Regions Bank 2008 Annual Report Download - page 155

Download and view the complete annual report

Please find page 155 of the 2008 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

Mortgage servicing rights are initially recorded at estimated fair value and are then periodically measured

for impairment by projecting and discounting future cash flows associated with servicing at market rates. The

projection of cash flows is a Level 3 measurement, incorporating assumptions of changes in cash flows due to

estimated prepayments, estimated costs to service and estimates of other servicing income. Market assumptions,

where available, are obtained from brokers and adjusted for Company-specific observations. These assumptions

primarily include discount rates and expected prepayments.

In addition to the assets currently measured at fair value mentioned above, Regions often uses fair value

measurements in determining the period-end balance of certain financial instruments such as non-marketable

investments. Typically, these assets use fair value measurements to determine the recorded lower of cost or fair

value of the asset or to determine the losses incurred during the period. As of December 31, 2008, none of these

assets were recognized at fair value on the consolidated balance sheet.

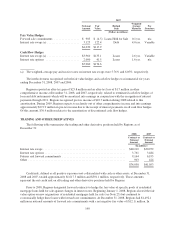

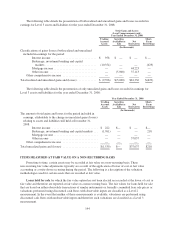

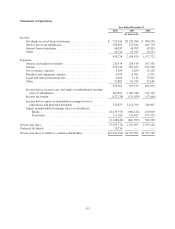

The following table presents the carrying value of those assets measured at fair value on a non-recurring

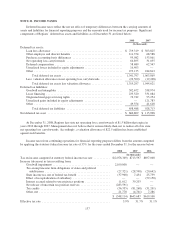

basis as of December 31, 2008, and gains and losses recognized during the year. The table does not reflect the

change in fair value attributable to any related economic hedges the Company used to mitigate the interest rate

risk associated with these assets.

Carrying Value as of December 31, 2008

Fair value

adjustments for

the year ended

December 31, 2008Level 1 Level 2 Level 3 Total

(Dollars in thousands)

Loans Held for Sale ........................ $— $133,912 $221,300 $355,212 $(358,937)

Mortgage Servicing Rights ................... — — 160,890 160,890 (85,000)

Regions also uses fair value measurements on a non-recurring basis for certain non-financial instruments

such as other real estate and foreclosed assets. However, the effective date for the FAS 157 requirements for

these instruments was deferred until January 1, 2009. See Note 1 for further discussion.

FAIR VALUE OPTION

Regions also adopted FAS 159 as of January 1, 2008. FAS 159 allows an entity the irrevocable option to

elect fair value for the initial and subsequent measurement for certain financial assets and liabilities on a

contract-by-contract basis. FAS 159 requires the difference between the carrying value before election of the fair

value option and the fair value of these financial instruments be recorded as an adjustment to beginning retained

earnings in the period of adoption. There was no material effect of adoption on the consolidated financial

statements.

Regions elected the fair value option for residential mortgage loans held for sale originated after January 1,

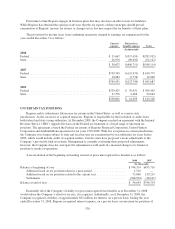

2008. This election allows for a more effective offset of the changes in fair values of the loans and the derivative

instruments used to economically hedge them without the burden of complying with the requirements for hedge

accounting under FAS 133. Regions has not elected the fair value option for other loans held for sale primarily

because they are not economically hedged using derivative instruments. Fair values of loans held for sale are

based on traded market prices of similar assets where available and/or discounted cash flows at market interest

rates, adjusted for securitization activities that include servicing values and market conditions. At December 31,

2008, loans held for sale for which the fair value option was elected had an aggregate fair value of $506.3 million

and an aggregate outstanding principal balance of $492.3 million and were recorded in loans held for sale in the

consolidated balance sheet. Interest income on mortgage loans held for sale is recognized based on contractual

rates and reflected in interest income on loans held for sale in the consolidated statements of operations. Net

gains (losses) resulting from changes in fair value of these loans of $16.2 million was recorded in mortgage

income in the consolidated statement of operations for the year ended December 31, 2008. These changes in fair

value are mostly offset by economic hedging activities. An immaterial portion of this amount was attributable to

changes in instrument-specific credit risk.

145