Bank of America 2001 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

BANK OF AMERICA 2001 ANNUAL REPORT

93

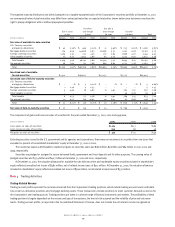

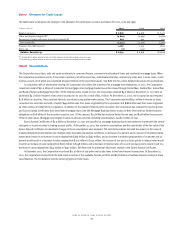

Interest rate contracts, which are generally non-leveraged generic interest rate and basis swaps, options and futures, allow the Corporation to

effectively manage its interest rate risk position. Generic interest rate swaps involve the exchange of fixed-rate and variable-rate interest payments

based on the contractual underlying notional amount. Basis swaps involve the exchange of interest payments based on the contractual underlying

notional amounts, where both the pay rate and the receive rate are floating rates based on different indices. Option products primarily consist of caps,

floors, swaptions and options on index futures contracts. Futures contracts used for ALM activities are primarily index futures providing for cash

payments based upon the movements of an underlying rate index.

The Corporation uses foreign currency contracts to manage the foreign exchange risk associated with certain foreign-denominated assets and

liabilities, as well as the Corporation’s equity investments in foreign subsidiaries. Foreign exchange contracts, which include spot, futures and forward

contracts, represent agreements to exchange the currency of one country for the currency of another country at an agreed-upon price on an agreed-upon

settlement date. Foreign exchange option contracts are similar to interest rate option contracts except that they are based on currencies rather than

interest rates. Exposure to loss on these contracts will increase or decrease over their respective lives as currency exchange and interest rates fluctuate.

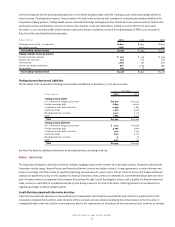

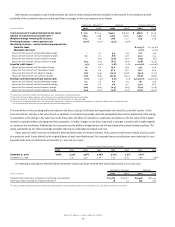

Fair Value Hedges

The Corporation uses various types of interest rate and foreign currency exchange rate derivative contracts to protect against changes in the fair

value of its fixed rate assets and liabilities due to fluctuations in interest rates and exchange rates. In 2001, the Corporation recognized in the

Consolidated Statement of Income a net loss of $6 million, which represented the ineffective portion and excluded component in assessing hedge

effectiveness of fair value hedges.

Cash Flow Hedges

The Corporation also uses various types of interest rate and foreign currency exchange rate derivative contracts to protect against changes in cash

flows of its variable rate assets and liabilities and anticipated transactions. In 2001, the Corporation recognized in the Consolidated Statement of

Income a net gain of $0.2 million, which represented the ineffective portion and excluded component in assessing hedge effectiveness of cash flow

hedges. The Corporation has determined that there are no hedging positions where it is probable that certain forecasted transactions may not occur

within the originally designated time period.

For cash flow hedges, gains and losses on derivative contracts reclassified from accumulated other comprehensive income to current period

earnings are included in the line item in the Consolidated Statement of Income in which the hedged item is recorded and in the same period the

hedged item affects earnings. Deferred net gains on derivative instruments of approximately $272 million included in accumulated other compre-

hensive income at December 31, 2001 are expected to be reclassified into earnings during the next twelve months. These net gains reclassified into

earnings are expected to increase income or reduce expense on the hedged items. The maximum term over which the Corporation is hedging its

exposure to the variability of future cash flows for all forecasted transactions (excluding interest payments on variable-rate debt) is thirty years with

an associated notional amount of $60 million. The weighted-average term over which the Corporation is hedging its exposure to this variability in

cash flows is 4.63 years.

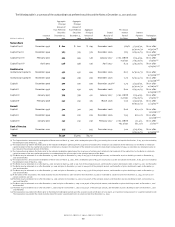

Hedges of Net Investments in Foreign Operations

The Corporation uses forward exchange contracts, currency swaps, and nonderivative hedging instruments to hedge its net investments in foreign

operations against adverse movements in foreign currency exchange rates. In 2001, net gains of $132 million related to these derivatives and non-

derivative hedging instruments were recorded as a component of the foreign currency translation adjustment in other comprehensive income. These

net gains were largely offset by losses in the Corporation’s net investments in foreign operations. In 2001, the Corporation recognized in the Consolidated

Statement of Income a net loss of $10 million, which represented the excluded component in assessing effectiveness of hedges of net investments in

foreign operations.