Regions Bank 2008 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2008 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

The challenges of the current market environment demonstrate the importance of having and using various

sources of liquidity to satisfy the Company’s funding requirements. In 2008, the financial industry was presented

with unprecedented challenges. Those challenges included but were not limited to government-assisted

transactions, failure of major Wall Street firms, government “bailouts”, and government-guided transactions. All

of these events contributed to severely disrupted short-term money markets. The U.S. Treasury introduced

several programs in the fall of 2008 to aid in the liquidity normally generated in these markets. TAF was

introduced in late 2007, but expanded in size and duration in 2008.

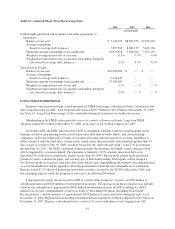

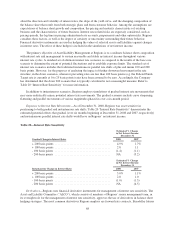

The securities portfolio is one of Regions’ primary sources of liquidity. Maturities of securities provide a

constant flow of funds available for cash needs (see Table 12 “Relative Contractual Maturities and Weighted-

Average Yields for Securities”). Maturities in the loan portfolio also provide a steady flow of funds (see Table 10

“Selected Loan Maturities”). At December 31, 2008, commercial loans, real estate construction loans and

commercial real estate mortgage loans with an aggregate balance of $20.9 billion, as well as securities of $229.4

million, were due to mature in one year or less. Additional funds are provided from payments on consumer loans

and one-to-four family residential first mortgage loans. In addition, liquidity needs can be met by the borrowing

of funds in state and national money markets. Historically, Regions’ liquidity has been enhanced by a relatively

stable customer deposit base. While this deposit base is significant in size, during most of 2008, deposit

disintermediation through a flight to quality, such as Treasury securities, and increased pricing competition from

community banks and some large competitors pressured overall customer deposit balances. However, during the

fourth quarter of 2008, Regions’ customer deposit base grew substantially in response to competitive offers and

customers’ desire to lock-in rates in the falling rate environment, as well as the introduction of new consumer

and business checking products.

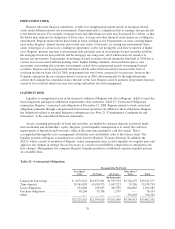

Regions’ financing arrangement with the FHLB adds additional flexibility in managing its liquidity position.

The maximum amount that could be borrowed under the current borrowing agreement is approximately $1.1

billion (see Note 14 “Long-Term Borrowings” to the consolidated financial statements). However, the actual

borrowing capacity is contingent on the amount of collateral pledged to the FHLB. At December 31, 2008,

approximately $11.6 billion of first mortgage loans on one-to-four family dwellings and home equity lines of

credit held by Regions Bank and its subsidiaries were pledged to secure borrowings from the FHLB. Investment

in FHLB stock is required in relation to the level of outstanding borrowings. Regions held $458.2 million in

FHLB stock at December 31, 2008. As of December 31, 2008, Regions’ borrowings from the FHLB totaled $9.6

billion. The FHLB has been and is expected to continue to be a reliable and economical source of funding.

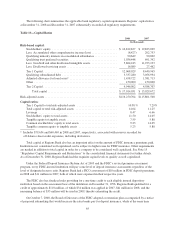

As mentioned previously in the “Long-Term Borrowings” section of this report, Regions has on file with the

SEC, a shelf registration statement, which allows for the issuance of an indeterminate amount of various debt

and/or equity securities and does not have a limit on the amount of securities that can be issued.

As of December 31, 2008, Regions Bank had issued the maximum amount of $5 billion under its previously

approved bank note program. In July 2008, the Board of Directors approved a new bank note program that allows

Regions Bank to issue up to $20 billion aggregate principal amount of bank notes that can be outstanding at any

one time. Notes issued under the new program may be senior notes with maturities of from 30 days to 15 years

and subordinated notes with maturities of from 5 years to 30 years. This program had not been drawn upon as of

December 31, 2008. The issuance of additional bank notes could provide a significant source of liquidity and

funding to meet future needs. Investor demand for bank notes had ceased in the current market environment.

However, the new TLGP recently enacted by the FDIC, which is discussed later in this section, has reopened this

market due to the government’s guarantee backing and has to some extent renewed optimism that this platform

will reopen investor demand for unguaranteed issuances. In particular, Regions issued, from the $5 billion bank

note program described above, $3.75 billion in guaranteed bank notes during the fourth quarter of 2008 through

the TLGP. The Company has remaining capacity under the TLGP to issue up to an additional $4 billion.

At year-end 2008, based on assets available for collateral as of this date, Regions can borrow an additional

$9.0 billion with terms of less than 29 days, or $7.2 billion with terms of greater than 29 days, from the Federal

71