Regions Bank 2008 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2008 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

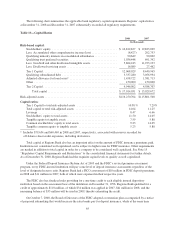

making adjustments to the system that determines what rate a bank pays the FDIC. Under this and additional

proposals, the assessment rate schedule will be raised beginning on January 1, 2009. Also during 2009, Regions’

one-time assessment credit will expire. Based on certain assumptions regarding various assessment criteria,

including future deposit levels, Regions estimates FDIC premiums will increase within a range of $90 million to

$110 million (pre-tax) during 2009. Assessment rates, however, are subject to change by the FDIC throughout

the year.

OFF-BALANCE SHEET ARRANGEMENTS

Regions’ primary off-balance sheet arrangements are financial instruments issued in connection with

lending activities. These arrangements include commitments to extend credit, standby letters of credit and

commercial letters of credit. A meaningful component of the off-balance sheet arrangements are facilities

supporting Variable Rate Demand Notes (“VRDNs”), including certain standby letters of credit and standby bond

purchase agreements (also referred to as “liquidity facilities”). Fundings under these letters of credit are largely

related to redemption requests in money market mutual funds that invested in VRDNs as a result of the increased

volatility in the financial markets. Late in 2008, disruption in market liquidity supporting VRDNs resulted in

significant frequency of failed remarketing of VRDNs. As of December 31, 2008, Regions had funded $331.7

million in letters of credit backing VRDN’s. An additional $9 million had been tendered but not yet funded. The

remaining unfunded VRDN letters of credit portfolio is approximately $4.9 billion (net of participations). See

Note 25 “Commitments, Contingencies and Guarantees” to the consolidated financial statements for further

discussion, including details of the contractual amounts outstanding at December 31, 2008.

Regions has certain variable interests in unconsolidated variable interest entities (i.e., Regions is not the

primary beneficiary). Regions owns the common stock of subsidiary business trusts, which have issued

mandatorily redeemable preferred capital securities (“trust preferred securities”) in the aggregate of $1.0 billion

at the time of issuance. These trusts meet the definition of a variable interest entity of which Regions is not the

primary beneficiary; the trusts’ only assets are junior subordinated debentures issued by Regions, which were

acquired by the trusts using the proceeds from the issuance of the trust preferred securities and common stock.

The junior subordinated debentures are included in long-term borrowings and Regions’ equity interests in the

business trusts are included in other assets. For regulatory reporting and capital adequacy purposes, the Federal

Reserve Board has indicated that such trust preferred securities will continue to constitute Tier 1 Capital until

further notice.

Also, Regions periodically invests in various limited partnerships that sponsor affordable housing projects,

which are funded through a combination of debt and equity with equity typically comprising 30% to 50% of the

total partnership capital. Regions’ maximum exposure to loss as of December 31, 2008 was $710.0 million,

which included $298.1 million in unfunded commitments to the partnerships. Additionally, Regions has short-

term construction loans or letters of credit with the partnerships totaling $187.7 million as of December 31, 2008.

The portion of the letters of credit which was funded was $114.8 million at December 31, 2008. The funded

portion is included with loans on the consolidated balance sheets. See Note 2 “Variable Interest Entities” to the

consolidated financial statements for further discussion.

EFFECTS OF INFLATION

The majority of assets and liabilities of a financial institution are monetary in nature; therefore, a financial

institution differs greatly from most commercial and industrial companies, which have significant investments in

fixed assets or inventories that are greatly impacted by inflation. However, inflation does have an important

impact on the growth of total assets in the banking industry and the resulting need to increase equity capital at

higher than normal rates in order to maintain an appropriate equity-to-assets ratio. Inflation also affects other

expenses that tend to rise during periods of general inflation.

Management believes the most significant potential impact of inflation on financial results is a direct result

of Regions’ ability to react to changes in interest rates. Management attempts to maintain an essentially balanced

66