Regions Bank 2008 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2008 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

The ability of Regions to pay dividends to its shareholders, however, is not totally dependent on the receipt

of dividends from Regions Bank, as Regions has other cash available to make such payment. As of December 31,

2008, Regions had $4.8 billion of cash and cash equivalents, which is available for corporate purposes, including

debt service and to pay dividends to its shareholders. This compares to an anticipated common dividend

requirement, assuming current dividend payment levels, of approximately $277 million and preferred cash

dividends of approximately $175 million for the full-year 2009. Expected debt maturities in 2009 total

approximately $425 million.

Although Regions currently has capacity to make common dividend payments in 2009, the payment of

dividends by Regions and the dividend rate are subject to management review and approval by Regions’ Board

of Directors on a quarterly basis. Preferred dividends are to be paid in accordance with the terms of the CPP. See

Item 1 “Business” and Item 1A. “Risk Factors” for additional information.

BANK REGULATORY CAPITAL REQUIREMENTS

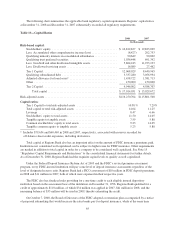

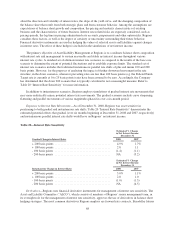

Regions and Regions Bank are required to comply with capital adequacy standards established by banking

regulatory agencies. Currently, there are two basic measures of capital adequacy: a risk-based measure and a

leverage measure.

The risk-based capital standards are designed to make regulatory capital requirements more sensitive to

differences in credit risk profiles among banks and bank holding companies, to account for off-balance sheet

exposure and interest rate risk, and to minimize disincentives for holding liquid assets. Assets and off-balance

sheet items are assigned to broad risk categories, each with specified risk-weighting factors. The resulting capital

ratios represent capital as a percentage of total risk-weighted assets and off-balance sheet items. Banking

organizations that are considered to have excessive interest rate risk exposure are required to maintain higher

levels of capital.

The minimum standard for the ratio of total capital to risk-weighted assets is 8%. At least 50% of that

capital level must consist of common equity, undivided profits and non-cumulative perpetual preferred stock, less

goodwill and certain other intangibles (“Tier 1 Capital”). The remainder (“Tier 2 Capital”) may consist of a

limited amount of other preferred stock, mandatory convertible securities, subordinated debt, and a limited

amount of the allowance for loan losses. The sum of Tier 1 Capital and Tier 2 Capital is “total risk-based capital”

or total capital.

The banking regulatory agencies also have adopted regulations that supplement the risk-based guidelines to

include a minimum ratio of 3% of Tier 1 Capital to average assets less goodwill (the “Leverage ratio”).

Depending upon the risk profile of the institution and other factors, the regulatory agencies may require a

Leverage ratio of 1% to 2% above the minimum 3% level.

In October, 2008, President Bush signed into law the Emergency Economic Stabilization Act of 2008 in

response to the financial crises affecting the banking system. The U.S. Treasury and banking regulators are

implementing a number of programs under this legislation to address capital and liquidity issues in the banking

system. Under the U. S. Treasury’s CPP, Regions received $3.5 billion through its issuance of preferred stock

and a warrant for common stock to the U.S. Treasury. The preferred stock issuance and the related warrant both

qualify for Tier 1 capital and added approximately 300 basis points to that measure. The fair value allocation of

the $3.5 billion between the preferred shares and the warrant resulted in $3.304 billion allocated to the preferred

shares and $196 million allocated to the warrant. Both the preferred securities and the warrant will be accounted

for as components of Regions’ regulatory Tier 1 capital. See discussion of “Stockholders’ Equity” above for

additional details.

64