RBS 2004 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2004 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

|

|

80

Operating and financial review

Operating and financial review continued

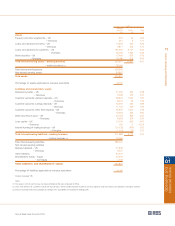

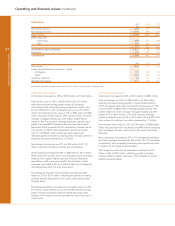

Corporate Banking and Financial Markets

2004 2003 2002

£m £m £m

Net interest income excluding funding cost of rental assets 2,959 2,653 2,631

Funding cost of rental assets (414) (329) (282)

Net interest income 2,545 2,324 2,349

Fees and commissions receivable 1,723 1,537 1,394

Fees and commissions payable (277) (220) (157)

Dealing profits (before associated direct costs) 1,855 1,661 1,338

Income on rental assets 1,282 1,088 931

Other operating income 381 307 197

Non-interest income 4,964 4,373 3,703

Total income 7,509 6,697 6,052

Direct expenses

– staff costs 1,642 1,410 1,230

– other 412 394 375

– operating lease depreciation 610 518 461

2,664 2,322 2,066

Contribution before provisions 4,845 4,375 3,986

Provisions 580 755 725

Contribution 4,265 3,620 3,261

£bn £bn £bn

Total assets* 265.3 219.0 203.4

Loans and advances to customers – gross*

– banking book 114.9 99.3 92.1

– trading book 10.0 5.0 3.6

Rental assets 11.2 10.1 7.0

Customer deposits* 74.9 68.6 62.2

Weighted risk assets – banking 160.9 140.0 125.2

Weighted risk assets – trading 16.9 12.6 11.3

* excluding repos and reverse repos

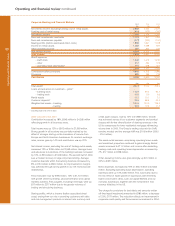

2004 compared with 2003

Contribution increased by 18%, £645 million to £4,265 million

reflecting growth in all business areas.

Total income was up 12% or £812 million to £7,509 million.

Strong growth in all locations was partially masked by the

effect of stronger sterling on the translation of income from

Europe and North American businesses. At constant exchange

rates, income grew by 14% and contribution was up 20%.

Net interest income, excluding the cost of funding rental assets,

increased 12% or £306 million to £2,959 million. Average loans

and advances to customers of the banking business increased

by 10% or £9.5 billion to £103.8 billion. The second half of 2004

saw a modest recovery in large corporate lending. Average

customer deposits within the banking business increased by

8% or £5.0 billion to £66.0 billion. An improvement in margins

was achieved through strong growth in our UK mid-corporate

relationships.

Fees receivable rose by £186 million, 12% to £1,723 million

with growth driven by lending, structured finance and capital

markets activities. Fees payable, including brokerage, were up

£57 million to £277 million due to the greater volumes of

trading and structuring business.

Dealing profits, which is income (before associated direct

costs) arising from our role in providing customers with debt

and risk management products in interest rate, currency and

credit asset classes, rose by 12% to £1,855 million. Growth

was achieved across all our customer segments and product

classes with further diversification of dealing revenues in the

US to compensate for lower residential mortgage refinancing

volume than in 2003. The Group's trading value-at-risk (VaR)

remains modest and the average VaR was £10.8 million (2003

– £9.4 million).

The asset rental business, comprising operating lease assets

and investment properties continued to grow strongly. Rental

assets increased to £11.2 billion and income after deducting

funding costs and operating lease depreciation increased by

7%, £17 million to £258 million.

Other operating income also grew strongly, up £74 million or

24% to £381 million.

Direct expenses increased by 15% or £342 million to £2,664

million. Excluding operating lease depreciation, operating

expenses were up 14%, £250 million. This was mainly due to

the mix effect of faster growth in businesses with inherently

higher cost:income ratios, such as Capital Markets and our

overseas businesses, together with the investment in new

revenue initiatives in the US.

The charge for provisions for bad debts and amounts written

off fixed asset investments amounted to £580 million, a decrease

of 23%, £175 million. The reduction reflects an improvement in

corporate credit quality and the economic environment in 2004.