Regions Bank 2008 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2008 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

position between rate-sensitive assets and liabilities in order to minimize the impact of interest rate fluctuations

on net interest income. This goal, however, can be difficult to completely achieve in times of rapidly changing

rate structure, such as that experienced in 2008.

EFFECTS OF DEFLATION

A period of deflation would affect all industries, including financial institutions. Potentially, deflation could

lead to lower profits, higher unemployment and deterioration in overall economic conditions. In addition,

deflation could depress economic activity and impair bank earnings through increasing the value of debt while

decreasing the value of collateral for loans. If the economy experienced a severe period of deflation, then it could

depress loan demand, impair the ability of borrowers to repay loans and sharply reduce bank earnings.

Management believes the most significant potential impact of deflation on financial results is a direct result

of Regions’ ability to maintain a high amount of capital to cushion against future losses. In addition, the

Company’s risk management can utilize certain tools to help the bank maintain its balance sheet strength even if

a deflationary scenario were to develop.

RISK MANAGEMENT

Risk identification and risk management are key elements in the overall management of Regions.

Management believes the primary risk exposures are interest rate and associated prepayment risk, liquidity risk,

market and other brokerage-related risk associated with Morgan Keegan, counterparty risk, and credit risk.

Interest rate risk is the risk to net interest income due to the impact of movements in interest rates. Prepayment

risk is the risk that borrowers may repay their loans or securities earlier than at their stated maturities. Liquidity

risk relates to Regions’ ability to fund present and future obligations. The Company, through Morgan Keegan, is

also subject to various market-related risks associated with its brokerage and market-related activities.

Counterparty risk represents the risk that a counterparty will not comply with its contractual obligations. Credit

risk represents the possibility that borrowers may not be able to repay loans.

External factors beyond management’s control may result in losses despite risk management efforts.

Management follows a formal policy to evaluate and document the key risks facing each line of business, how

those risks can be controlled or mitigated, and how management monitors the controls to ensure that they are

effective. Regions’ Internal Audit Division performs ongoing, independent reviews of the risk management

process and assures the adequacy of documentation. The results of these reviews are reported regularly to the

Audit Committee of the Board of Directors. The Company also has a Risk Committee that assists the Board of

Directors in overseeing the Company’s policies, procedures and practices relating to market, regulatory and

operational risk.

Some of the more significant processes used to manage and control these and other risks are described in the

remainder of this report.

INTEREST RATE RISK

Regions’ primary market risk is interest rate risk, including uncertainty with respect to absolute interest rate

levels as well as uncertainty with respect to relative interest rate levels, which is impacted by both the shape and

the slope of the various yield curves that affect the financial products and services that the Company offers. To

quantify this risk, Regions measures the change in its net interest income in various interest rate scenarios

compared to a base case scenario. Net interest income sensitivity is a useful short-term indicator of Regions’

interest rate risk.

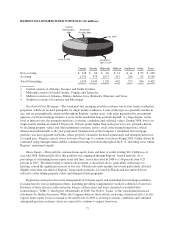

Sensitivity Measurement—Financial simulation models are Regions’ primary tools used to measure interest

rate exposure. Using a wide range of sophisticated simulation techniques provides management with extensive

information on the potential impact to net interest income caused by changes in interest rates. Models are

structured to simulate cash flows and accrual characteristics of Regions’ balance sheet. Assumptions are made

67