Bank of America 2001 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2001 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

BANK OF AMERICA 2001 ANNUAL REPORT

75

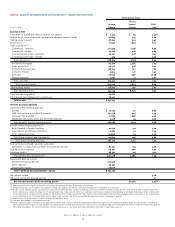

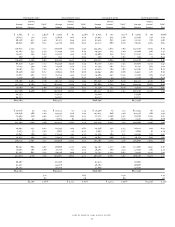

Provision for Credit Losses

The provision for credit losses was $2.5 billion in 2000 compared to $1.8 billion in 1999. The increase in the provision for credit losses was primarily due

to an increase in net charge-offs. Net charge-offs were $2.4 billion in 2000 compared to $2.0 billion in 1999. The increase was primarily driven by

deterioration of credit quality in the commercial – domestic loan portfolio and overall portfolio growth.

Noninterest Expense

Noninterest expense remained essentially unchanged at $18.6 billion in 2000 as increases due to inflation and business growth were offset by productivity

and investment initiatives.

Income Taxes

The Corporation’s income tax expense for both 2000 and 1999 was $4.3 billion. The effective tax rates for 2000 and 1999 were 36.2 percent and 35.5

percent, respectively.

Recently Issued Accounting Pronouncements

In June 2001, the Financial Accounting Standards Board (FASB) issued Statement of Financial Accounting Standards No. 141, “Business Combinations”

(SFAS 141), and Statement of Financial Accounting Standards No. 142, “Goodwill and Other Intangible Assets” (SFAS 142). SFAS 141 was effective for

business combinations initiated after June 30, 2001. SFAS 141 requires that all business combinations completed after its adoption be accounted for

under the purchase method of accounting and establishes specific criteria for the recognition of intangible assets separately from goodwill. SFAS 142

became effective for the Corporation on January 1, 2002 and primarily addresses the accounting for goodwill and intangible assets subsequent to

their acquisition. SFAS 142 requires that goodwill be recorded at the reporting unit level. Reporting units are defined as an operating segment or one

level below. The Corporation has determined its reporting units and assigned goodwill to them. The Corporation has evaluated the lives of intangible

assets as required by SFAS 142 and determined that no change will be made regarding lives upon adoption. SFAS 142 prohibits the amortization of

goodwill but requires that it be tested for impairment at least annually at the reporting unit level. The impairment test will be performed in two phases.

The first step of the goodwill impairment test, used to identify potential impairment, compares the fair value of a reporting unit with its carrying amount,

including goodwill. If the fair value of the reporting unit exceeds its carrying amount, goodwill of the reporting unit is considered not impaired; however,

if the carrying amount of a reporting unit exceeds its fair value an additional procedure must be performed. That additional procedure compares the

implied fair value of the reporting unit goodwill with the carrying amount of that goodwill. An impairment loss is recorded to the extent that the carrying

amount of goodwill exceeds its implied fair value. Management does not anticipate that an impairment charge will be recorded as a result of the adoption

of SFAS 142. Based on amortization expense recorded in 2001, the Corporation estimates that the elimination of goodwill amortization expense will

increase net income by approximately $600 million, or approximately $0.37 per common share (diluted).

In June 2001, the FASB also issued Statement of Financial Accounting Standards No. 143, “Accounting for Asset Retirement Obligations” (SFAS 143).

SFAS 143 is effective for financial statements issued for fiscal years beginning after June 15, 2002. SFAS 143 addresses financial accounting and reporting

for obligations associated with the retirement of tangible long-lived assets and the associated asset retirement costs. The Corporation does not expect

the adoption of this pronouncement to have a material impact on its results of operations or financial condition.

In August 2001, the FASB issued Statement of Financial Accounting Standards No. 144, “Accounting for the Impairment or Disposal of Long-Lived

Assets” (SFAS 144). SFAS 144 is effective for financial statements issued for fiscal years beginning after December 15, 2001. The standard addresses

financial accounting and reporting for the impairment or disposal of long-lived assets. The Corporation does not expect the adoption of this pronouncement

to have a material impact on its results of operations or financial condition.