Bank of America 2001 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

BANK OF AMERICA 2001 ANNUAL REPORT

36

Summary of Significant Accounting Policies

The Corporation’s accounting policies are fundamental to understanding management’s discussion and analysis of results of operations and financial

condition. Many of the Corporation’s accounting policies require significant judgment regarding valuation of assets and liabilities and/or significant

interpretation of the specific accounting guidance. The Corporation’s significant accounting policies are discussed in detail in Note One of the con-

solidated financial statements. The following is a summary of the more judgmental and complex accounting policies of the Corporation.

Many of the Corporation’s assets and liabilities are recorded using various valuation techniques that require significant judgment as to recoverability.

The collectablity of loans is reflected through the Corporation’s estimate of the allowance for credit losses. The Corporation performs periodic and

systematic detailed reviews of its lending portfolio to assess overall collectibility. In addition, certain assets and liabilities are reflected at their

estimated fair value in the consolidated financial statements. Such amounts are based on either quoted market prices or estimated values derived by

the Corporation utilizing dealer quotes, market comparisons or internally generated modelling techniques. The Corporation’s internal models generally

involve present value of cash flow techniques. The various valuation techniques are discussed in greater detail elsewhere in management’s discussion

and analysis and the notes to the consolidated financial statements.

There are other complex accounting standards that require the Corporation to employ significant judgment in interpreting and applying certain

of the principles prescribed by those standards. These judgments include, but are not limited to, the determination of whether a financial instrument or

other contract meets the definition of a derivative in accordance with Statement of Financial Accounting Standards No. 133, “Accounting for Derivative

Instruments and Hedging Activities” (SFAS 133), and the applicable hedge deferral criteria, the accounting for the transfer of financial assets and

extinguishments of liabilities in accordance with Statement of Financial Accounting Standards No. 140, “Accounting for Transfers and Servicing of

Financial Assets and Extinguishments of Liabilities” (SFAS 140), and the determination of when certain special purpose vehicles should be consolidated

in the Corporation’s balance sheet and statement of income. For a more complete discussion of these policies, see Notes One, Five and Eight of the

consolidated financial statements.

The remainder of management’s discussion and analysis of the Corporation’s results of operations and financial position should be read in

conjunction with the consolidated financial statements and related notes presented on pages 78 through 119.

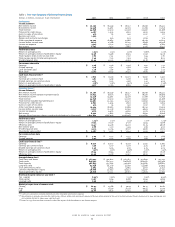

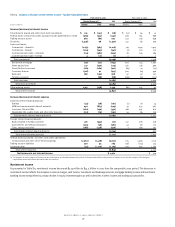

Business Segment Operations

The Corporation provides a diversified range of banking and nonbanking financial services and products through its various subsidiaries. The Corporation

manages its operations through four business segments: Consumer and Commercial Banking, Asset Management, Global Corporate and Investment

Banking and Equity Investments. Certain operating segments have been aggregated into a single business segment. In the first quarter of 2001, the

thirty-year mortgage portfolio was moved from Consumer and Commercial Banking to the Corporate Other segment. In the third quarter of 2001, certain

consumer finance businesses being liquidated were transferred from Consumer and Commercial Banking to Corporate Other. A customer-centered

strategic focus is changing the way the Corporation is managing its business. In addition to existing financial reporting, the Corporation has begun

preparing customer segment-based financial operating information.

The business segments summarized in Table Two are primarily managed with a focus on various performance measures including total revenue,

net income, shareholder value added (SVA), return on average equity and efficiency. Some of these performance measures are also presented on a

cash basis which excludes the impact of goodwill and other intangible amortization expense. Total revenue includes net interest income on a taxable-

equivalent basis and noninterest income. The net interest income of the business segments reflects the results of a funds transfer pricing process

which matches assets and liabilities with similar interest rate sensitivity and maturity characteristics and reflects the allocation of net interest income

related to the Corporation’s overall asset and liability management activities on a proportionate basis. SVA is a performance measure that is aligned

with the Corporation’s growth strategy orientation and strengthens the Corporation’s focus on generating long-term growth and shareholder value. SVA

is defined as cash basis operating earnings less a charge for the use of capital. The capital charge is calculated by multiplying 12 percent (management’s

estimate of the shareholder’s minimum required rate of return on capital invested) by average total common shareholders’ equity (at the Corporation

level) and by average allocated equity (at the business segment level). Equity is allocated to each business segment based on an assessment of its

inherent risk.

See Note Nineteen of the consolidated financial statements for additional business segment information, reconciliations to consolidated amounts

and information on Corporate Other. Additional information on noninterest income can be found in the “Noninterest Income” section beginning on

page 46. Certain prior period amounts have been reclassified between segments and their components (presented after Table Two) to conform to

the current period presentation.