Bank of America 2001 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

BANK OF AMERICA 2001 ANNUAL REPORT

92

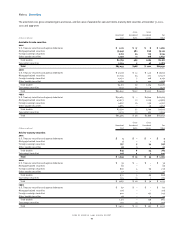

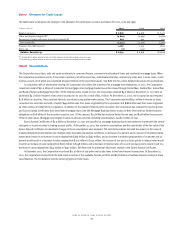

of the potential change in value of contracts over their remaining lives are considered. In managing credit risk associated with its derivative activities,

the Corporation deals primarily with commercial banks, broker-dealers and corporations. To minimize credit risk, the Corporation enters into legally

enforceable master netting arrangements, which reduce risk by permitting the closeout and netting of transactions with the same counterparty upon

occurrence of certain events. In addition, the Corporation reduces credit risk by obtaining collateral where appropriate. Required collateral levels vary

depending on the credit risk rating and the type of counterparty. Generally, the Corporation accepts collateral in the form of cash, U.S. Treasury securities,

and other marketable securities. Collateral of $10.8 billion was held on derivative assets of $22.1 billion at December 31, 2001.

The Corporation also provides credit derivatives to sophisticated customers who wish to hedge existing credit exposures or take on additional

credit exposure to generate revenue. The Corporation’s credit derivative positions at December 31, 2001 and 2000 primarily consisted of credit default

swaps and total return swaps.

A portion of the derivative activity involves exchange-traded instruments. Because exchange-traded instruments conform to standard terms and

are subject to policies set by the exchange involved, including counterparty approval, margin requirements and security deposit requirements, the credit

risk is considered minimal.

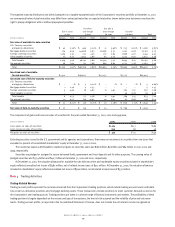

The following table presents the notional or contract and credit risk amounts at December 31, 2001 and 2000 of the Corporation’s derivative asset

positions held for trading and hedging purposes. These derivative positions are primarily executed in the over-the-counter market. The credit risk

amounts presented in the following table do not consider the value of any collateral held but take into consideration the effects of legally enforceable

master netting agreements.

Derivative Assets(1)

December 31, 2001 December 31, 2000

(2)

Contract/ Credit Contract/ Credit

(Dollars in millions)

Notional Risk Notional Risk

Interest rate contracts

Swaps $5,267,608 $ 9,550 $3,256,992 $ 3,236

Futures and forwards 1,663,109 67 1,227,537 57

Written options 678,242 – 664,108 –

Purchased options 704,159 2,165 601,828 145

Foreign exchange contracts

Swaps 140,778 2,274 61,035 1,424

Spot, futures and forwards 654,026 2,496 682,665 3,215

Written options 57,963 – 35,161 –

Purchased options 55,050 496 32,639 380

Equity contracts

Swaps 14,504 562 17,482 637

Futures and forwards 46,970 44 61,004 353

Written options 21,009 – 30,976 –

Purchased options 28,902 2,511 36,304 3,670

Commodity contracts

Swaps 6,600 1,152 9,126 1,902

Futures and forwards 2,176 – 2,098 81

Written options 8,231 – 12,603 –

Purchased options 8,219 199 10,515 228

Credit derivatives 57,182 631 40,638 206

Net replacement cost $22,147 $15,534

(1) Includes both long and short derivative positions.

(2) The amounts at December 31, 2000 do not reflect derivative positions that were off-balance sheet prior to the adoption of SFAS 133.

The average fair value of derivative assets for 2001 and 2000 was $19.8 billion and $17.9 billion, respectively. The average fair value of derivative

liabilities for 2001 and 2000 was $17.4 billion and $19.8 billion, respectively.

Asset and Liability Management (ALM) Activities

Risk management interest rate contracts and foreign exchange contracts are utilized in the Corporation’s ALM process. The Corporation maintains an

overall interest rate risk management strategy that incorporates the use of interest rate contracts to minimize significant unplanned fluctuations in

earnings that are caused by interest rate volatility. The Corporation’s goal is to manage interest rate sensitivity so that movements in interest rates do

not adversely affect net interest income. As a result of interest rate fluctuations, hedged fixed-rate assets and liabilities appreciate or depreciate in

market value. Gains or losses on the derivative instruments that are linked to the hedged fixed-rate assets and liabilities are expected to substantially

offset this unrealized appreciation or depreciation. Interest income and interest expense on hedged variable-rate assets and liabilities, respectively,

increases or decreases as a result of interest rate fluctuations. Gains and losses on the derivative instruments that are linked to these hedged assets

and liabilities are expected to substantially offset this variability in earnings.