RBS 2004 Annual Report Download - page 191

Download and view the complete annual report

Please find page 191 of the 2004 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

|

|

section

03

189

Annual Report and Accounts 2004

Notes on the accounts

Financial

statements

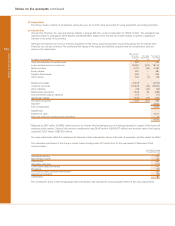

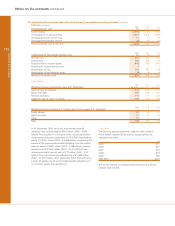

(n) Share-based compensation

Under UK GAAP, no compensation expense is recognised

for the Group’s executive share option schemes, under

which options are granted at the higher of nominal value

and market value on the date of grant and for the Group’s

Sharesave schemes, under which employees are granted

options at a 20% discount to market value at date of grant.

Under US GAAP, the compensation expense based on the

options’ intrinsic value is charged to the profit and loss

account over the period to their average vesting date.

(o) Consolidation

UK GAAP requires consolidation of entities controlled by an

enterprise where control means the enterprise’s ability to

direct the financial and operating policies of an entity with

a view to gaining economic benefits. US GAAP requires

consolidation by the primary beneficiary of a variable

interest entity (“VIE”). An enterprise is the primary

beneficiary of a VIE if it will absorb a majority of the

entity’s expected losses, receive a majority of the entity’s

expected residual returns, or both.

(p) Acceptances

Acceptances outstanding and the matching customers’

liabilities are not reflected in the consolidated balance

sheet, but are disclosed as memorandum items. Under US

GAAP, acceptances outstanding and the matching customers’

liabilities are reflected in the consolidated balance sheet.

(q) Offset arrangements

Under UK GAAP, debit and credit balances with the same

counterparty are aggregated into a single item where there

is a right to insist on net settlement and the debit balance

matures no later than the credit balance. Under US GAAP,

agreements and balances with the same counterparty may

be offset only where they have the same settlement date

specified at inception and there is an intention to set off.

(r) Deferred taxation

Accounting for deferred tax under UK GAAP is consistent

with US GAAP except that deferred tax is not recognised

under UK GAAP on certain timing differences resulting from

the roll-over of gains on disposal of properties, but is

provided under US GAAP on such differences.

Recent developments in US GAAP

The FASB issued SFAS 153 ‘Exchanges of Nonmonetary

assets, an amendment of APB Opinion No. 29’ in December

2004. SFAS 153 provides for a general exception from fair

value measurement for exchanges of nonmonetary assets that

do not have commercial substance. The Statement is effective

for fiscal years beginning after 15 June 2005 and is not

expected to affect the Group's US GAAP reporting.

In December 2004, the FASB issued SFAS 123 (revised 2004)

‘Share-Based Payment’ which requires compensation costs

related to share-based payment transactions to be recognised

in the financial statements. The compensation cost will be

based on the grant-date fair value of the equity issued and will

be recognised over the period that an employee provides

service in exchange for the award. SFAS 123 (revised 2004)

would be effective for the Group from 1 January 2006. Entities

that use the fair value method for either recognition or

disclosure under SFAS 123 will apply the revised Statement

using a modified version of prospective application whereby

for that portion of outstanding awards for which the requisite

service has not yet been rendered, compensation cost will be

based on the grant-date fair value calculated under SFAS 123

for either recognition or pro forma disclosures. For periods

before the effective date, entities may elect to apply a modified

version of retrospective application under which financial

statements for prior periods are adjusted on a basis consistent

with the pro forma disclosures required by SFAS 123. The

Group currently makes pro forma disclosures of the effect on

net income of compensation costs determined under the fair

value method of SFAS 123.