Bank of America 2001 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

BANK OF AMERICA 2001 ANNUAL REPORT

67

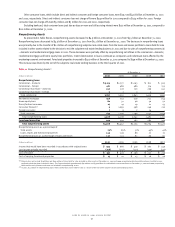

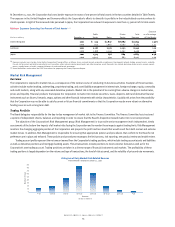

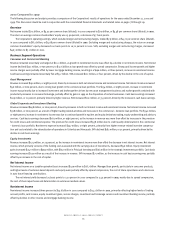

The Corporation controls and manages its commodity risk through the use of VAR limits. See Tables Twenty-One and Twenty-Two for further details.

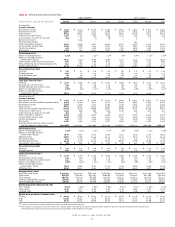

The following table indicates the maturities of non-exchange traded commodity contracts at December 31, 2001:

Asset Liability

(Dollars in millions)

Positions Positions

Maturity less than 1 year $ 3,118 $ 2,866

Maturity 1-3 years 304 172

Maturity 4-5 years 179 136

Maturity in excess of 5 years 352 461

Gross fair value of contracts $ 3,953 $ 3,635

Effects of legally enforceable master netting agreements (2,625) (2,625)

Net fair value of contracts $ 1,328 $ 1,010

Asset and Liability Management Activities

Non-Trading Portfolio

The Corporation’s Asset and Liability Management (ALM) process, managed through the Asset and Liability Committee of the Finance Committee, is

used to manage interest rate risk through structuring balance sheet portfolios and identifying and linking derivative positions to specific hedged

assets and liabilities. Interest rate risk represents the only material market risk exposure to the Corporation’s non-trading financial instruments.

To effectively measure and manage interest rate risk, the Corporation uses sophisticated computer simulations that determine the impact on net

interest income of numerous interest rate scenarios, balance sheet trends and strategies. These simulations cover the following financial instruments:

short-term financial instruments, securities, loans, deposits, borrowings and ALM derivative instruments. These simulations incorporate assumptions

about balance sheet dynamics, such as loan and deposit growth and pricing, changes in funding mix and asset and liability repricing and maturity

characteristics. Simulations are run under various interest rate scenarios to determine the impact on net income and capital. From these scenarios,

interest rate risk is quantified and appropriate strategies are developed and implemented. The overall interest rate risk position and strategies are

reviewed on an ongoing basis by senior management. Additionally, duration and market value sensitivity measures are selectively utilized where they

provide added value to the overall interest rate risk management process.

The Corporation specifically reviews the impact on net interest income of parallel and non-parallel shifts in the yield curve over different time

horizons. At December 31, 2001, the Federal Funds rate was 1.75 percent and our outlook did not anticipate additional easing from the Fed, with

continued uncertainty surrounding the timing and extent of future tightenings. As a result, the interest rate risk position of the Corporation was relatively

neutral to parallel shifts upward in the yield curve as the impact on net interest income of a 100 basis point parallel shift, up over either two months

(rapid) or twelve months (gradual) would be slightly favorable, but less than one percent. While further material declines in interest rates are unlikely,

the impact on net interest income of a 100 basis point parallel shift down would be negative three percent.

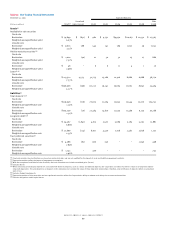

Table Twenty-Three summarizes the expected maturities, unrealized gains and losses and weighted average effective yields and rates

associated with certain of the Corporation’s significant non-trading financial instruments. Cash and cash equivalents, time deposits placed and other

short-term investments, federal funds sold and purchased, resale and repurchase agreements, commercial paper, other short-term borrowings and

foreign deposits, which are similar in nature to other short-term borrowings, are excluded from Table Twenty-Three as their respective carrying values

approximate fair values. These financial instruments generally expose the Corporation to insignificant market risk as they have either no stated maturities

or an average maturity of less than 30 days and interest rates that approximate market rates. However, these financial instruments could expose the

Corporation to interest rate risk by requiring more or less reliance on alternative funding sources, such as long-term debt. Loans held for sale are also

excluded as their carrying values approximate their fair values, generally exposing the Corporation to insignificant market risk. For further information

on the fair value of financial instruments, see Note Eighteen of the consolidated financial statements. The fair values and expected maturities for ALM

derivative instruments used for balance sheet management purposes are presented in Table Twenty-Four.