capital for each business is based on an assessment of its specific credit, market and operational risk.

The goal of the governance structure is to enable management to actively balance risk and return.

>The Chief Financial Officer has oversight responsibility for the soundness of the Corporation’s capitalization and earnings.

>The Chief Risk Officer has enterprise-wide oversight of market, credit and operational risks.

>The business unit leaders have responsibility for meeting corporate performance objectives within the boundaries of their allocated risk position.

The Corporation manages day-to-day risk-taking through three senior executive committees. The Risk and Capital Committee determines the

corporate objectives for each performance measure, allocates capital, sets aggregate risk levels and plans the use of capital. It also coordinates two

committees responsible for market and credit risk. The Asset and Liability Committee reviews aggregate balance sheet exposures, including trading

positions, recommends balance sheet capital allocations and recommends changes in the market risk profile. The Credit Risk Committee reviews

business asset quality, portfolio management results and industry concentrations and limits.

The Board of Directors addresses risk in three ways. The Finance Committee oversees both market and credit risk through reports from the Asset

and Liability Committee and the Credit Risk Committee. The Asset Quality Committee of the Board also reviews credit risk, and the Audit Committee

of the Board reviews the scope and coverage of the external audit and internal audit activities.

Senior management and the Board of Directors oversight builds on the cornerstone of the Corporation’s corporate governance: individual

decision-making and accountability. The Corporation’s corporate governance is designed so that individuals at all levels are delegated appropriate

authority, take appropriate action and are accountable for actions taken. Wherever practical, decision-making authority is delegated as close to the

customer as possible.

The following sections, Credit Risk Management and Credit Portfolio Review, Market Risk Management and Liquidity Risk Management, provide

specific information on the Corporation’s processes and current risk assessment in each area as of December 31, 2001 and 2000.

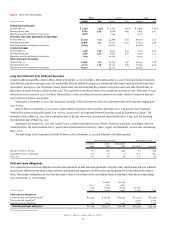

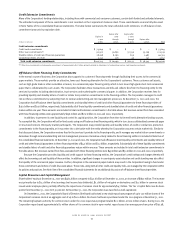

Credit Risk Management and Credit Portfolio Review

In conducting business activities, the Corporation is exposed to the risk that borrowers or counterparties may default on their obligations to the

Corporation. This exposure exists in both on- and off-balance sheet relationships. Credit risk arises through the extension of loans and leases, certain

securities, off-balance sheet letters of credit and financial guarantees, unfunded loan commitments and through counterparty exposure on trading

and capital markets transactions. To manage both on- and off-balance sheet credit risk, the Risk Management group, which reports to the Chief Risk

Officer, establishes policies and procedures and communicates, implements and monitors the application of these throughout the Corporation.

The Corporation uses statistical techniques and modeling to estimate both expected losses and unexpected losses for each segment of the port-

folio. The expected loss drives the periodic credit cost charged to earnings for management reporting purposes, and the unexpected loss estimate

drives the capital allocation to each business unit. Both the expected loss and unexpected loss are incorporated into each business unit's SVA meas-

urement. As a result, the overall credit risk profile of each business unit is an important factor in assessing its performance.