RBS 2004 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2004 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

|

|

68

Operating and financial review

Operating and financial review continued

2004 compared with 2003

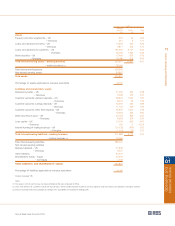

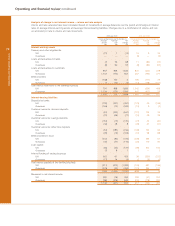

Profit

Profit before tax, goodwill amortisation and integration costs

increased by 15% or £1,033 million, from £7,068 million to

£8,101 million. At constant exchange rates the increase was

18% or £1,278 million.

Profit before tax was up 14%, from £6,076 million to £6,917

million.

The Group made a number of acquisitions during 2004 which

had a bearing on the year's results. These included:

In January 2004, Ulster Bank completed the acquisition of First

Active plc, for a cash consideration of 887 million.

In March 2004, RBS completed the purchase of the credit card

business of People's Bank in the US.

In August 2004, Citizens completed the acquisition of Charter

One Financial, Inc. for a cash consideration of US$10.1 billion.

The Group has adopted Financial Reporting Standard 17

‘Retirement Benefits’ (“FRS 17”) – the standard that replaces

SSAP24 ‘Pension Costs’. The effect on prior years of adopting

FRS 17 is shown on page 139.

Total income

The Group achieved strong growth in income during 2004.

Total income was up 18% or £3,473 million to £22,754 million.

Excluding acquisitions and at constant exchange rates, total

income was up by 11%, £2,004 million.

Net interest income increased by 11% to £9,208 million and

represents 40% of total income (2003 – 43%). Excluding

acquisitions and at constant exchange rates, net interest

income was up 8%. Average loans and advances to customers

and average customer deposits grew by 19% and 10%

respectively.

Non-interest income increased by 23% to £13,546 million and

represents 60% of total income (2003 – 57%). Excluding

acquisitions and at constant exchange rates, non-interest

income was up 13%. There was good growth in transmission

income and other fees, up 17% while general insurance

premium income increased by 58%, reflecting organic growth

and the acquisition of Churchill in September 2003. Gross

income from rental assets grew by 18%, reflecting strong

growth in operating lease assets.

Net interest margin

The Group's net interest margin at 2.92% was in line with

expectations. Excluding the acquisition of First Active, the

Group's net interest margin was down 0.03% from 2.97% in

2003, principally as a result of strong organic growth in

mortgage lending and the increased funding cost of rental

assets, the income from which is included in other income.

Operating expenses

Operating expenses, excluding goodwill amortisation and

integration costs, rose by 13% to £9,662 million to support the

strong growth in business volumes. Excluding acquisitions and

at constant exchange rates, operating expenses were up by

9%, £739 million.

Cost:income ratio

The Group's ratio of operating expenses (excluding goodwill

amortisation and integration costs and after netting operating

lease depreciation against rental income) to total income

improved further to 40.8% from 42.6%. Excluding Charter One,

the Group's cost:income ratio was 40.6%.

Net insurance claims

General insurance claims, after reinsurance, increased by 59%

to £3,480 million. Excluding Churchill, the increase was 20%,

consistent with volume growth and business mix.

Provisions

The profit and loss charge for bad and doubtful debts and

amounts written off fixed asset investments was £1,511 million

compared with £1,494 million in 2003. The charge for

provisions in 2004 represented 0.51% of gross loans and

advances to customers (excluding reverse repurchase

agreements), compared with 0.64% in 2003.

Credit quality

Credit quality remains strong with no material change during

2004 in the distribution by grade of the Group's total risk assets.

The ratio of risk elements in lending to gross loans and

advances to customers improved to 1.58% (2003 – 2.01%).

Risk elements in lending and potential problem loans

represented 1.66% of gross loans and advances to customers

(2003 – 2.24%).

Provision coverage of risk elements in lending and potential

problem loans improved to 73% (2003 – 68%).

Integration

Integration costs in 2004 were £269 million principally relating

to the integration of Churchill and the acquisitions by Citizens.

Earnings and dividends

Basic earnings per ordinary share increased by 79%, from

76.9p to 138.0p. The final dividend on the Additional Value

Shares (“AVS”) paid in December 2003 reduced earnings per

ordinary share for that year by 49.9p. Adjusting for this and for

goodwill amortisation and integration costs, earnings per

ordinary share increased by 10%, from 157.2p to 172.5p.

A final dividend of 41.2p per ordinary share is recommended,

making a total for the year of 58.0p per share, an increase of

15%. If approved, the final dividend will be paid on 3 June

2005 to shareholders registered on 11 March 2005. The total

dividend is covered 2.9 times by earnings before goodwill

amortisation and integration costs.