Regions Bank 2008 Annual Report Download - page 149

Download and view the complete annual report

Please find page 149 of the 2008 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

approximately $39 million. During 2009, the Company anticipates filing amended state and local income tax

returns to reflect the agreement reached with the IRS for tax years 1999-2006. If completed and accepted by the

states, the gross unrecognized tax benefits could decrease by approximately $55 million.

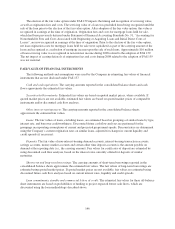

NOTE 22. DERIVATIVE FINANCIAL INSTRUMENTS AND HEDGING ACTIVITIES

Regions maintains positions in derivative financial instruments to manage interest rate risk, to facilitate

asset/liability management strategies and to serve the risk management needs of customers. These derivative

instruments include forward rate contracts, Eurodollar futures, interest rate swaps, put and call option contracts,

interest rate floors, and foreign currency contracts. For those derivative contracts that qualify for hedge

accounting, according to FAS 133, Regions designates hedging instruments as either a fair value or cash flow

hedge. Derivative contracts that do not qualify for hedge accounting are classified as trading. The accounting

policies associated with derivative financial instruments are discussed further in Note 1 to the consolidated

financial statements.

Forward rate contracts are commitments to buy or sell financial instruments at a future date at a specified

price or yield. Regions primarily enters into forward rate contracts on market instruments, which expose Regions

to market risk associated with changes in the value of the underlying financial instrument, as well as the credit

risk that the counterparty will fail to perform. Eurodollar futures are futures contracts on three-month Eurodollar

deposits. Eurodollar futures subject Regions to market risk associated with changes in interest rates. Because

futures contracts are cash settled daily, there is minimal credit risk associated with Eurodollar futures. Interest

rate swaps are agreements to exchange interest payments based upon notional amounts. Interest rate swaps

subject Regions to market risk associated with changes in interest rates, as well as the credit risk that the

counterparty will fail to perform. Option contracts involve rights to buy or sell financial instruments on a

specified date or over a period at a specified price. These rights do not have to be exercised. Some option

contracts such as interest rate floors, involve the exchange of cash based on changes in specified indices. Interest

rate floors are contracts to hedge interest rate declines based on a notional amount. Interest rate floors subject

Regions to market risk associated with changes in interest rates, as well as the credit risk that the counterparty

will fail to perform. Foreign currency contracts involve the exchange of one currency for another on a specified

date and at a specified rate. These contracts are executed on behalf of the Company’s customers and are used to

manage fluctuations in foreign exchange rates. The Company is subject to the credit risk that another party will

fail to perform.

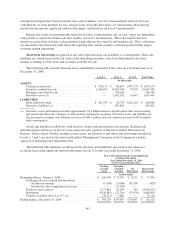

HEDGING DERIVATIVES

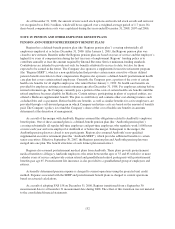

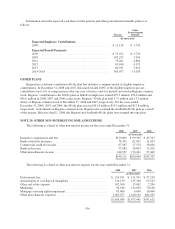

The following tables summarize the hedging derivative positions utilized by Regions to manage interest rate

risk and facilitate asset/liability strategies as of December 31:

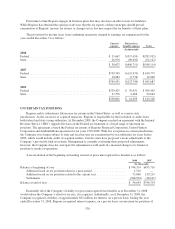

2008

Notional

Amount

Fair

Value

Hedged

Item

Weighted-

Average

Maturity

Pay

Structure

(Dollars in millions)

Fair Value Hedges

Interest rate swaps (a) ................................ $ 5,775 $292.0 Debt 2.6 yrs. Variable

Cash Flow Hedges

Interest rate swaps (a) ................................ $ 7,350 $313.0 Loans 1.9 yrs. Variable

Interest rate options .................................. 3,500 115.9 Loans 1.5 yrs. n/a

Eurodollar futures ................................... 10,000 — Loans 0.3 yrs. n/a

$20,850 $428.9

(a) The weighted-average pay and receive rates on interest rate swaps were 2.45% and 4.58%, respectively.

139