RBS 2004 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2004 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

|

|

section

01

Operating and

financial review

75

Annual Report and Accounts 2004

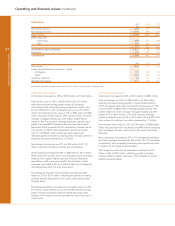

Operating and financial review

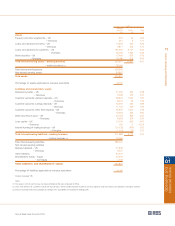

2004 compared with 2003

Non-interest income increased by £2,566 million, 23% to

£13,546 million and represents 60% of total income (2003 –

57%). Excluding acquisitions and at constant exchange rates,

non-interest income was up 13%.

Within non-interest income, fees and commissions receivable

increased by 17% or £941 million, to £6,634 million. This

reflected strong growth in lending, transmission and card

related fees together with increased insurance brokerage

and ATM income.

Fees and commissions payable increased by £617 million to

£1,954 million reflecting higher brokerage costs in CBFM due

to greater volumes of trading and structuring business and

fees paid in Retail Direct in support of higher volumes.

Commissions payable to brokers and intermediaries in the

general insurance business were up reflecting the acquisition

of Churchill in September 2003.

Dealing profits at £1,988 million were up £195 million, 11% on

2003. Growth was achieved across all customer segments and

product classes with further diversification of dealing revenues

in the US to compensate for lower residential refinancing

volume than the previous year.

Other operating income increased by 12% to £1,855 million.

This was principally due to higher gross income from rental

assets reflecting strong growth in operating lease assets.

General insurance premium income, after reinsurance, rose by

58%, or £1,821 million to £4,944 million reflecting organic

growth and the acquisition of Churchill. Excluding Churchill, the

growth was 17% reflecting volume growth in motor and home

insurance products.

2003 compared with 2002

Non-interest income increased by 20%, or £1,813 million, to

£10,980 million. Non-interest income represented 57% of total

income. Excluding general insurance premium income, non-

interest income rose by 9% or £643 million to £7,857 million

reflecting strong performances in CBFM, up 18% or £670

million and Retail Direct, up 17%, or £145 million.

Within non-interest income, fees and commissions receivable

increased by 8% or £444 million, to £5,693 million. This

reflected an increase in lending and transmission fees, and

good growth in insurance brokerage, cards related fees and

ATM income.

Fees and commissions payable increased by £372 million to

£1,337 million reflecting higher brokerage costs in CBFM, fees

paid in Retail Direct in support of higher volumes and

commissions payable to brokers and intermediaries following

the acquisition of Churchill.

Dealing profits at £1,793 million were up £331 million, 23% on

2002. This reflected strong growth in volumes in all product

areas. The performance in the first half of the year benefited

from the unusually high levels of demand for mortgage backed

securities in the US.

Other operating income increased by 17% to £1,650 million.

This was due to growth in income from rental assets

(comprising operating lease assets and investment properties)

and higher investment securities gains.

General insurance premium income, after reinsurance, rose by

60%, or £1,170 million to £3,123 million. Excluding the acquisition

of Churchill Insurance the growth was 25% or £490 million

reflecting volume growth in motor and home insurance products.

Non-interest income

2004 2003* 2002*

£m £m £m

Dividend income 79 58 58

Fees and commissions receivable 6,634 5,693 5,249

Fees and commissions payable (1,954) (1,337) (965)

Dealing profits 1,988 1,793 1,462

Other operating income 1,855 1,650 1,410

8,602 7,857 7,214

General insurance premium income

Earned premiums 5,357 3,627 2,442

Reinsurance (413) (504) (489)

4,944 3,123 1,953

13,546 10,980 9,167

* restated (see page 139)