Regions Bank 2008 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2008 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

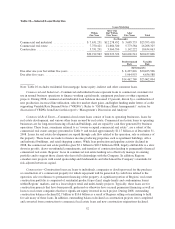

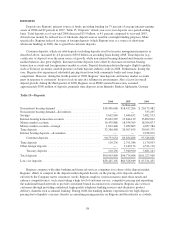

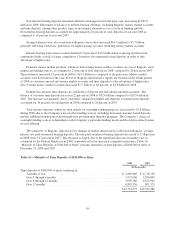

DEPOSITS

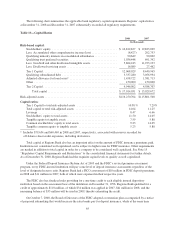

Deposits are Regions’ primary source of funds, providing funding for 75 percent of average interest-earning

assets in 2008 and 82 percent in 2007. Table 15 “Deposits” details year-over-year deposits on a period-ending

basis. Total deposits as of year-end 2008 decreased $3.9 billion, or 4.1 percent, compared to year-end 2007,

driven lower mainly by reduced use of wholesale deposit sources used for overnight funding purposes. More

specifically, Regions reduced its usage of foreign deposits (which Regions uses as a source of short-term

wholesale funding) in 2008, due to growth in customer deposits.

Customer deposits, which are total deposits excluding deposits used for treasury management purposes as

described above, increased by 4.6 percent to $90.8 billion on an ending basis during 2008. Time deposits (e.g.,

certificates of deposit) were the main source of growth, while non-interest bearing demand and domestic money

market balances also grew slightly. Increases in time deposits were offset by decreases in interest-bearing

transaction accounts and foreign money market accounts. Deposit disintermediation through a flight to quality,

such as Treasury securities, exerted pressure on bank deposits industry-wide in 2008. Furthermore, during the

year, Regions also experienced substantial pricing strain from both community banks and some larger

competitors. However, during the fourth quarter of 2008, Regions’ time deposits and money market accounts

grew in response to customers’ desire to lock-in rates in a falling rate environment. Also a factor in overall

deposit growth, during the third quarter of 2008, Regions, in an FDIC-assisted transaction, assumed

approximately $900 million of deposits, primarily time deposits, from Integrity Bank in Alpharetta, Georgia.

Table 15—Deposits

2008 2007 2006

(In thousands)

Non-interest bearing demand .............................. $18,456,668 $18,417,266 $ 20,175,482

Non-interest bearing demand—divestitures ................... — — 533,295

Savings ............................................... 3,662,949 3,646,632 3,882,533

Interest-bearing transaction accounts ........................ 15,022,207 15,846,139 15,899,812

Money market accounts .................................. 19,470,886 18,934,309 18,764,873

Money market accounts—foreign ........................... 1,812,446 3,482,603 4,037,384

Time deposits .......................................... 32,368,498 26,507,459 30,015,375

Interest bearing deposits—divestitures ....................... — — 2,238,072

Customer deposits ................................... 90,793,654 86,834,408 95,546,826

Time deposits .......................................... 110,236 2,791,386 1,170,033

Other foreign deposits .................................... — 5,149,174 4,511,110

Treasury deposits .................................... 110,236 7,940,560 5,681,143

Total deposits .......................................... $90,903,890 $94,774,968 $101,227,969

Low cost deposits ....................................... $58,425,156 $60,326,949 $ 65,531,451

Regions competes with other banking and financial services companies for a share of the deposit market.

Regions’ ability to compete in the deposit market depends heavily on the pricing of its deposits and how

effectively the Company meets customers’ needs. Regions employs various means to meet those needs and

enhance competitiveness, such as providing a high level of customer service, competitive pricing and expanding

the traditional branch network to provide convenient branch locations for its customers. Regions also services

customers through providing centralized, high-quality telephone banking services and alternative product

delivery channels such as internet banking. During 2008, the banking industry experienced very high deposit

pricing due to liquidity concerns, thereby accentuating pricing pressure on Regions and the industry as a whole.

58