Bank of America 2001 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

BANK OF AMERICA 2001 ANNUAL REPORT

69

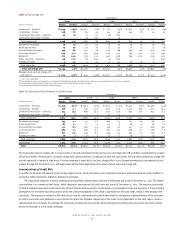

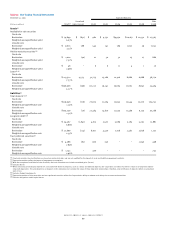

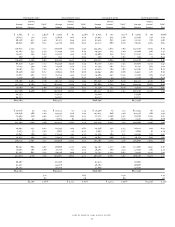

Interest Rate and Foreign Exchange Contracts

Risk management interest rate contracts and foreign exchange contracts are utilized in the Corporation’s ALM process. The Corporation maintains an

overall interest rate risk management strategy that incorporates the use of interest rate contracts to minimize significant unplanned fluctuations in

earnings that are caused by interest rate volatility. The Corporation’s goal is to manage interest rate sensitivity so that movements in interest rates do

not adversely affect net interest income. As a result of interest rate fluctuations, hedged fixed-rate assets and liabilities appreciate or depreciate in

market value. Gains or losses on the derivative instruments that are linked to the hedged fixed-rate assets and liabilities are expected to substantially

offset this unrealized appreciation or depreciation. Interest income on hedged variable-rate assets, primarily variable rate commercial loans, and interest

expense on hedged variable rate liabilities, primarily short-term time deposits, increases or decreases as a result of interest rate fluctuations. Gains

and losses on the derivative instruments that are linked to these hedged assets and liabilities are expected to substantially offset this variability in

earnings. See Note Five of the consolidated financial statements for additional information on the Corporation’s hedging activities.

Interest rate contracts, which are generally non-leveraged generic interest rate and basis swaps, options, futures and forwards, allow the Corporation

to effectively manage its interest rate risk position. In addition, the Corporation uses foreign currency contracts to manage the foreign exchange risk

associated with foreign-denominated assets and liabilities, as well as the Corporation’s equity investments in foreign subsidiaries. Table Twenty-Four

reflects the notional amounts, fair value, weighted average receive and pay rates, expected maturity and estimated duration of the Corporation’s ALM

derivatives at December 31, 2001 and 2000. Fair values are based on the last repricing and will change in the future primarily based on movements in

one-, three- and six-month LIBOR rates. Management believes the fair value of the ALM interest rate and foreign exchange portfolios should be viewed

in the context of the overall balance sheet, and the value of any single component of the balance sheet positions should not be viewed in isolation.

Consistent with the Corporation’s strategy of managing interest rate sensitivity, the net receive fixed interest rate swap position declined by

$5.8 billion to $43.0 billion at December 31, 2001. This reduction primarily occurred in the last half of 2001. Option products in the Corporation’s ALM

process may include from time to time option collars or spread strategies, which involve the buying and selling of options on the same underlying

security or interest rate index. These strategies may involve caps, floors and options on index futures contracts.

The amount of unamortized net realized deferred gains associated with closed ALM swaps was $966 million and $25 million at December 31, 2001

and 2000, respectively. The amount of unamortized net realized deferred gains associated with closed ALM options was $114 million and $95 million

at December 31, 2001 and 2000, respectively. The amount of unamortized net realized deferred losses associated with closed ALM futures and forward

contracts was $9 million and $15 million at December 31, 2001 and 2000, respectively. There were no unamortized net realized deferred gains or losses

associated with closed foreign exchange contracts at December 31, 2001 and 2000. Of these unamortized net realized deferred gains, $1.0 billion was

included in accumulated other comprehensive income at December 31, 2001.

Table 24 Asset and Liability Management Interest Rate and Foreign Exchange Contracts

December 31, 2001

Expected Maturity Average

(Dollars in millions, average

Fair After Estimated

estimated duration in years)

Value Total 2002 2003 2004 2005 2006 2006 Duration

Open interest rate contracts

Total receive fixed swaps $784 4.68

Notional value $ 64,472 $ 1,510 $ 266 $10,746 $ 8,341 $9,608 $ 34,001

Weighted average receive rate 5.74% 7.04% 8.27% 5.31% 5.79% 5.37% 5.89%

Total pay fixed swaps (322) 2.26

Notional value $ 21,445 $11,422 $4,319 $ 122 $2,664 $ 60 $ 2,858

Weighted average pay rate 3.97% 2.61% 4.21% 6.09% 6.77% 5.83% 6.34%

Basis swaps –

Notional value $ 15,700 $ – $ – $ 9,000 $ 500 $4,400 $ 1,800

Total swaps 462

Option products 105

Notional amount $ 7,000 $ – $7,000

Futures and forward rate contracts –

Notional amount $–

Total open interest rate contracts 567

Closed interest rate contracts(1) 1,071

Net interest rate contract position 1,638

Open foreign exchange contracts (285)

Notional amount $ 6,968 $ 465 $ 283 $ 576 $ 1,180 $ 2,335 $ 2,129

Total ALM contracts $1,353