Regions Bank 2008 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2008 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

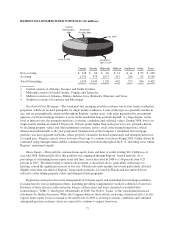

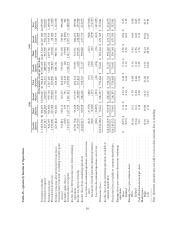

2008 2007 2006 2005 2004

(In thousands)

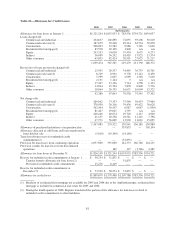

Loans, net of unearned income, outstanding

at end of period ..................... $97,418,685 $95,378,847 $94,550,602 $58,404,913 $57,526,954

Average loans, net of unearned income

outstanding for the period ............. $97,601,272 $94,372,061 $64,765,653 $58,002,167 $44,667,472

Ratios:

Allowance for loan losses at end of

period to loans, net of unearned

income ........................ 1.87% 1.39% 1.12% 1.34% 1.31%

Allowance for credit losses at end of

period to loans, net of unearned

income ........................ 1.95 1.45 1.17 1.34 1.31

Allowance for loan losses at end of

period to non-performing loans,

excluding loans held for sale ....... 1.74 1.78 3.45 2.29 1.94

Allowance for credit losses at end of

period to non-performing loans,

excluding loans held for sale ....... 1.81 1.86 3.61 2.29 1.94

Net charge-offs as percentage of:

Average loans, net of unearned

income .................... 1.59 0.29 0.22 0.23 0.29

Provision for loan losses ........ 75.2 48.7 98.2 82.5 101.9

Allowance for credit losses ...... 81.4 19.6 12.6 17.4 17.4

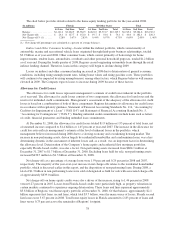

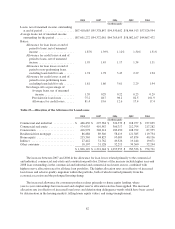

Table 23—Allocation of the Allowance for Loan Losses

2008 2007 2006 2005 2004

(In thousands)

Commercial and industrial .............. $ 466,430 $ 295,384 $ 324,539 $ 218,957 $ 237,699

Commercial real estate ................. 574,935 410,587 306,717 212,794 217,282

Construction ......................... 416,978 348,214 189,450 108,722 87,955

Residential first mortgage ............... 86,888 89,346 58,419 121,385 119,734

Home equity ......................... 235,369 94,823 95,089 67,874 40,136

Indirect ............................. 27,442 51,762 49,526 19,444 19,671

Other consumer ....................... 18,107 31,128 32,213 34,360 32,244

$ 1,826,149 $ 1,321,244 $ 1,055,953 $ 783,536 $ 754,721

The increase between 2007 and 2008 in the allowance for loan losses related primarily to the commercial

and industrial, commercial real estate and construction portfolios. Drivers of the increase include higher year-end

2008 loan outstandings in the commercial and industrial and commercial real estate sectors, combined with

higher reserve allocation rates for all three loan portfolios. The higher allocation rates are reflective of increased

loan losses and adverse quality migration within the portfolio, both of which resulted primarily from the

economic recession and the prolonged housing slump.

The increased allowance for consumer products relates primarily to home equity lending, where

year-to-year outstandings have increased and a higher reserve allocation rate has been applied. The increased

allocation rate is reflective of increased loan losses and deteriorating delinquency trends which have been caused

by deterioration in the housing markets, falling home equity values, and rising unemployment.

82