Bank of America 2001 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

BANK OF AMERICA 2001 ANNUAL REPORT

59

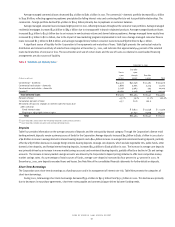

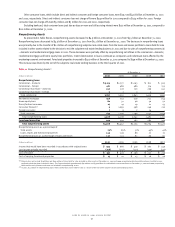

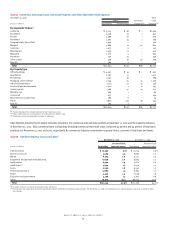

Table 13 Loans Past Due 90 Days or More and Still Accruing Interest

At December 31, 2001 At December 31, 2000

(Dollars in millions)

Amount Percent

(1)

Amount Percent

(1)

Commercial – domestic $175 .15% $141 .10%

Commercial – foreign 6.02 37.12

Commercial real estate – domestic 40 .18 16 .06

Total commercial 221 .13 194 .10

Residential mortgage 14 .02 17 .02

Direct/Indirect consumer 89 .24 89 .22

Consumer finance 24 .45 4.02

Bankcard 332 1.67 191 1.36

Total consumer 459 .28 301 .16

Total $680 .21% $495 .13%

(1) Represents amounts past due 90 days or more and still accruing interest as a percentage of loans and leases for each loan category.

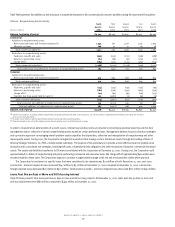

Allowance for Credit Losses

The Corporation performs periodic and systematic detailed reviews of its lending portfolios to identify inherent risks and to assess the overall

collectibility of those portfolios. The allowance on certain homogeneous loan portfolios, which generally consist of consumer loans, is based on

aggregated portfolio segment evaluations generally by loan type. Loss forecast models are utilized for these segments which consider a variety of

factors including, but not limited to historical loss experience, anticipated defaults or foreclosures based on portfolio trends, delinquencies and

credit scores, and expected loss factors by loan type. The remaining portfolios are reviewed on an individual loan basis. Loans subject to individual

reviews are analyzed and segregated by risk according to the Corporation’s internal risk rating scale. These risk classifications, in conjunction with an

analysis of historical loss experience, current economic conditions and performance trends within specific portfolio segments, and any other pertinent

information (including individual valuations on nonperforming loans in accordance with Statement of Financial Accounting Standards No. 114,

“Accounting by Creditors for Impairment of a Loan”) result in the estimation of specific allowances for credit losses. The Corporation has procedures

in place to monitor differences between estimated and actual incurred credit losses. These procedures include detailed periodic assessments by senior

management of both individual loans and credit portfolios and the models used to estimate incurred credit losses in those portfolios.

Portions of the allowance for credit losses are assigned to cover the estimated probable incurred credit losses in each loan and lease category

based on the results of the Corporation’s detail review process described above. The assigned portion continues to be weighted toward the commercial

loan portfolio, which reflected a higher level of nonperforming loans and the potential for higher individual losses. The remaining or unassigned portion

of the allowance for credit losses, determined separately from the procedures outlined above, addresses certain industry and geographic concentrations,

including global economic conditions. This procedure helps to minimize the risk related to the margin of imprecision inherent in the estimation of the

assigned allowances for credit losses. Due to the subjectivity involved in the determination of the unassigned portion of the allowance for credit losses,

the relationship of the unassigned component to the total allowance for credit losses may fluctuate from period to period. Management evaluates the

adequacy of the allowance for credit losses based on the combined total of the assigned and unassigned components.

Additions to the allowance for credit losses are made by charges to the provision for credit losses. Credit exposures deemed to be uncollectible

are charged against the allowance for credit losses. Recoveries of previously charged off amounts are credited to the allowance for credit losses.

Excluding the impact of charges related to the exit of the subprime real estate lending business, the provision for credit losses totaled $3.9 billion

for the year ended December 31, 2001 compared to $2.5 billion in 2000. The increase in the provision for credit losses from last year was primarily due to

an increase in net charge-offs, which included $210 million in charge-offs related to Enron. Additional provision expense was also recorded in 2001 to

increase the allowance for credit losses due to deterioration in credit quality and the overall uncertainty in the economy. Excluding the impact of exit-

related charges, the provision for credit losses for 2001 was $283 million in excess of net charge-offs. Total net charge-offs, excluding the impact

of exit-related charges, were $3.6 billion for the year ended December 31, 2001 compared to $2.4 billion in 2000. This increase was due to higher

charge-offs in the commercial – domestic portfolio and deterioration in credit quality stemming from the weak economic environment. Bankcard

charge-offs also increased due to growth in the portfolio, an increase in personal bankruptcy filings and a weaker economic environment.

An exit-related provision for credit losses of $395 million, combined with an existing allowance for credit losses of $240 million, was used to

write down the subprime real estate loan portfolio to estimated market value in the third quarter of 2001. This resulted in charge-offs of $635 million

in the consumer finance loan portfolio. Including the exit impact, the provision for credit losses totaled $4.3 billion and total net charge-offs were

$4.2 billion for the year ended December 31, 2001.

The nature of the process by which the Corporation determines the appropriate allowance for credit losses requires the exercise of considerable

judgment. After review of all relevant matters affecting loan collectibility, management believes that the allowance for credit losses is appropriate

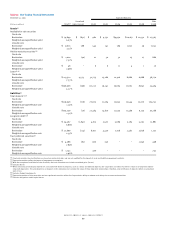

given its analysis of estimated incurred credit losses at December 31, 2001. Table Fourteen presents the activity in the allowance for credit losses for

the most recent five years.