RBS 2004 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2004 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

|

|

82

Operating and financial review

Operating and financial review continued

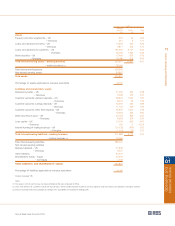

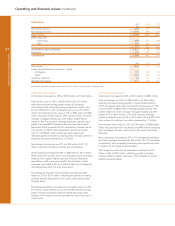

Retail Banking

2004 2003* 2002*

£m £m £m

Net interest income 3,112 2,959 2,849

Non-interest income 1,630 1,514 1,430

Total income 4,742 4,473 4,279

Direct expenses

– staff costs 834 793 729

– other 240 237 263

1,074 1,030 992

Contribution before provisions 3,668 3,443 3,287

Provisions 389 273 213

Contribution 3,279 3,170 3,074

£bn £bn £bn

Total banking assets 74.2 63.9 57.4

Loans and advances to customers – gross

– mortgages 44.1 36.6 32.1

– small business 15.2 13.8 12.5

– consumer lending 12.9 11.4 11.0

Customer deposits 70.6 66.5 61.9

Weighted risk assets 49.7 42.9 38.8

* prior periods have been restated to reflect the transfer in 2004 of certain activities from Wealth Management.

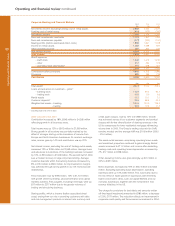

2004 compared with 2003

The division continued to achieve strong volume growth across

all key product areas – in particular mortgages, loans and

savings – supported by increased customer numbers. As a

result, income increased by 6% or £269 million to £4,742 million,

and contribution by 3% or £109 million to £3,279 million.

Net interest income rose by 5% or £153 million to £3,112

million, reflecting strong growth in lending and deposits which

more than offset the impact of business mix – particularly

strong growth in low risk mortgage lending – and the impact of

lower margin in some areas, especially unsecured lending.

Average loans to customers, excluding mortgages, grew by

12% or £2.8 billion to £26.5 billion. Average mortgage lending

grew by 21% or £7.0 billion to £40.7 billion. Both mortgage and

non-mortgage lending have evidenced a slowdown in growth

in the second half of the year. Average customer deposits

increased by 8% or £4.9 billion to £66.0 billion.

Non-interest income rose by 8% or £116 million to £1,630

million. This reflected higher fee income associated with strong

asset growth in both personal and business sectors together

with increased volumes of money transmission activity.

Direct expenses increased by 4% or £44 million to £1,074

million. Staff expenses increased 5% or £41 million to £834

million, principally due to the deployment of an additional one

thousand customer facing staff in the NatWest network. The

increase in other expenses was 1% or £3 million, reflecting

rigorous cost management.

The charge for provisions for bad and doubtful debts increased

by £116 million to £389 million. The increased charge reflects

the anticipated increase in delinquency rates in the NatWest

portfolio following growth in unsecured lending in recent years.

NatWest credit experience is now broadly consistent with the

RBS portfolio which has been stable for a number of years. As

reported in the first half, there has also been a higher incidence

of fraud which has led to some deterioration in recovery rates.

The overall quality of the loan portfolio, the majority of which is

mortgage lending, as measured by probability of default,

remained in line with expectations.