RBS 2004 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2004 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

|

|

section

01

Operating and

financial review

71

Annual Report and Accounts 2004

Operating and financial review

Analysis of results

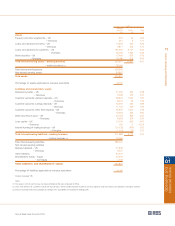

Net interest income 2004 2003 2002

£m £m £m

Interest receivable 16,696 13,998 13,561

Interest payable (7,488) (5,697) (5,712)

Net interest income 9,208 8,301 7,849

%% %

Gross yield on interest-earning assets of the banking business 5.30 5.00 5.41

Cost of interest-bearing liabilities of the banking business (2.70) (2.32) (2.70)

Interest spread of the banking business 2.60 2.68 2.71

Benefit from interest-free funds 0.32 0.29 0.42

Net interest margin of the banking business 2.92 2.97 3.13

Yields, spreads and margins of the banking business % %%

Gross yield

Group 5.30 5.00 5.41

UK 5.70 5.20 5.56

Overseas 4.38 4.44 4.97

Interest spread

Group 2.60 2.68 2.71

UK 2.68 2.68 2.72

Overseas 2.48 2.71 2.69

Net interest margin

Group 2.92 2.97 3.13

UK 2.96 2.95 3.14

Overseas 2.83 3.02 3.09

The Royal Bank of Scotland plc base rate 4.38 3.69 4.00

London inter-bank three month offered rates:

Sterling 4.64 3.74 4.06

Eurodollar 1.62 1.22 1.80

Euro 2.11 2.33 3.32

Notes:

(1) Gross yield is the interest rate earned on average interest-earning assets of the banking business.

(2) Interest spread is the difference between the gross yield and the interest rate paid on average interest-bearing liabilities of the banking business.

(3) Net interest margin is net interest income of the banking business as a percentage of average interest-earning assets of the banking business.

2004 compared with 2003

Group – The net interest margin decreased from 2.97% to 2.92%.

The interest spread declined reflecting principally a change in

mix towards relatively lower margin mortgage business including

the acquisition of First Active. This was partially offset by an

increase in the benefit from interest-free funds due to increased

volumes and movements in interest rates.

UK – The UK net interest margin increased slightly from 2.95% to

2.96%. An increase in the benefit from interest-free funds, due to

movements in interest rates, and improvements in corporate

lending margins were largely offset by growth in the mortgage

business.

Overseas – The Overseas net interest margin decreased from

3.02% to 2.83%. This reduction reflected the continued

tightening of asset spreads in the US, together with the growth in

mortgage business following the acquisition of First Active.

Higher volumes together with movements in interest rates led to

an increase in the benefit of interest-free funds.

2003 compared with 2002

Net interest income increased by 6%, £452 million, to £8,301

million. Average interest-earning assets of the Group’s banking

business increased by 12%, £29.1 billion, to £279.7 billion.

Within this, average loans and advances to customers were up

12%, £23.3 billion, to £213.3 billion due to growth in both

corporate and personal lending.

Interest spread for the Group as a whole decreased from 2.71%

to 2.68%. Interest-free balances fell partly due to the outcome

of the Competition Commission inquiry into SME banking.

This, together with the lower interest rate environment

contributed to the reduction in the benefit of interest-free funds

from 0.42% to 0.29% giving a decline in net interest margin

from 3.13% to 2.97%.

UK – Interest spread decreased from 2.72% to 2.68% with

product margins remaining stable despite growth in the

relatively lower margin mortgage business. The reduced

benefit of interest-free funds due to the rate and volume

impact described above resulted in the decrease in net

interest margin from 3.14% to 2.95%.

Overseas – Interest spread increased from 2.69% to 2.71%.

Asset spreads tightened in the US due to lower interest rates;

however, this was more than offset by overall mix and volume

improvements elsewhere. Lower interest rates led to a

reduction in the benefit from interest-free funds, resulting

in the decline in net interest margin from 3.09% to 3.02%.