Regions Bank 2008 Annual Report Download - page 153

Download and view the complete annual report

Please find page 153 of the 2008 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

and option pricing models based on market rates and volatilities, or Level 2 measurements. Interest rate lock

commitments on loans intended for sale, treasury locks and credit derivatives are valued using option pricing

models that incorporate significant unobservable inputs, and therefore are Level 3 measurements.

Interest rate swaps are predominantly traded in over-the-counter markets and, as such, values are determined

using widely accepted discounted cash flow models, or Level 2 measurements. These discounted cash flow

models use projections of future cash payments/receipts that are discounted at mid-market rates. These valuations

are adjusted for the unsecured credit risk at the reporting date, which considers collateral posted and the impact

of master netting agreements.

Short-term borrowings recognized at fair value represent short-sale liabilities to counterparties. Short-sale

liabilities are valued based on the fair value of the underlying securities, which are determined in the same

manner as trading account assets and securities available for sale.

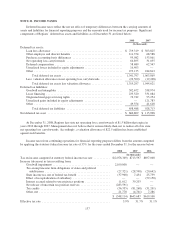

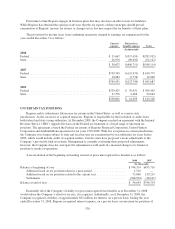

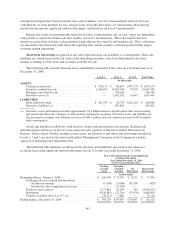

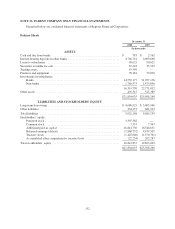

The following table presents financial assets and liabilities measured at fair value on a recurring basis as of

December 31, 2008:

Level 1 Level 2 Level 3 Fair Value

(In thousands)

ASSETS:

Trading account assets ............................ $ 338,133 $ 318,867 $393,270 $ 1,050,270

Securities available for sale ......................... 2,658,994 16,095,449 95,039 18,849,482

Mortgage loans held for sale ........................ — 506,260 — 506,260

Derivative assets (a) .............................. — 1,842,652 54,847 1,897,499

LIABILITIES:

Short-term borrowings ............................ $ 421,799 $ 88,743 $118,124 $ 628,666

Derivative liabilities (a) ........................... — 895,841 — 895,841

(a) Derivative assets and liabilities include approximately $1.6 billion related to legally enforceable master netting

agreements that allow the Company to settle positive and negative positions. Derivative assets and liabilities are

also presented excluding cash collateral received of $108.1 million and cash collateral posted of $450.9 million

with counterparties.

Assets and liabilities in all levels could result in volatile and material price fluctuations. Realized and

unrealized gains and losses on Level 3 assets represent only a portion of the risk to market fluctuations in

Regions’ balance sheets. Further, trading account assets, net derivatives and short-term borrowings included in

Levels 1, 2 and 3 are used by the Asset and Liability Management Committee of the Company in a holistic

approach to managing price fluctuation risks.

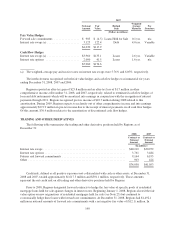

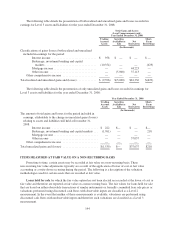

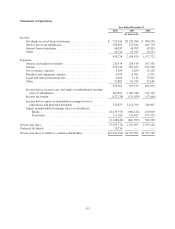

The following table illustrates a rollforward for all assets and (liabilities) measured at fair value on a

recurring basis using significant unobservable inputs (Level 3) for the year ended December 31, 2008:

Fair Value Measurements Using Significant

Unobservable Inputs

Year Ended December 31, 2008

(Level 3 measurements only)

Trading

Account

Assets

Securities

Available

for Sale

Net

Derivatives

Short-Term

Borrowings

(In thousands)

Beginning balance, January 1, 2008 ........................ $ 166,003 $ 73,003 $ 8,122 $ 57,456

Total gains (losses) realized and unrealized:

Included in earnings ............................ (9,396) (5,000) 81,336 (429)

Included in other comprehensive income ............ — (3,428) — —

Purchases and issuances ............................. 3,277,881 49,100 459 (8,450,525)

Settlements ....................................... (3,020,867) (23,716) (35,070) 8,488,904

Transfers in and/or out of Level 3, net .................. (20,351) 5,080 — 22,718

Ending balance, December 31, 2008 ....................... $ 393,270 $ 95,039 $ 54,847 $ 118,124

143