Regions Bank 2008 Annual Report Download - page 156

Download and view the complete annual report

Please find page 156 of the 2008 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

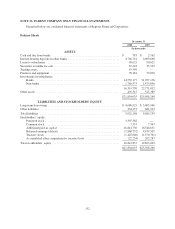

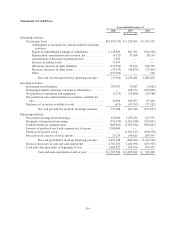

The election of the fair value option under FAS 159 impacts the timing and recognition of servicing value,

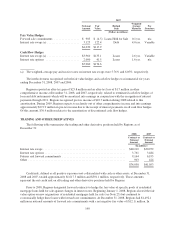

as well as origination fees and costs. The servicing value of a loan was precluded from being recognized until the

sale of the loan prior to the election of the fair value option. After adoption of the fair value option, this value is

recognized in earnings at the time of origination. Origination fees and costs for mortgage loans held for sale,

which had been previously deferred under Statement of Financial Accounting Standards No. 91, “Accounting for

Nonrefundable Fees and Costs Associated with Originating or Acquiring Loans and Initial Direct Costs of

Leases”, are now recognized in earnings at the time of origination. Prior to the election of the fair value option,

net loan origination costs for mortgage loans held for sale were capitalized as part of the carrying amount of the

loans and recognized as a reduction of mortgage income upon the sale of such loans. Approximately $10 million

of loan servicing value was recognized in non-interest income during 2008 related to the adoption of FAS 159.

The net impact of ceasing deferrals of origination fees and costs during 2008 related to the adoption of FAS 159

was not material.

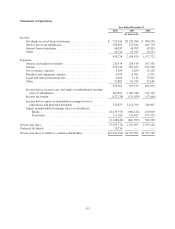

FAIR VALUE OF FINANCIAL INSTRUMENTS

The following methods and assumptions were used by the Company in estimating fair values of financial

instruments that are not disclosed under FAS 157.

Cash and cash equivalents: The carrying amounts reported in the consolidated balance sheets and cash

flows approximate the estimated fair values.

Securities held to maturity: Estimated fair values are based on quoted market prices, where available. If

quoted market prices are not available, estimated fair values are based on quoted market prices of comparable

instruments and/or discounted cash flow analyses.

Other interest-earning assets: The carrying amounts reported in the consolidated balance sheets

approximate the estimated fair values.

Loans: The fair values of loans, excluding leases, are estimated based on groupings of similar loans by type,

interest rate, and borrower creditworthiness. Discounted future cash flow analyses are performed for the

groupings incorporating assumptions of current and projected prepayment speeds. Discount rates are determined

using the Company’s current origination rates on similar loans, adjusted for changes in current liquidity and

credit spreads (if necessary).

Deposits: The fair value of non-interest-bearing demand accounts, interest-bearing transaction accounts,

savings accounts, money market accounts and certain other time deposit accounts is the amount payable on

demand at the reporting date (i.e., the carrying amount). Fair values for certificates of deposit are estimated by

using discounted cash flow analyses, based on the interest rates currently offered for deposits of similar

maturities.

Short-term and long-term borrowings: The carrying amounts of short-term borrowings reported in the

consolidated balance sheets approximate the estimated fair values. The fair values of long-term borrowings are

estimated using quoted market prices. If quoted market prices are not available, fair values are estimated using

discounted future cash flow analyses based on current interest rates, liquidity and credit spreads.

Loan commitments, standby and commercial letters of credit: The estimated fair values for these off-balance

sheet instruments are based on probabilities of funding to project expected future cash flows, which are

discounted using the loan methodology described above.

146