Regions Bank 2008 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2008 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

generated by the real estate property. Net charge-offs on commercial real estate loans rose substantially, from

0.15 percent in 2007 to 1.52 percent in 2008 in reaction to the dramatic slowdown in demand for real estate

properties and an associated drop in property valuations. Losses on sales or transfers to held for sale of

non-performing commercial real estate loans also contributed to the year-over-year increase in net charge-offs. In

addition, the implications of a recession further pressured borrowers and contributed to higher losses. Regions

expects that losses on these types of loans will continue to be at elevated levels during 2009.

Construction—Construction loans are primarily extensions of credit to real estate developers or investors

where repayment is dependent on the sale of real estate or income generated from the real estate collateral. A

construction loan may also be made to a commercial business for the development of land or construction of a

building where the repayment is usually derived from revenues generated from the business of the borrower (e.g.,

the sale or refinance of completed properties). These loans are generally underwritten and managed by a

specialized real estate group that also manages loan disbursements during the construction process. As of

December 31, 2008, real estate construction loans were $10.6 billion. Most construction credits were to finance

shopping centers, apartment complexes, condominiums, commercial buildings and residential property

development. Overall losses in the construction portfolio increased to 4.67 percent in 2008 as compared to 0.22

percent in 2007. The 2008 loss rate reflects the Company’s aggressive efforts to dispose of non-performing loans

within the construction portfolio.

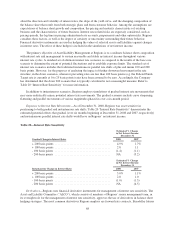

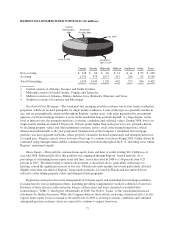

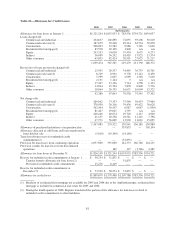

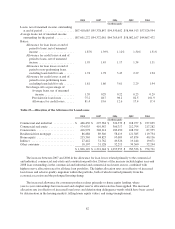

Included in the construction loan category are loans to residential homebuilders. The chart and table that

follow provide details related to this residential homebuilder portfolio, which totaled $4.4 billion at

December 31, 2008. Further details about this portfolio are also provided in the “Balance Sheet Analysis”

section, found earlier in this report. Credit quality of the construction portfolio is sensitive to risks associated

with construction loans such as cost overruns, project completion risk, general contractor credit risk,

environmental and other hazard risks, and market risks associated with the sale or rental of completed properties.

While losses within this portfolio were influenced by stresses described previously above, the most significant

driver of losses was the severe decline in demand for residential real estate. Portfolio stresses are expected to

continue throughout 2009 and, accordingly, losses on real estate construction loans are expected to continue at

elevated levels.

76