RBS 2004 Annual Report Download - page 143

Download and view the complete annual report

Please find page 143 of the 2004 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

|

|

section

03

141

Annual Report and Accounts 2004

Accounting policies

Financial

statements

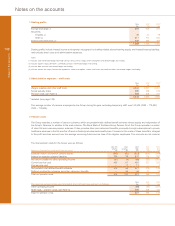

7 General insurance

General insurance comprises short-duration contracts and

include principally property and liability insurance contracts.

Due to the nature of the products sold – retail based property

and casualty, motor, home and personal health insurance

contracts – the insurance protection is provided on an even

basis throughout the term of the policy.

In calculating operating profit from general insurance activities,

premiums (net of reinsurance premiums) are recognised in the

accounting period in which they begin. Unearned premiums

represent the proportion of the net premiums that relate to

periods of insurance after the balance sheet date and are

calculated over the period of exposure under the policy, on a

daily basis, 24th’s basis or allowing for the estimated incidence

of exposure under policies which are longer than twelve

months. Provision is made where necessary for the estimated

amount required over and above unearned premiums net of

reinsurance, including that in respect of future written business

on discontinued lines under the run-off of delegated underwriting

authority arrangements. It is designed to meet future claims

and related expenses and is calculated across related classes

of business on the basis of a separate carry forward of

deferred acquisition expenses after making allowance for

investment income.

Acquisition expenses relating to new and renewed business for

all classes are deferred over the period during which the

premiums are unearned. The principal acquisition costs so

deferred are commissions payable, direct advertising expenditure,

costs associated with the telesales and underwriting staff and

prepaid claims handling costs in respect of delegated claims

handling arrangements for claims which are expected to occur

after the balance sheet date.

Claims (net of reinsurance) are recognised in the accounting

period in which the loss occurs. Provision is made for the full

cost (net of reinsurance) of settling outstanding claims at the

balance sheet date, including claims estimated to have been

incurred but not yet reported at that date, and claims handling

expenses.

8 Long-term life assurance business

The Group’s long-term assurance business includes whole-life,

guaranteed renewable term life, endowment, annuity and

universal life contracts that are expected to remain in force for

an extended period of time, generally five to forty years.

The value placed on the Group’s long-term life assurance

business comprises the net assets of the Group’s life

assurance subsidiaries, including its interest in the surpluses

retained within the long-term assurance funds, and the present

value of profits inherent in in-force policies. In calculating the

value of in-force policies, future surpluses expected to emerge

are estimated using appropriate assumptions as to future

mortality, persistency and levels of expenses, which are then

discounted at a risk-adjusted rate. Changes in this value,

which is determined on a post-tax basis, are included in

operating profit, grossed up at the underlying rate of taxation.

Long-term assurance assets attributable to policyholders are

valued on the following bases: equity shares and debt

securities at market price; investment properties and loans at

valuation. These assets are held in the life funds of the Group’s

life assurance companies, and although legally owned by

them, the Group only benefits from these assets when surpluses

are declared. To reflect the distinct nature of the long-term

assurance assets, they are shown separately on the consolidated

balance sheet, as are liabilities attributable to policyholders.

The Group has reinsured contracts that transfer significant

insurance risk. Within net assets, the reinsurance cash flows

are recognised when they become payable. For most contracts

this effectively spreads the cost of reinsurance over the life of

the reinsured contracts. In some cases, the acquisition costs

are financed by the reinsurer offering a nil premium payment

period. In these cases, the acquisition costs incurred on the

underlying insurance contracts are compared with the benefit

arising with respect to the nil premium paying period on the

reinsurance contract.

9 Loans and advances

The Group makes provisions for bad and doubtful debts,

through charges to the profit and loss account, so as to record

impaired loans and advances at their expected ultimate net

realisable value.

Specific provisions are made against individual loans and

advances that the Group no longer expects to recover in full.

For the Group’s portfolios of smaller balance homogeneous

advances, such as credit card receivables, specific provisions

are established on a portfolio basis taking into account the

level of arrears, security and past loss experience. For loans

and advances that are individually assessed, the specific

provision is determined from a review of the financial condition

of the borrower and any guarantor and takes into account the

nature and value of any security held.

The general provision is made to cover bad and doubtful debts

that have not been separately identified at the balance sheet

date but are known to be present in any portfolio of advances.

The level of general provision is determined in the light of past

experience, current economic and other factors affecting the

business environment and the Group’s monitoring and control

procedures, including the scope of specific provisioning

procedures.

Specific and general provisions are deducted from loans and

advances. When there is significant doubt that interest

receivable can be collected, it is excluded from the profit and

loss account and credited to an interest suspense account.

Loans and advances and suspended interest are written off in

part or in whole when there is no realistic prospect of recovery.

10 Taxation

Provision is made for taxation at current enacted rates on

taxable profits taking into account relief for overseas taxation

where appropriate. Timing differences arise where gains and

losses are accounted for in different periods for financial

reporting purposes and for taxation purposes. Deferred

taxation is accounted for in full for all such timing differences,

except in relation to revaluations of fixed assets where there is

no commitment to dispose of the asset, taxable gains on sales