RBS 2004 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2004 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

|

|

section

01

101

Annual Report and Accounts 2004

Operating and financial review

Operating and

financial review

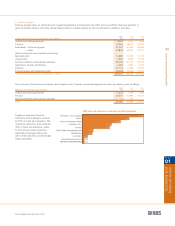

Risk elements in lending and potential problem loans

The table below sets out the Group’s loans that are classified as non-accrual, accruing past due and restructured loans (together

risk elements in lending (REIL)) or potential problem loans (PPL) as defined by the SEC in the US. The figures incorporate estimates

and are stated before deducting the value of security held or related provisions.

2004 2003 2002

REIL and PPL £m £m £m

Non-accrual loans (2) 4,780 4,432 4,175

Accrual loans past due 90 days (3) 725 642 492

Troubled debt restructurings 24 83 204

Total REIL 5,529 5,157 4,871

PPL (4) 280 591 1,183

Total REIL and PPL 5,809 5,748 6,054

Notes:

(1) The classification of a loan as non-accrual, past due 90 days or troubled debt restructuring does not necessarily indicate that the principal of the loan is uncollectable in whole

or in part. Collection depends in each case on the individual circumstances of the loan, including the adequacy of any collateral securing the loan and therefore classification of

a loan as non-accrual, past due 90 days or troubled debt restructuring does not always require that a provision be made against such a loan. In accordance with the Group’s

provisioning policy for bad and doubtful debts, it is considered that adequate provisions for the above risk elements in lending have been made.

(2) The Group’s UK banking subsidiary undertakings account for loans on a non-accrual basis from the point in time at which the collectability of interest is in significant doubt.

Certain subsidiary undertakings of the Group, principally Citizens, generally account for loans on a non-accrual basis when interest or principal is past due 90 days.

(3) Overdrafts generally have no fixed repayment schedule and consequently are not included in this category.

(4) Loans which are current as to the payment of principal and interest but in respect of which management have serious doubts about the ability of the borrowers to comply with

contractual repayment terms. Substantial security is held in respect of these loans and appropriate provisions are made in accordance with the Group’s provisioning policy for

bad and doubtful debts.

REIL increased to £5,529 million, a rise of 7% compared with

2003 partly due to acquisitions made in 2004. REIL as a

proportion of total loans and advances to customers was 1.58%

in 2004 (2003 – 2.01%; 2002 – 2.14%), reflecting active risk

management, growth in lower risk portfolios and improvements

in the economic environment in the Group’s key markets.

REIL and PPL in aggregate, as a proportion of loans and

advances also shows an improving trend, accounting for

1.66% of loans and advances to customers in 2004

(2003 – 2.24%; 2002 – 2.66%).

REIL and PPL as a percentage of loans and advances

Provisions

The Group provides for losses in its loan portfolio so as to

record impaired loans and advances at their expected ultimate

net realisable value. The objective is to set provisions based on

the current understanding of the portfolio. To reach this

understanding, retail and corporate loans and advances are

treated separately.

The Group’s retail portfolios which consist of small value, high

volume credits have highly efficient largely automated processes

for identifying problem credits and very short timescales,

typically three months, before resolution or adoption of various

recovery measures.

Corporate portfolios consist of higher value, lower volume

credits, which tend to be structured to meet individual

customers requirements. These portfolios do not have an

automated provisioning process, relying on individual expert

judgement and provisioning committees to provide the

necessary controls and oversight to identify problems.

Early and proactive management of problem exposures ensures

that credit losses are minimised. Specialised units are used for

different customer types to ensure that the appropriate risk

mitigation is taken in a timely manner.