Regions Bank 2008 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2008 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

PREPAYMENT RISK

Regions, like most financial institutions, is subject to changing prepayment speeds on mortgage-related

assets under different interest rate environments. Prepayment risk is a significant risk to earnings and specifically

to net interest income. For example, mortgage loans and other financial assets may be prepaid by a debtor, so that

the debtor may refinance its obligations at lower rates. As loans and other financial assets prepay in a falling rate

environment, Regions must reinvest these funds in lower-yielding assets. Prepayments of assets carrying higher

rates reduce Regions’ interest income and overall asset yields. Conversely, in a rising rate environment, these

assets will prepay at a slower rate, resulting in opportunity cost by not having the cash flow to reinvest at higher

rates. Regions’ greatest exposure to prepayment risks primarily rests in its mortgage-backed securities portfolio,

the mortgage fixed-rate loan portfolio and the mortgage servicing asset, all of which tend to be sensitive to

interest rate movements. Prepayments on mortgage-backed securities slowed during the latter half of 2008 due to

various factors associated with the housing crisis. Tighter lending standards, decreased home prices, and

uncertainty surrounding the economic environment created slower prepayment speeds on mortgage-backed

securities. Regions also has prepayment risk that would be reflected in non-interest income in the form of

servicing income on loans sold. In 2008, prepayment rates were lower compared to recent years; however the

Company anticipates the rate of prepayments to increase in 2009, driven primarily by the high refinancing

activity the Company has experienced since the start of the year. Regions actively monitors prepayment exposure

as part of its overall net interest income forecasting and interest rate risk management.

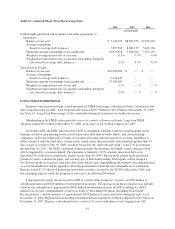

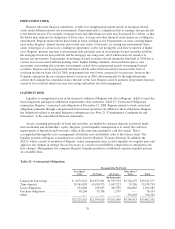

LIQUIDITY RISK

Liquidity is an important factor in the financial condition of Regions and affects Regions’ ability to meet the

borrowing needs and deposit withdrawal requirements of its customers. Table 21 “Contractual Obligations”

summarizes Regions’ contractual cash obligations at December 31, 2008. Regions intends to fund contractual

obligations primarily through cash generated from normal operations. In addition to these obligations, Regions

has obligations related to potential litigation contingencies (see Note 25 “Commitments, Contingencies and

Guarantees” to the consolidated financial statements).

Assets, consisting principally of loans and securities, are funded by customer deposits, purchased funds,

borrowed funds and stockholders’ equity. Regions’ goal in liquidity management is to satisfy the cash flow

requirements of depositors and borrowers, while at the same time meeting its cash flow needs. This is

accomplished through the active management of both the asset and liability sides of the balance sheet. The

liquidity position of Regions is monitored on a daily basis by Regions’ Treasury Division. In addition, the

ALCO, which consists of members of Regions’ senior management team, reviews liquidity on a regular basis and

approves any changes in strategy that are necessary as a result of asset/liability composition or anticipated cash

flow changes. Management also compares Regions’ liquidity position to established corporate liquidity policies

on a monthly basis.

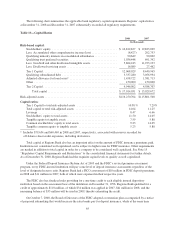

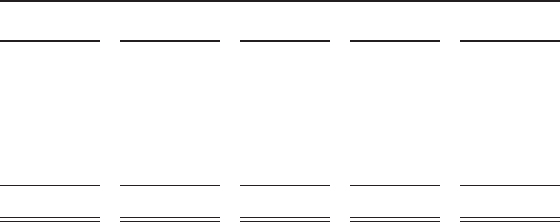

Table 21—Contractual Obligations

Payments Due By Period

Less than 1

Year 1-3 Years 4-5 Years

More than 5

Years Total

(In thousands)

Long-term borrowings ............... $ 2,671,023 $10,875,851 $1,955,924 $3,728,479 $19,231,277

Time deposits ..................... 20,361,650 10,430,575 1,647,223 39,286 32,478,734

Lease obligations ................... 154,646 256,635 205,559 644,845 1,261,685

Purchase obligations ................ 38,206 35,558 2,339 — 76,103

Other ............................ — — — 354,343 354,343

$23,225,525 $21,598,619 $3,811,045 $4,766,953 $53,402,142

70