Regions Bank 2008 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2008 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

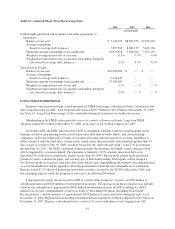

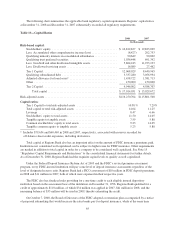

The following chart summarizes the applicable bank regulatory capital requirements. Regions’ capital ratios

at December 31, 2008 and December 31, 2007 substantially exceeded all regulatory requirements.

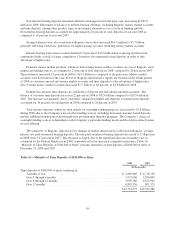

Table 19—Capital Ratios

2008 2007

(In thousands)

Risk-based capital:

Stockholders’ equity ............................................ $ 16,812,837 $ 19,823,029

Less: Accumulated other comprehensive income (loss) ................. (8,427) 202,753

Qualifying minority interests in consolidated subsidiaries ............... 90,649 90,002

Qualifying trust preferred securities ................................ 1,036,448 691,342

Less: Goodwill and other disallowed intangible assets .................. 5,864,243 11,933,193

Less: Disallowed servicing assets .................................. 16,089 27,462

Tier 1 Capital .................................................. 12,068,029 8,440,965

Qualifying subordinated debt ..................................... 3,337,280 3,056,994

Adjusted allowance for loan losses* ................................ 1,458,722 1,381,713

Other ........................................................ 150,000 150,000

Tier 2 Capital .................................................. 4,946,002 4,588,707

Total capital ............................................... $ 17,014,031 $ 13,029,672

Risk-adjusted assets ................................................. $116,250,704 $115,801,508

Capital ratios:

Tier 1 Capital to total risk-adjusted assets ........................... 10.38 % 7.29%

Total capital to total risk-adjusted assets ............................ 14.64 11.25

Leverage ..................................................... 8.47 6.66

Stockholders’ equity to total assets ................................. 11.50 14.05

Tangible equity to tangible assets .................................. 7.59 5.88

Common stockholders’ equity to total assets ......................... 9.23 14.05

Tangible common equity to tangible assets .......................... 5.23 5.88

* Includes $79,654 and $60,469 in 2008 and 2007, respectively, associated with reserves recorded for

off-balance sheet credit exposures, including derivatives.

Total capital at Regions Bank also has an important effect on the amount of FDIC insurance premiums paid.

Institutions not considered well capitalized can be subject to higher rates for FDIC insurance. Other requirements

are needed in addition to total capital in order for a company to be considered well capitalized. See Note 15

“Regulatory Capital Requirements and Restrictions” to the consolidated financial statements for further details.

As of December 31, 2008, Regions Bank had the requisite capital levels to qualify as well capitalized.

Under the Federal Deposit Insurance Reform Act of 2005 and the FDIC’s revised premium assessment

program, every FDIC-insured institution will pay some level of deposit insurance assessments regardless of the

level of designated reserve ratio. Regions Bank had a FICO assessment of $10 million in FDIC deposit premiums

in 2008 and $11 million in 2007, both of which were expensed in their respective years.

The FDIC also has finalized rules providing for a one-time credit to each eligible insured depository

institution based on the assessment base of the institution on December 31, 1996. Regions Bank qualified for a

credit of approximately $110 million, of which $34 million was applied in 2007, $41 million in 2008, and the

remaining balance of $35 million will be used in 2009, thereby exhausting the credit.

On October 7, 2008, the Board of Directors of the FDIC adopted a restoration plan accompanied by a notice

of proposed rulemaking that would increase the rates banks pay for deposit insurance, while at the same time

65