RBS 2004 Annual Report Download - page 157

Download and view the complete annual report

Please find page 157 of the 2004 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

|

|

section

03

155

Annual Report and Accounts 2004

Notes on the accounts

Financial

statements

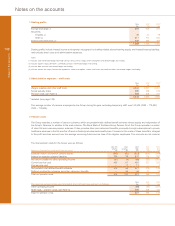

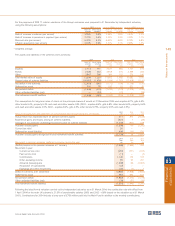

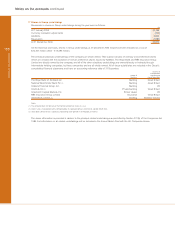

13 Provisions for bad and doubtful debts

2004 2003

Specific General Total Specific General Total

£m £m £m £m £m £m

At 1 January 3,363 566 3,929 3,330 597 3,927

Currency translation and other adjustments (22) (76) (98) (23) (39) (62)

Acquisition of subsidiary 222 68 290 44 6 50

Amounts written off (1,468) –– (1,468) (1,519) — (1,519)

Recoveries of amounts written off in previous periods 147 –– 147 72 — 72

Charge to profit and loss account 1,412 16 1,428 1,459 2 1,461

At 31 December 3,654 574 4,228 3,363 566 3,929

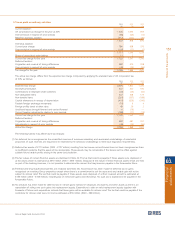

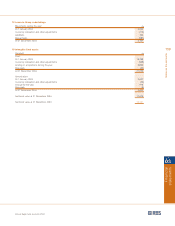

14 Interest in suspense

In certain cases, interest may be charged to a customer’s account but, because its recoverability is in doubt, not recognised in the

Group’s consolidated profit and loss account. Such interest is held in a suspense account and netted off against loans and advances

in the consolidated balance sheet.

2004 2003

£m £m

Loans and advances on which interest is being placed in suspense:

– before specific provisions 2,558 1,938

– after specific provisions 1,203 930

Loans and advances on which interest is not being applied:

– before specific provisions 2,225 2,494

– after specific provisions 850 980

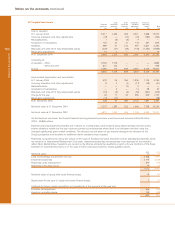

(ii) Mortgage securitisations – following the acquisition of First

Active in 2004, the Group is party to a number of mortgage

securitisations that qualify for linked presentation. Mortgages

have been transferred to special purpose vehicles, held

ultimately by charitable trusts, funded principally through the

issue of floating rate notes. The Group is not obliged, and does

not intend, to support losses that may be suffered by the note

holders. There are no arrangements for the Group to

repurchase the mortgages. The note holders have agreed that

they will be paid, as to interest and principal, only to the extent

that sufficient funds are generated by the mortgage loans and

their underlying security. The Group has entered into arm's

length fixed/floating interest rate swaps with the securitisation

vehicles and provides mortgage management and agency

services to the vehicles. On repayment of the financing, any

further amounts generated by the mortgages will be paid to

the Group. At 31 December 2004, mortgages of £1,519 million

are subject to non-recourse finance of £1,479 million. During

the year the Group recognised net income of £26 million

comprising interest receivable of £72 million less interest

payable and other expenses of £46 million.

(iii) Securitisation of housing association loans – the Group has

arranged the securitisation of housing association loans. The

loans were acquired by special purpose vehicles, held ultimately

by charitable trusts, funded principally through the issue of

floating and fixed rate notes. The Group is not obliged, and

does not intend, to support losses that may be suffered by the

note holders. The note holders have agreed that they will be

paid, as to interest and principal, only to the extent that sufficient

funds are generated by the loans and their underlying security.

Any proceeds from the loans in excess of the amounts required

to service and repay the notes are payable to the Group after

deduction of expenses. At 31 December 2004, gross loans

amounted to £1,412 million (2003 – £1,450 million) and notes

held by third parties were £1,012 million (2003 – £861 million).

During the year the Group recognised net income of £37 million

(2003 – £39 million; 2002 – £40 million) comprising interest

receivable of £116 million (2003 – £119 million; 2002 – £118

million) less interest payable and other expenses of £79 million

(2003 – £80 million; 2002 – £78 million).

(iv) Mortgage banking activities - the Group sells originated

mortgage loans to US Agencies in return for securities

backed by these loans and guaranteed by the Agency whilst

retaining the rights to service the mortgages. These securities

may be subsequently sold. The purchaser has recourse to the

Group for losses up to pre-determined levels on certain

designated mortgages. The Group is not obliged, and does

not intend, to support losses that may be suffered by the

Agencies. Under the terms of the sale agreements, the

Agencies have agreed to seek repayment only from the cash

from the mortgage loans. Once the securities exchanged for the

loans have been sold the Group's exposure is restricted to the

amount of the recourse and the transaction qualifies for the

linked presentation. At 31 December 2004 mortgages

amounting to £472 million had been sold with recourse and

the related securities sold. Recourse is limited to a maximum

of £6 million. No amounts were recognised in the profit and loss

account except for income from the servicing of the mortgages.

(v) Loan transfer – during 2004, loans originated by the Group

and another bank were transferred to a special purpose

vehicle which funded the purchase through the issue of notes.

The Group is not obliged, and does not intend, to support

losses that may be suffered by the note holders. There are no

arrangements for the Group to repurchase the loan. The note

holders have agreed that they will be paid, as to interest and

principal, only to the extent that sufficient funds are generated

by the loans. At 31 December 2004, the gross loan amounted

to £301 million and the non-recourse financing of £301 million.

Gross and net income in 2004 were less than £1 million.