Bank of America 2001 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

BANK OF AMERICA 2001 ANNUAL REPORT

55

The Corporation’s overall objective in managing credit risk is to minimize the adverse impact of any single event or set of occurrences. To achieve

this objective, the Risk Management group works with lending officers, trading personnel and various other line personnel in areas that conduct

activities involving credit risk to maintain a credit risk profile that is diverse in terms of product type, industry concentration, geographic distribution

and borrower or counterparty concentration.

The Corporation manages credit exposure to individual borrowers and counterparties on an aggregate basis including loans and leases, securities,

letters of credit, bankers’ acceptances, derivatives and unfunded commitments. The creditworthiness of individual borrowers or counterparties is

determined by experienced personnel, and limits are established for the total credit exposure to any one borrower or counterparty. Credit limits are

subject to varying levels of approval by senior line personnel and credit risk management.

The approving credit officer assigns borrowers or counterparties an initial risk rating which is based primarily on an analysis of each borrower’s

financial capacity in conjunction with industry and economic trends. Risk ratings are subject to review and validation by the independent credit review

group. Approvals are made based upon the perceived level of inherent credit risk specific to the transaction and the counterparty and are reviewed

for appropriateness by senior line and credit risk personnel. Credits are monitored by line and credit risk management personnel for deterioration in a

borrower’s or counterparty’s financial condition which would impact the ability of the borrower or counterparty to perform under the contract. Risk

ratings are adjusted as necessary, and the Corporation seeks to reduce exposure in such situations where appropriate.

The Corporation also has a goal of managing exposure to a single borrower, industry, product-type, country or other concentration through

syndications of credits, credit derivatives, participations, loan sales and securitizations. Through the Global Corporate and Investment Banking segment,

the Corporation is a major participant in the syndications market. In a syndicated facility, each participating lender funds only its portion of the syndicated

facility, therefore limiting its exposure to the borrower. The Corporation’s strategy remains one of origination for distribution. Additionally, the SVA

discipline discourages the retention of loan assets that do not generate a positive return above the cost of risk-adjusted capital.

For consumer and small business lending, credit scoring systems are utilized to determine the relative risk of new underwritings and provide

standards for extensions of credit. Consumer portfolio credit risk is monitored primarily using statistical models and reviews of actual payment experience

in an attempt to predict portfolio behavior.

In some credit situations, the Corporation obtains collateral to support credit extensions and commitments. Generally, such collateral is in the

form of real and/or personal property, cash on deposit or other liquid instruments. In certain circumstances, the Corporation obtains real property as

security for some loans that are made on the general creditworthiness of the borrower and whose proceeds were not used for real estate-related purposes.

An independent Credit Review group provides executive management, the Board of Directors and the Credit Risk Committee with an evaluation

of portfolio quality and the effectiveness of the credit management process. The group conducts ongoing reviews of credit activities and portfolios

through transactional and process reviews, re-examining on a regular basis risk assessments for credit exposures and overall compliance with policy.

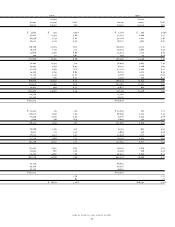

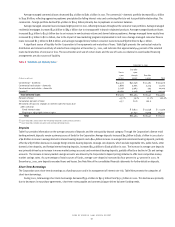

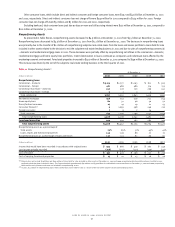

Loans and Leases Portfolio Review

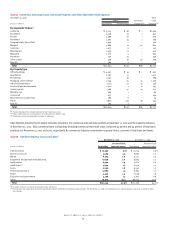

The Corporation’s credit exposure is focused in its loans and leases portfolio, which totaled $329.2 billion and $392.2 billion at December 31, 2001

and 2000, respectively. In addition, there are off-balance sheet commitments to fund loans, which totaled $295.2 billion and $315.2 billion at

December 31, 2001 and 2000, respectively. In an effort to minimize the adverse impact of any single event or set of occurrences, the Corporation

strives to maintain a diverse credit portfolio. Table Ten presents the loans and leases by category. Additional information on the Corporation’s industry,

real estate and foreign exposures can be found in the Concentrations of Credit Risk section beginning on page 61.

As a result of the exit of the auto leasing and subprime real estate lending businesses, the Corporation immediately ceased originations of auto leases

and subprime real estate loans. The Corporation intends to allow its auto lease portfolio to run off over its remaining term of three to four years. The

Corporation began to execute its exit strategy for the subprime real estate loan portfolio through securitizations and sales in the fourth quarter of 2001.

Additional information on the exit of these consumer finance businesses can be found in Notes Two and Six of the consolidated financial statements.

Table 10 Loans and Leases

December 31

2001 2000 1999 1998 1997

(Dollars in millions)

Amount Percent Amount Percent Amount Percent Amount Percent Amount Percent

Commercial – domestic $118,205 35.9% $ 146,040 37.2% $ 143,450 38.7% $ 137,422 38.5% $ 122,463 35.8%

Commercial – foreign 23,039 7.0 31,066 7.9 27,978 7.5 31,495 8.8 30,080 8.8

Commercial real estate – domestic 22,271 6.8 26,154 6.7 24,026 6.5 26,912 7.5 28,567 8.3

Commercial real estate – foreign 383 .1 282 .1 325 .1 301 .1 324 .1

Total commercial 163,898 49.8 203,542 51.9 195,779 52.8 196,130 54.9 181,434 53.0

Residential mortgage 78,203 23.8 84,394 21.5 81,860 22.1 73,608 20.6 71,540 20.9

Home equity lines 22,107 6.7 21,598 5.5 17,273 4.7 15,653 4.4 16,536 4.8

Direct/Indirect consumer 37,638 11.5 40,457 10.3 42,161 11.4 40,510 11.3 40,058 11.7

Consumer finance 5,331 1.6 25,800 6.6 22,326 6.0 15,400 4.3 14,566 4.3

Bankcard 19,884 6.0 14,094 3.6 9,019 2.4 12,425 3.5 14,908 4.4

Foreign consumer 2,092 .6 2,308 .6 2,244 .6 3,602 1.0 3,098 .9

Total consumer 165,255 50.2 188,651 48.1 174,883 47.2 161,198 45.1 160,706 47.0

Total loans and leases $329,153 100.0% $392,193 100.0% $370,662 100.0% $357,328 100.0% $342,140 100.0%