Bank of America 2006 Annual Report Download

Download and view the complete annual report

Please find the complete 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

Building

OpportunitiesTM

2006 Annual Report

Table of contents

-

Page 1

Building Opportunities 2006 Annual Report TM -

Page 2

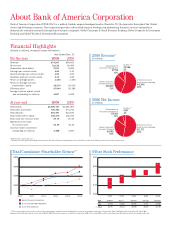

... Management $7,779 10% $2,086 3% Global Corporate & Investment Banking Global Consumer & Small Business Banking $22,691 31% $41,691 56% At year end Total assets Total loans and leases Total deposits Total shareholders' equity Book value per common share Market price per share of common stock... -

Page 3

... checking, savings, credit and debit cards, home equity lending and mortgages. We also serve mass-market small businesses with capital, credit, deposit and payment services. BUSINESSES Deposits Card Services Mortgage Home Equity Revenue* Mortgage Home Equity Net Income** Mortgage Home Equity... -

Page 4

... do we create opportunities for ourselves. Bank of America customers and clients know they can count on us to anticipate their needs, and create the opportunities that enable them to achieve their goals. - KENNETH D. LEWIS, CHAIRMAN, CHIEF EXECUTIVE OFFICER AND PRESIDENT 2 Bank of America 2006 -

Page 5

... product lines in banking, our market penetration is actually small, given our potential, in a number of areas, such as first mortgage lending, small business lending, capital markets and wealth management. These and other areas of opportunity are discussed in this annual report. Our new marketing... -

Page 6

... curve and rising credit costs, which we will most likely continue to face in 2007. The yield curve continues to be flat to inverted. The curve represents the spread between short- and long-term interest rates and is an indicator of the opportunity that banks have to generate net interest income. We... -

Page 7

... process improvement, increasing customer satisfaction and product innovation. At the same time, we have taken advantage of select opportunities presented to us to enter new markets. These acquisitions - Fleet, National Processing Inc., MBNA and U.S. Trust, scheduled to close in 2007 - add customers... -

Page 8

...in Mexico, China and Brazil. This strategy enables us to participate 21 million active online banking in the growth of the market with a customers, up local bank that brings appropriate 44% from 2005 size and scale to the table; reduces the operational risks that come with managing a foreign banking... -

Page 9

... the market of online bill payers with demand deposit accounts at financial institutions in the United States. First mortgage applications increased by 7 percent and home equity applications increased by 14 percent over 2005. Customers opened 2.4 million net new checking accounts, which contributed... -

Page 10

... for associates. As one of the largest financial service providers in the country, the opportunity we see in the future is to finance and encourage the new products, services and technologies that will help meet future global energy needs. Our goal is to help our customers and clients take the lead... -

Page 11

... and resources are managed in cooperation by leaders at the corporate and local levels, to ensure we are maximizing the impact of our work in all the neighborhoods we serve. For more information on all our programs supporting the environment and our communities, I encourage you to visit our Web site... -

Page 12

...of transactions we execute every day. That helps us understand and anticipate the needs of our clients - from individuals to global corporations. We use our knowledge to create new products, improve service and operate more effectively. The result? Growing value for shareholders. 10 Bank of America... -

Page 13

- AMY WOODS BRINKLEY, CHIEF RISK OFFICER, AND LIAM E. MCGEE, PRESIDENT, GLOBAL CONSUMER & SMALL BUSINESS BANKING Bank of America 2006 11 -

Page 14

Building Opportunities Through Integrated Delivery - BRIAN T. MOYNIHAN, PRESIDENT, GLOBAL WEALTH & INVESTMENT MANAGEMENT, AND BARBARA J. DESOER, CHIEF TECHNOLOGY & OPERATIONS OFFICER 12 Bank of America 2006 -

Page 15

...-to-coast network of banking offices in the United States, and we have made significant strategic investments overseas. We are working together to bring the entire scale, scope and resources of Bank of America to each client. Through integrated delivery of new products and services, we can provide... -

Page 16

...continually, improve our processes and focus on what really matters to our customers. We are unrivaled in our ability to integrate acquisitions. That is why, with our diverse mix of businesses, we are the most efficient bank in the world and we are growing shareholder value. 14 Bank of America 2006 -

Page 17

- R. EUGENE TAYLOR, VICE CHAIRMAN AND PRESIDENT, GLOBAL CORPORATE & INVESTMENT BANKING, AND JOE L. PRICE, CHIEF FINANCIAL OFFICER Bank of America 2006 15 -

Page 18

... HOW BANK OF AMERICA CAN GROW THROUGH BRANDING, STRATEGIC INVESTMENTS AND PRODUCT INNOVATION. FROM LEFT: BRUCE L. HAMMONDS, PRESIDENT, BANK OF AMERICA CARD SERVICES; GREGORY L. CURL, VICE CHAIRMAN OF CORPORATE DEVELOPMENT; AND J. STEELE ALPHIN, CHIEF ADMINISTRATIVE OFFICER 16 Bank of America 2006 -

Page 19

... support their groups through lines of credit and everyday checking and debit card transactions. We plan to offer affinity deposit and loan products through our more than 5,700 banking centers and the Bank of America Web site, as well as through direct marketing. We expect the new offerings to... -

Page 20

Building Opportunities in the Mortgage Market ® Helping More People Own Homes WITH GROWING PROSPECTS IN THE MORTGAGE FIELD, BANK OF AMERICA IS EXPANDING ITS OFFERINGS. DIANA SOTO MAKES CUPCAKES WITH HER CHILDREN FOR THE FIRST TIME IN THE KITCHEN OF HER NEW HOME IN PHOENIX. 18 Bank of America ... -

Page 21

... reduced application fee, a Community Commitment mortgage requires no traditional credit history, and owners can put down as little as 1 percent of the purchase price for a down payment. These loans have leveled the playing field in the real estate market, helping lower-income customers afford homes... -

Page 22

...an added bonus: The Business Coach employees who chose direct deposit got free MyAccess Checking® with Bank of America. Business 24/7 also provided them with easy access to credit through Business Credit Express , a new service that enabled Bank of America to double the number of loans and lines of... -

Page 23

... Credit ExpressTM, a card-based service that helps qualified customers get credit easily, as they need it. We also offer an online payroll program, automated invoicing and bill payment, and access to health-insurance providers specializing in plans for small employers. And in many markets, our small... -

Page 24

...Our Managing Monster Cash Flows WITH EPAYABLES, COMPANIES SAVE MONEY BY PAYING THEIR BILLS ELECTRONICALLY. Monster Worldwide Inc., the leading global online careers and recruiting company, wanted to eliminate its cumbersome paper-based accounts-payable process and consolidate its many card programs... -

Page 25

..., the shift to electronic payment mechanisms is accelerating. Our investment strategy is specifically designed to drive our capabilities and market share in electronic channels consistent with our dominant share in traditional cash management products. With a non-U.S. market share that is one-sixth... -

Page 26

... MARKETS PLATFORM, BANK OF AMERICA IS HELPING AIGGIG MEET ITS GOALS. IMPROVING QUALITY, BUILDING MARKET SHARE 2004 2005 2006 Quality Index th Rank 9 Market Share 11th 5th 9th 3rd 6th Source: Greenwich Associates; results for ï¬ xed income Opportunity â- Estimated industry revenue from sales... -

Page 27

... months. This momentum will help us become our clients' most sought after provider of financial solutions." MARK WERNER, HEAD OF GLOBAL MARKETS RICHARD SCOTT, RIGHT, CHIEF INVESTMENT OFFICER FOR AIG INSURANCE COMPANIES, IN HONG KONG WITH JOHN CHU, CHAIRMAN OF AIG GLOBAL INVESTMENT GROUP-ASIA. Bank... -

Page 28

... a Personal Touch A TEAM APPROACH PROVIDES CLIENTS WITH A FULL RANGE OF TAILORED SOLUTIONS FOR THEIR FINANCIAL NEEDS. CLIENTS TED AND CAROLYN TYLER RELAX AT THE BEACH. THEY MANAGE INVESTMENTS WITH THEIR FINANCIAL ADVISOR AND PERSONAL BANKER FROM PREMIER BANKING & INVESTMENTS. 26 Bank of America... -

Page 29

... as customers, Bank of America has the relationships to build upon. In 2006, the number of Premier Banking clients who have investment accounts with us Like many affluent Americans, Ted Tyler, an architect and business owner in California, needed more personalized financial services. "When... -

Page 30

... RENAISSANCE WALK IS THE LATEST STEP IN THE RENEWAL OF A CULTURALLY IMPORTANT NEIGHBORHOOD. SITE MANAGER BILLY K. GLAZE, LEFT, AND DEVELOPER EGBERT L.J. PERRY OF THE INTEGRAL GROUP INSPECT PROGRESS AT THE RENAISSANCE WALK PROJECT IN ATLANTA'S HISTORIC SWEET AUBURN DISTRICT. 28 Bank of America 2006 -

Page 31

... corporate philanthropy goal for 2007 is one of the largest in the world." Bank of America touches communities like Sweet Auburn in many ways. We bring together innovative products, the financial resources of one of the world's largest banks and the talents and enthusiasm of our associates. We work... -

Page 32

...'s leading online banking and bill-pay service, supported by a world-class telephone banking team. Bank of America is the leading provider of checking, savings, credit and debit cards and home equity lending, with a leading Merchant Services business and a mortgage business with growing market share... -

Page 33

... planning, customized products and relationship pricing through two key areas, Premier Banking and Banc of America Investment Services, Inc.® (BAI), a full-service and online brokerage. The Private Bank provides integrated wealth-management solutions to highnet-worth individuals, middle-market... -

Page 34

Building Opportunities on the Web Join Us Online LOG ON NOW TO ACCESS THE ENTIRE ANNUAL REPORT ON THE WEB AND TO OPT OUT OF RECEIVING PAPER COPIES IN THE FUTURE. Using the Web instead of paper to receive your Bank of America annual report is one easy way for you to help us conserve natural ... -

Page 35

Bank of America 2006 Financial Review Bank of America 2006 33 -

Page 36

...75 76 77 81 81 81 81 84 84 84 86 96 98 99 Consolidated Statement of Income ...100 Consolidated Balance Sheet ...101 Consolidated Statement of Changes in Shareholders' Equity ...102 Consolidated Statement of Cash Flows ...103 Notes to Consolidated Financial Statements ...104 34 Bank of America 2006 -

Page 37

... margins and impact funding sources; changes in foreign exchange rates; adverse movements and volatility in debt and equity capital markets; changes in market rates and prices which may adversely impact the value of financial products including securities, loans, deposits, debt and derivative... -

Page 38

... growth which increased Average Loans and Leases. Noninterest Income increased primarily due to the MBNA merger which resulted in an increase in Card Income driven by increases in excess servicing income, cash advance fees, interchange income and late fees. These increases were partially offset by... -

Page 39

... portfolio balances (primarily residential mortgages) and the impact of changes in spreads across all product categories. These increases were partially offset by a lower contribution from market-based earning assets and the higher costs associated with higher levels of wholesale funding. The net... -

Page 40

... 4 Selected Balance Sheet Data December 31 (Dollars in millions) Average Balance 2005 2006 2006 2005 Assets Federal funds sold and securities purchased under agreements to resell Trading account assets Debt securities Loans and leases, net of allowance for loan and lease losses All other assets... -

Page 41

...-making activities in interest rate, credit and equity products. For additional information, see Market Risk Management beginning on page 75. IRAs, and noninterest-bearing deposits. Core deposits exclude negotiable CDs, public funds, other domestic time deposits and foreign interestbearing deposits... -

Page 42

...per share information) 2006 2005 2004 2003 2002 Income statement Net interest income Noninterest income Total revenue Provision for credit losses Gains (losses) on sales of debt securities Noninterest expense Income before income taxes Income tax expense Net income Average common shares issued... -

Page 43

... our use of equity (i.e., capital) at the individual unit level and are integral components in the analytics for resource allocation. We believe using SVA as a performance measure places specific focus on whether incremental investments generate returns in excess of the costs of capital associated... -

Page 44

... yield Efficiency ratio Reconciliation of net income to operating earnings Net income Merger and restructuring charges Related income tax benefit Operating earnings Reconciliation of average shareholders' equity to average tangible shareholders' equity Average shareholders' equity Average goodwill... -

Page 45

... product categories. Partially offsetting these increases was the higher costs associated with higher levels of wholesale funding. On a managed basis, core average earning assets increased $199.3 billion primarily due to the impact of the MBNA merger, higher levels of consumer and commercial loans... -

Page 46

...management accounting reporting process derives segment and business results by utilizing allocation methodologies for revenue, expense and capital. The Net Income derived for the businesses are dependent upon revenue and cost allocations using an activity-based costing model, funds transfer pricing... -

Page 47

Global Consumer and Small Business Banking 2006 (Dollars in millions) Total Deposits Card Services (1) Mortgage Home Equity ALM/Other Net interest income (2) Noninterest income Card income Service charges Mortgage banking income All other income Total noninterest income $ 21,100 13,504 5,343... -

Page 48

... to have the debit transactions processed. We added approximately 2.4 million net new retail checking accounts and 1.2 million net new retail savings accounts during 2006. These additions resulted from continued improvement in sales and service results in the Banking Center Channel, the introduction... -

Page 49

.... Pursuant to American Institute of Certified Public Accountants (AICPA) Statement of Position No. 03-3 "Accounting for Certain Loans or Debt Securities Acquired in a Transfer" (SOP 03-3) the Corporation decreased held net charge-offs for Card Services and credit card $288 million or 30 bps and... -

Page 50

...products and services to customers nationwide. Mortgage products are available to our customers through a retail network of personal bankers located in 5,747 banking centers, sales account executives in nearly 200 locations and through a sales force offering our customers direct telephone and online... -

Page 51

... product offerings and the expanding home equity market. ALM/Other ALM/Other is comprised primarily of the allocation of a portion of the Corporation's Net Interest Income from ALM activities, the residual of the funds transfer pricing allocation process associated with recording Card Services... -

Page 52

... Provision for credit losses Gains on sales of debt securities Noninterest expense Income before income taxes (1) Income tax expense Net income Shareholder value added Net interest yield (1) Return on average equity Efficiency ratio (1) Period end - total assets (2) (1) (2) $ $ 2,594 $ $ 1,346... -

Page 53

.... These increases were partially offset by declines in Net Interest Income and Gains on Sales of Debt Securities and increases in Provision for Credit Losses and Noninterest Expense. Although Global Corporate and Investment Banking experienced overall growth in Average Loans and Leases of $28... -

Page 54

... offices and special clearing arrangements. Our clients include multinationals, middle-market companies, correspondent banks, commercial real estate firms and governments. Our products and services include treasury management, trade finance, foreign exchange, short-term credit facilities and short... -

Page 55

...average equity Efficiency ratio (1) Period end - total assets (2) $ $ 2,403 $ 335 $ 196 n/m 20.66% 65.49 $3,082 2005 $ $ 948 1,340 3.29% 23.20 51.48 $137,739 302 3.20% 22.46 60.69 $34,047 574 2.93% 26.89 47.29 $105,460 (Dollars in millions) Total Private Bank Columbia Management Premier... -

Page 56

...assets which benefited from new pricing strategies including $0 Online Equity Trades which were offered beginning in the fourth quarter of 2006. Assets in custody increased $6.7 billion, or seven percent, due to market appreciation partially offset by net outflows. The Private Bank The Private Bank... -

Page 57

... driven by higher deposit spreads partially offset by lower average deposit balances. Deposit spreads increased 40 bps to 2.34 percent. Net Interest Income also benefited from higher Average Loans and Leases, mainly residential mortgages and home equity. Noninterest Income increased $60 million, or... -

Page 58

...Securities. The objective of the funds transfer pricing allocation methodology is to neutralize the businesses from changes in interest rate and foreign exchange fluctuations. Accordingly, for segment reporting purposes, the businesses received in 2005 the neutralizing benefit to Net Interest Income... -

Page 59

... additional information on credit card securitizations, see Note 9 of the Consolidated Financial Statements. Commercial Paper Qualified Special Purpose Entities To manage our capital position and diversify funding sources, we will, from time to time, sell assets to off-balance sheet entities that... -

Page 60

... are equity commitments of $2.8 billion related to obligations to further fund equity investments. As part of the MBNA merger, on January 1, 2006, the Corporation acquired $588.4 billion of unused credit card lines. Managing Risk Overview Our management governance structure enables us to manage all... -

Page 61

...' actions are in compliance with corporate policies, standards, procedures, and applicable laws and regulations. We use various methods to manage risks at the line of business levels and corporate-wide. Examples of these methods include planning and forecasting, risk committees and forums, limits... -

Page 62

... of the $5.2 billion cash payment related to the MBNA merger that was paid on January 1, 2006 combined with an increase in share repurchases. The primary sources of funding for our banking subsidiaries include customer deposits and wholesale market-based funding. Primary uses of funds for the... -

Page 63

... a larger share of mortgage production on the Corporation's balance sheet. The strength of our balance sheet is a result of rigorous financial and risk discipline. Our core deposit base, which is a low cost funding source, is often used to fund the purchase of incremental assets (primarily loans and... -

Page 64

... classifications including loans and leases, derivatives, trading account assets, assets held-for-sale, and unfunded lending commitments that include loan commitments, letters of credit and financial guarantees. For derivative positions, our credit risk is measured as the net replacement cost in the... -

Page 65

... netting agreements and cash collateral. Our consumer and commercial credit extension and review procedures take into account funded and unfunded credit exposures. For additional information on derivatives and credit extension commitments, see Notes 4 and 13 of the Consolidated Financial Statements... -

Page 66

... 03-3) of total average held credit card - domestic loans compared to 6.76 percent in 2005 primarily due to bankruptcy reform which accelerated charge-offs into 2005. This decrease in net charge-offs was partially offset by new advances on accounts for which previous loan balances were sold to the... -

Page 67

... Small Business Banking (home equity loans, student and other non-real estate secured and unsecured personal loans) and the remainder was included in Global Wealth and Investment Management (home equity loans and other non-real estate secured and unsecured personal loans) and All Other (home equity... -

Page 68

... in Net Income for 2006. Balances do not include nonperforming loans held for sale included in Other Assets of $30 million and $24 million at December 31, 2006 and 2005. Commercial Portfolio Credit Risk Management Credit risk management for the commercial portfolio begins with an assessment of... -

Page 69

...Consumer Credit Portfolio section. Net charge-off ratios are calculated as net charge-offs divided by average outstanding loans and leases during the year for each loan and lease category. Includes domestic commercial real estate loans of $35.7 billion and $35.2 billion at December 31, 2006 and 2005... -

Page 70

... of a number of relatively small credits in a variety of property types, the largest of which is residential. The increase was partially offset by improvements centered in hotels/motels and multiple use commercial properties. Table 18 presents outstanding commercial real estate loans by geographic... -

Page 71

... 19 Nonperforming Commercial Assets Activity (1) (Dollars in millions) 2006 2005 Nonperforming loans and leases Balance, January 1 Additions to nonperforming loans and leases: New nonaccrual loans and leases Advances Reductions in nonperforming loans and leases: Paydowns and payoffs Sales Returns... -

Page 72

... (Dollars in millions) Total Commercial Committed 2006 2005 Net Credit Default Protection (2) 2006 2005 2006 2005 Real estate (3) Diversified financials Retailing Government and public education Capital goods Banks Consumer services Healthcare equipment and services Individuals and trusts... -

Page 73

...2006 2005 2004 $ 53 298 74 $9,172 7,272 1,585 $ 8,059 13,616 8,481 $17,284 21,186 10,140 1.18% 1.64 0.91 (1) (2) Exposure includes cross-border claims by our foreign offices as follows: loans, accrued interest receivable, acceptances, time deposits placed, trading account assets, securities... -

Page 74

... America 2006 actions are expected to close in early 2007. Subsequent to the sale of our Brazilian operations and the closing of the Chile and Uruguay transactions, the Corporation will hold approximately seven percent of the equity of Banco Itaú through voting and non-voting shares. The increased... -

Page 75

... in 2005 for changes in minimum payment requirements were utilized to absorb associated net charge-offs. Direct/indirect consumer allowance levels increased as the Corporation discontinued new sales of receivables into the Card Services unsecured lending securitization trusts. Commercial - domestic... -

Page 76

... 26 Allowance for Credit Losses (Dollars in millions) 2006 2005 Allowance for loan and lease losses, January 1 MBNA balance, January 1, 2006 Loans and leases charged off Residential mortgage Credit card - domestic Credit card - foreign Home equity lines Direct/Indirect consumer Other consumer... -

Page 77

... process, credit risk mitigation activities and mortgage banking activities. Our traditional banking loan and deposit products are nontrading positions and are reported at amortized cost for assets or the amount owed for liabilities (historical cost). The accounting rules require a historical cost... -

Page 78

...the Net Interest Income recognized on trading positions, or the related funding charge or benefit. Trading Account Profits can be volatile and are largely driven by general market conditions and customer demand. Trading Account Profits are dependent on the volume and type of transactions, the level... -

Page 79

...daily VAR for the twelve months ended December 31, 2006 and 2005. Table 28 Trading Activities Market Risk Twelve Months Ended December 31 2006 (Dollars in millions) 2005 Low (1) Average VAR High (1) Low (1) Average VAR High (1) Foreign exchange Interest rate Credit Real estate/mortgage Equities... -

Page 80

... about balance sheet dynamics such as loan and deposit growth and pricing, changes in funding mix, and asset and liability repricing and maturity characteristics. The Balance Sheet Management group analyzes core net interest income - managed basis forecasts utilizing different rate scenarios... -

Page 81

... rate swaps of $1.3 billion, partially offset by losses from changes in the values of foreign exchange contracts of $1.2 billion, and option products of $1.0 billion. The increase in the value of foreign exchange basis swaps was due to the strengthening of most foreign currencies against the dollar... -

Page 82

...that will not be effective until their respective contractual start dates. Foreign exchange basis swaps consist of cross-currency variable interest rate swaps used separately or in conjunction with receive fixed interest rate swaps. Option products include $225.1 billion in caps and $18.2 billion in... -

Page 83

... gathered from the self-assessment process, key operational risk indicators have been developed and are used to help identify trends and issues on both a corporate and a business line level. Mortgage Banking Risk Management Interest rate lock commitments (IRLCs) on loans intended to be sold... -

Page 84

...the Allowance for Loan and Lease Losses to changes in key inputs. We believe the risk ratings and loss severities currently in use are appropriate and that the probability of a downgrade of one level of the internal risk ratings for commercial loans and leases within a short period of time is remote... -

Page 85

... publicly-traded companies at all stages of their life cycle, from start-up to buyout. These investments are made either directly in a company or held through a fund. Some of these companies may need access to additional cash to support their long-term business models. Market conditions and company... -

Page 86

... card and home equity) and commercial loans, higher domestic deposit levels and a larger ALM portfolio (primarily securities). Partially offsetting these increases was the adverse impact of spread compression due to the flattening of the yield curve, which contributed to lower Net Interest Income... -

Page 87

... other noninterest income, Trading Account Profits and Investment and Brokerage Services. Net Income was also impacted by higher Gains on Sales of Debt Securities. These increases were partially offset by an increase in Noninterest Expense and a reduced benefit from Provision for Credit Losses. The... -

Page 88

... Earning assets Time deposits placed and other short-term investments Federal funds sold and securities purchased under agreements to resell Trading account assets Debt securities (1) Loans and leases (2): Residential mortgage Credit card - domestic Credit card - foreign Home equity lines Direct... -

Page 89

...in interest income Time deposits placed and other short-term investments Federal funds sold and securities purchased under agreements to resell Trading account assets Debt securities Loans and leases: Residential mortgage Credit card - domestic Credit card - foreign Home equity lines Direct/Indirect... -

Page 90

Table III Outstanding Loans and Leases December 31 (Dollars in millions) 2006 2005 2004 2003 2002 Consumer Residential mortgage Credit card - domestic Credit card - foreign Home equity lines Direct/Indirect consumer (1) Other consumer (2) $241,181 61,195 10,999 74,888 68,224 9,218 465,705 161... -

Page 91

... real estate Commercial lease financing Commercial - foreign 110 23 n/a 29 162 $860 Total commercial Total accruing loans and leases past due 90 days or more (1) $1,455 $1,294 Balance at December 31, 2006 is related to repurchases pursuant to our servicing agreements with GNMA mortgage... -

Page 92

... Credit Losses (Dollars in millions) 2006 2005 2004 2003 2002 Allowance for loan and lease losses, January 1 FleetBoston balance, April 1, 2004 MBNA balance, January 1, 2006 Loans and leases charged off Residential mortgage Credit card - domestic Credit card - foreign Home equity lines Direct... -

Page 93

...for Credit Losses by Product Type December 31 2006 (Dollars in millions) 2005 Percent Amount Percent 2004 Amount Percent 2003 Amount Percent 2002 Amount Percent Amount Allowance for loan and lease losses Residential mortgage Credit card - domestic Credit card - foreign Home equity lines Direct... -

Page 94

... 53,756 Commercial paper At December 31 Average during year Maximum month-end balance during year Other short-term borrowings At December 31 Average during year Maximum month-end balance during year Table X Non-exchange Traded Commodity Contracts (Dollars in millions) Asset Positions Liability... -

Page 95

... Total ending equity to total ending assets Total average equity to total average assets Dividend payout Per common share data Earnings Diluted earnings Dividends paid Book value 1.20 1.18 0.56 29.52 Average balance sheet Total loans and leases Total assets Total deposits Long-term debt Common... -

Page 96

... assets Time deposits placed and other short-term investments Federal funds sold and securities purchased under agreements to resell Trading account assets Debt securities (1) Loans and leases (2): Residential mortgage Credit card - domestic Credit card - foreign Home equity lines Direct/Indirect... -

Page 97

... Earning assets Time deposits placed and other short-term investments Federal funds sold and securities purchased under agreements to resell Trading account assets Debt securities (1) Loans and leases (2): Residential mortgage Credit card - domestic Credit card - foreign Home equity lines Direct... -

Page 98

... derived from changes in an underlying index such as interest rates, foreign exchange rates or prices of securities. Derivatives utilized by the Corporation include swaps, financial futures and forward settlement contracts, and option contracts. Excess Servicing Income - For certain assets that have... -

Page 99

... Generally accepted accounting principles in the United States Office of the Comptroller of the Currency Other Comprehensive Income Qualified Special Purpose Entity Risk and Capital Committee Standby letters of credit Securities and Exchange Commission Special Purpose Entity Bank of America 2006... -

Page 100

... and the preparation of financial statements for external purposes in accordance with accounting principles generally accepted in the United States of America. The Corporation's internal control over financial reporting includes those policies and procedures that (i) pertain to the maintenance... -

Page 101

... opinion, the accompanying Consolidated Balance Sheet and the related Consolidated Statement of Income, Consolidated Statement of Changes in Shareholders' Equity and Consolidated Statement of Cash Flows present fairly, in all material respects, the financial position of Bank of America Corporation... -

Page 102

Consolidated Statement of Income Bank of America Corporation and Subsidiaries Year Ended December 31 (Dollars in millions, except per share information) 2006 2005 2004 Interest income Interest and fees on loans and leases Interest and dividends on securities Federal funds sold and securities ... -

Page 103

Consolidated Balance Sheet Bank of America Corporation and Subsidiaries December 31 (Dollars in millions) 2006 2005 Assets Cash and cash equivalents Time deposits placed and other short-term investments Federal funds sold and securities purchased under agreements to resell (includes $135,409 and... -

Page 104

..., 2003 Net income Net unrealized losses on available-for-sale debt and marketable equity securities Net unrealized gains on foreign currency translation adjustments Net losses on derivatives Cash dividends paid: Common Preferred Common stock issued under employee plans and related tax benefits Stock... -

Page 105

... Bank of America Corporation and Subsidiaries Year Ended December 31 (Dollars in millions) 2006 2005 2004 Operating activities Net income Reconciliation of net income to net cash provided by (used in) operating activities: Provision for credit losses (Gains) losses on sales of debt securities... -

Page 106

..., 2006, MBNA America Bank N.A. was renamed FIA Card Services, N.A., and on October 20, 2006, Bank of America, N.A. (USA) merged into FIA Card Services, N.A. These mergers had no impact on the Consolidated Financial Statements of the Corporation. Note 1 - Summary of Significant Accounting Principles... -

Page 107

... mortgage servicing rights, or MSRs) at fair value, with the changes in fair value recorded in the Consolidated Statement of Income. The Corporation elected to early adopt the standard and to account for consumer-related MSRs using the fair value measurement method on January 1, 2006. Commercial... -

Page 108

determined rate or price during a period or at a time in the future. Option agreements can be transacted on organized exchanges or directly between parties. The Corporation also provides credit derivatives to customers who wish to increase or decrease credit exposures. In addition, the Corporation ... -

Page 109

.... The changes in the fair value of these derivatives are recorded in Mortgage Banking Income. Investments in equity securities without readily determinable market values are recorded in Other Assets, are accounted for using the cost method and are subject to impairment testing as applicable. Equity... -

Page 110

... is reported in the Consolidated Statement of Income in the Provision for Credit Losses. Nonperforming Loans and Leases, Charge-offs, and Delinquencies In accordance with the Corporation's policies, non-bankrupt credit card loans, open-end unsecured consumer loans, and real estate secured loans are... -

Page 111

... lease term or estimated useful life for leasehold improvements. Mortgage Servicing Rights Effective January 1, 2006, the Corporation early adopted SFAS 156 and began accounting for consumer-related MSRs at fair value with changes in fair value recorded in Mortgage Banking Income, while commercial... -

Page 112

...service costs or credits, and transition assets or obligations as a component of Accumulated OCI. These amounts were previously netted against the plans' funded status in the Corporation's Consolidated Balance Sheet. These amounts will be subsequently recognized as components of net periodic benefit... -

Page 113

...is determined to be the U.S. dollar, the resulting remeasurement currency gains or losses on foreign denominated assets or liabilities are included in Net Income. Note 2 - MBNA Merger and Restructuring Activity The Corporation acquired 100 percent of the outstanding stock of MBNA on January 1, 2006... -

Page 114

... stock exchanged with MBNA shareholders was based upon the average of the closing prices of the Corporation's common stock for the period commencing two trading days before, and ending two trading days after, June 30, 2005, the date of the MBNA merger announcement. Includes purchased credit card... -

Page 115

...traded instruments conform to standard terms and are subject to policies set by the exchange involved, including margin and security deposit requirements. Management believes the credit risk associated with these types of instruments is minimal. The average fair value of Derivative Assets, less cash... -

Page 116

... used for the Corporation's ALM activities are primarily index futures providing for cash payments based upon the movements of an underlying rate index. The Corporation uses foreign currency contracts to manage the foreign exchange risk associated with certain foreign currency-denominated assets... -

Page 117

... Statement of Income for 2006 and 2005. Amount for 2006 primarily represents net investment hedges of certain foreign subsidiaries acquired in connection with the MBNA merger. Note 5 - Securities The amortized cost, gross unrealized gains and losses, and fair value of AFS debt and marketable equity... -

Page 118

...-than-temporary impairment for these securities. The Corporation had investments in securities from the Federal National Mortgage Association (Fannie Mae) and Federal Home Loan Mortgage Corporation (Freddie Mac) that exceeded 10 percent of consolidated Shareholders' Equity as of December 31, 2006... -

Page 119

... percent, or 19.1 billion shares, of the stock of China Construction Bank (CCB). These shares are accounted for at cost as they are non-transferable until the third anniversary of the initial public offering in October 2008. The Corporation also holds an option to increase its ownership interest in... -

Page 120

...and 2005. The Corporation has loan products with varying terms (e.g., interestonly mortgages, option adjustable rate mortgages, etc.) and loans with high loan-to-value ratios. Exposure to any of these loan products does not result in a significant concentration of credit risk. Terms of loan products... -

Page 121

... Consolidated Statement of Income in Mortgage Banking Income. The Corporation economically hedges these MSRs with certain derivatives such as options and interest rate swaps. Prior to Jan(Dollars in millions) uary 1, 2006, consumer-related MSRs were accounted for on a lower of cost or market basis... -

Page 122

...fee income on all mortgage loans serviced, including securitizations, was $775 million and $789 million in 2006 and 2005. For more information on MSRs, see Note 8 of the Consolidated Financial Statements. Credit Card and Other Securitizations As a result of the MBNA merger, the Corporation acquired... -

Page 123

...Consolidated Balance Sheet and increasing Net Interest Income and chargeoffs, with a related reduction in Noninterest Income. Portfolio balances, delinquency and historical loss amounts of the managed loans and leases portfolio for 2006 and 2005 are presented in the following table. Bank of America... -

Page 124

... 31, 2005 (1) Average Loans and Leases Outstanding Net Losses Net Loss Ratio (3) (Dollars in millions) Net Losses Residential mortgage Credit card - domestic Credit card - foreign Home equity lines Direct/Indirect consumer Other consumer Total consumer Commercial - domestic Commercial real estate... -

Page 125

...'s customers by facilitating their access to the commercial paper markets. The Corporation functions as administrator and provides either liquidity and letters of credit, or derivatives to the VIE. The Corporation also provides asset management and related services to or invests in other special... -

Page 126

... Holdings Corporation Other debt Advances from the Federal Home Loan Bank of Atlanta Floating, 5.49%, due 2007 Advances from the Federal Home Loan Bank of New York Fixed, with a weighted average rate of 6.07%, ranging from 4.00% to 8.29%, due 2007 to 2016 Advances from the Federal Home Loan Bank of... -

Page 127

...month London InterBank Offered Rates (LIBOR). Bank of America Corporation and Bank of America, N.A. maintain various domestic and international debt programs to offer both senior and subordinated notes. The notes may be denominated in U.S. dollars or foreign currencies. At December 31, 2006 and 2005... -

Page 128

The following table is a summary of the outstanding Trust Securities and the Notes at December 31, 2006 as originated by Bank of America Corporation and the predecessor banks. Aggregate Principal Amount of Trust Securities $ 575 900 500 375 518 1,000 1,665 530 900 1,000 863 365 500 500 450 300 450 ... -

Page 129

... to terminate or change certain terms of the credit card lines. Other Guarantees The Corporation sells products that offer book value protection primarily to plan sponsors of Employee Retirement Income Security Act of 1974 (ERISA) governed pension plans, such as 401(k) plans and 457 plans. The book... -

Page 130

...and 2005, the Corporation had not made a payment under these products, and management believes that the probability of payments under these guarantees is remote. The Corporation also has written put options on highly rated fixed income securities. Its obligation under these agreements is to buy back... -

Page 131

... Fee and Merchant Discount Anti-Trust Litigation. Motions to dismiss portions of the First Consolidated and Amended Class Action Complaint and the supplemental complaint are pending. In re Initial Public Offering Securities Beginning in 2001, Robertson Stephens, Inc. (an investment banking... -

Page 132

... provided financial services and extended credit to Parmalat and its related entities. On June 21, 2004, Extraordinary Commissioner Dr. Enrico Bondi filed with the Italian Ministry of Production Activities a plan of reorganization for the restructuring of the companies of the Parmalat group that are... -

Page 133

...LLC Litigation Trust, filed a complaint against the Corporation, BANA, BAS, BASL, Bank of America National Trust & Savings Association and BankAmerica International Limited, as well as other financial institutions and accounting firms, in the U.S. District Court for the Southern District of New York... -

Page 134

... filed a motion to extend class certification to the new allegations and claim in the second amended complaint. Refco Beginning in October 2005, BAS was named as a defendant in several putative class action lawsuits filed in the U.S. District Court for the Southern District of New York relating... -

Page 135

... were partially offset by the issuance of approximately 121.1 million shares of common stock under employee plans, which increased Shareholders' Equity by $3.9 billion, net of $127 million of deferred compensation related to restricted stock awards, and decreased diluted earnings per common share by... -

Page 136

... of Bank of America Corporation Floating Rate Non-Cumulative Preferred Stock, Series E (Series E Preferred Stock) with a par value of $0.01 per share. Ownership is held in the form of depositary shares, each representing a 1/1,000th interest in a share of Series E Preferred Stock, paying a quarterly... -

Page 137

... Note 1 of the Consolidated Financial Statements for a discussion on the calculation of earnings per common share. (Dollars in millions, except per share information; shares in thousands) 2006 2005 2004 Earnings per common share Net income Preferred stock dividends Net income available to common... -

Page 138

... deposits. Average daily reserve balances required by the FRB were $5.6 billion and $6.4 billion for 2006 and 2005. Currency and coin residing in branches and cash vaults (vault cash) are used to partially satisfy the reserve requirement. The average daily reserve balances, in excess of vault cash... -

Page 139

... of five years of service. It is the policy of the Corporation to fund not less than the minimum funding amount required by ERISA. The Pension Plan has a balance guarantee feature, applied at the time a benefit payment is made from the plan, that protects participant balances transferred and certain... -

Page 140

... of actuarial gains and losses, prior service costs or credits, and transition assets or obligations as a component of Accumulated OCI. These amounts were previously netted against the plans' funded status in the Corporation's Consolidated Balance Sheet pursuant to the provisions of SFAS 87... -

Page 141

... Health and Life Plans (1) 2006 2005 2006 2005 Change in fair value of plan assets (Primarily listed stocks, fixed income and real estate) Fair value, January 1 MBNA balance, January 1, 2006 Actual return on plan assets Company contributions (2) Plan participant contributions Benefits... -

Page 142

... as funding levels and liability characteristics change. Active and passive investment managers are employed to help enhance the risk/return profile of the assets. An additional aspect of the investment strategy used to minimize risk (part of the asset allocation plan) includes matching the equity... -

Page 143

...Equity securities for the Qualified Pension Plans include common stock of the Corporation in the amounts of $882 million (5.25 percent of total plan assets) and $798 million (6.10 percent of total plan assets) at December 31, 2006 and 2005. The Bank of America and MBNA Postretirement Health and Life... -

Page 144

...common stock when the stock options are exercised. 2006 Risk-free interest rate Dividend yield Expected volatility Weighted-average volatility Expected lives (years) n/a = not applicable Rewarding Success Plan In 2005, the Corporation introduced a broad-based cash incentive plan for associates that... -

Page 145

...to employees of predecessor companies assumed in mergers. The weighted average option price of the assumed options was $34.07 at December 31, 2006. Shareholder approval of these broad-based stock option plans was not required by applicable law or New York Stock Exchange rules. Restricted stock/unit... -

Page 146

...net deferred tax liability at December 31, 2006 and 2005 are presented in the following table. December 31 (Dollars in millions) 2006 2005 Deferred tax liabilities Equipment lease financing Intangibles Fee income Mortgage servicing rights Foreign currency State income taxes Fixed assets Loan fees... -

Page 147

... Assets such as purchased credit card, affinity, and trust relationships. Deposits The fair value for deposits with stated maturities was calculated by discounting contractual cash flows using current market rates for instruments with similar maturities. The carrying value of foreign time deposits... -

Page 148

...ALM activities, including the residual impact of funds transfer pricing allocation methodologies, amounts associated with the change in the value of derivatives used as economic hedges of interest rate and foreign exchange rate fluctuations that do not qualify for SFAS 133 hedge accounting treatment... -

Page 149

... and Net Income to the Consolidated Statement of Income, and Total Assets to the Consolidated Balance Sheet. The adjustments presented in the table below include consolidated income and expense amounts not specifically allocated to individual business segments. Year Ended December 31 (Dollars in... -

Page 150

... subsidiaries Total equity in undistributed earnings of subsidiaries Net income Net income available to common shareholders Condensed Balance Sheet December 31 (Dollars in millions) 2006 2005 Assets Cash held at bank subsidiaries Securities Receivables from subsidiaries: Bank subsidiaries Other... -

Page 151

...activities Net (purchases) sales of securities Net payments from (to) subsidiaries Other investing activities, net Net cash provided by (used in) investing activities Financing activities Net increase (decrease) in commercial paper and other short-term borrowings Proceeds from issuance of long-term... -

Page 152

...Total Assets, Total Revenue, Income Before Income Taxes and Net Income by geographic area. The Corporation identifies its geographic performance based upon the business unit structure used to manage the capital or expense deployed in the region as applicable. This requires certain judgments related... -

Page 153

... of North Carolina at Chapel Hill Chapel Hill, NC Kenneth D. Lewis Chairman, Chief Executive Ofï¬cer and President Bank of America Corporation Charlotte, NC Monica C. Lozano Publisher and Chief Executive Ofï¬cer La Opinión Los Angeles, CA Walter E. Massey President Morehouse College Atlanta, GA... -

Page 154

... concerning dividend checks, dividend reinvestment plan, electronic deposit of dividends, tax information, transferring ownership, address changes or lost or stolen stock certiï¬cates, contact Bank of America Shareholder Services at Computershare Trust Company, N.A., via our Internet access at www... -

Page 155

s Recycled Paper © 2007 Bank of America Corporation 00-04-1362B 3/2007