Regions Bank 2008 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2008 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

about the direction and volatility of interest rates, the slope of the yield curve, and the changing composition of

the balance sheet that result from both strategic plans and from customer behavior. Among the assumptions are

expectations of balance sheet growth and composition, the pricing and maturity characteristics of existing

business and the characteristics of future business. Interest rate-related risks are expressly considered, such as

pricing spreads, the lag time in pricing administered rate accounts, prepayments and other option risks. Regions

considers these factors, as well as the degree of certainty or uncertainty surrounding their future behavior.

Financial derivative instruments are used in hedging the values of selected assets and liabilities against changes

in interest rates. The effect of these hedges is included in the simulations of net interest income.

The primary objective of Asset/Liability Management at Regions is to coordinate balance sheet composition

with interest rate risk management to sustain reasonable and stable net interest income throughout various

interest rate cycles. A standard set of alternate interest rate scenarios is compared to the results of the base case

scenario to determine the extent of potential fluctuations and to establish exposure limits. The standard set of

interest rate scenarios includes the traditional instantaneous parallel rate shifts of plus and minus 100 and 200

basis points. However, for the purposes of analyzing the impact of further downward movement in the rate

structure, in the down scenarios, whenever prevailing rates are less than 100 basis points (e.g. the Federal Funds

Target rate is currently at 0 to 25 basis points) rates have been assumed to be zero. Accordingly, the Company

has determined that the down 200 scenario that is typically calculated is not a meaningful measure. Refer to

Table 20 “Interest Rate Sensitivity” for more information.

In addition to instantaneous scenarios, Regions employs simulations of gradual interest rate movements that

may more realistically mimic potential interest rate movements. The gradual scenarios include curve steepening,

flattening and parallel movements of various magnitudes phased in over a six-month period.

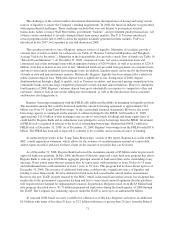

Exposure to Interest Rate Movements—As of December 31, 2008, Regions was asset sensitive in

positioning to both gradual and instantaneous rate shifts. Table 20 “Interest Rate Sensitivity” demonstrates the

estimated potential effects that gradual (over six months beginning at December 31, 2008 and 2007, respectively)

and instantaneous parallel interest rate shifts would have on Regions’ net interest income.

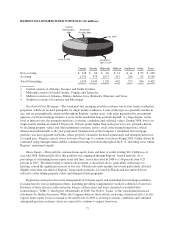

Table 20—Interest Rate Sensitivity

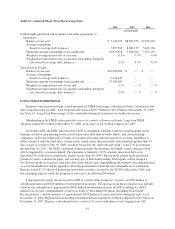

Estimated % Change

in Net Interest Income

December 31

Gradual Change in Interest Rates 2008 2007

+ 200 basis points ...................................... 4.9% 1.7%

+ 100 basis points ...................................... 2.8 1.1

- 100 basis points ...................................... (1.4) (1.1)

- 200 basis points ...................................... NA (3.2)

Estimated % Change

in Net Interest Income

December 31

Instantaneous Change in Interest Rates 2008 2007

+ 200 basis points ...................................... 5.0% 1.1%

+ 100 basis points ...................................... 2.8 1.0

- 100 basis points ...................................... (1.0) (1.5)

- 200 basis points ...................................... NA (4.5)

Derivatives—Regions uses financial derivative instruments for management of interest rate sensitivity. The

Asset and Liability Committee (“ALCO”), which consists of members of Regions’ senior management team, in

its oversight role for the management of interest rate sensitivity, approves the use of derivatives in balance sheet

hedging strategies. The most common derivatives Regions employs are forward rate contracts, Eurodollar futures

68