Bank of America 2006 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

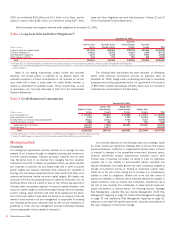

turn monitors, and independently reviews and evaluates, the plans and

measurement processes.

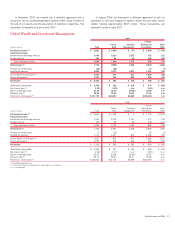

One of the key tools we use to manage strategic risk is economic

capital allocation. Through the economic capital allocation process, we

effectively manage each business unit’s ability to take on risk. Review and

approval of business plans incorporates approval of economic capital allo-

cation, and economic capital usage is monitored through financial and risk

reporting. Economic capital allocation plans for the business units are

incorporated into the Corporation’s operating plan that is approved by the

Board on an annual basis.

Liquidity Risk and Capital Management

Liquidity Risk

Liquidity is the ongoing ability to accommodate liability maturities and

deposit withdrawals, fund asset growth and business operations, and

meet contractual obligations through unconstrained access to funding at

reasonable market rates. Liquidity management involves forecasting fund-

ing requirements and maintaining sufficient capacity to meet the needs

and accommodate fluctuations in asset and liability levels due to changes

in our business operations or unanticipated events. Sources of liquidity

include deposits and other customer-based funding, and wholesale

market-based funding.

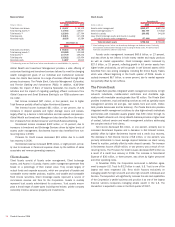

We manage liquidity at two levels. The first is the liquidity of the

parent company, which is the holding company that owns the banking and

nonbanking subsidiaries. The second is the liquidity of the banking sub-

sidiaries. The management of liquidity at both levels is essential because

the parent company and banking subsidiaries each have different funding

needs and sources, and each are subject to certain regulatory guidelines

and requirements. Through ALCO, the Finance Committee is responsible

for establishing our liquidity policy as well as approving operating and con-

tingency procedures, and monitoring liquidity on an ongoing basis. Corpo-

rate Treasury is responsible for planning and executing our funding

activities and strategy.

In order to ensure adequate liquidity through the full range of poten-

tial operating environments and market conditions, we conduct our liquid-

ity management and business activities in a manner that will preserve and

enhance funding stability, flexibility, and diversity. Key components of this

operating strategy include a strong focus on customer-based funding,

maintaining direct relationships with wholesale market funding providers,

and maintaining the ability to liquefy certain assets when, and if, require-

ments warrant.

We develop and maintain contingency funding plans for both the

parent company and bank liquidity positions. These plans evaluate our

liquidity position under various operating circumstances and allow us to

ensure that we would be able to operate through a period of stress when

access to normal sources of funding is constrained. The plans project

funding requirements during a potential period of stress, specify and quan-

tify sources of liquidity, outline actions and procedures for effectively

managing through the problem period, and define roles and

responsibilities. They are reviewed and approved annually by ALCO.

Our borrowing costs and ability to raise funds are directly impacted by

our credit ratings. The credit ratings of Bank of America Corporation and

Bank of America, N.A. are reflected in the table below.

Under normal business conditions, primary sources of funding for the

parent company include dividends received from its banking and non-

banking subsidiaries, and proceeds from the issuance of senior and sub-

ordinated debt, as well as commercial paper and equity. Primary uses of

funds for the parent company include repayment of maturing debt and

commercial paper, share repurchases, dividends paid to shareholders,

and subsidiary funding through capital or debt.

The parent company maintains a cushion of excess liquidity that

would be sufficient to fully fund holding company and nonbank affiliate

operations for an extended period during which funding from normal sour-

ces is disrupted. The primary measure used to assess the parent compa-

ny’s liquidity is the “Time to Required Funding” during such a period of

liquidity disruption. This measure assumes that the parent company is

unable to generate funds from debt or equity issuance, receives no divi-

dend income from subsidiaries, and no longer pays dividends to share-

holders while continuing to meet nondiscretionary uses needed to

maintain bank operations and repayment of contractual principal and

interest payments owed by the parent company and affiliated companies.

Under this scenario, the amount of time the parent company and its non-

bank subsidiaries can operate and meet all obligations before the current

liquid assets are exhausted is considered the “Time to Required Funding.”

ALCO approves the target range set for this metric, in months, and mon-

itors adherence to the target. Maintaining excess parent company cash

ensures that “Time to Required Funding” remains in the target range of 21

to 27 months and is the primary driver of the timing and amount of the

Corporation’s debt issuances. As of December 31, 2006 “Time to

Required Funding” was 24 months compared to 29 months at

December 31, 2005. The reduction reflects the funding in 2005 in antici-

pation of the $5.2 billion cash payment related to the MBNA merger that

was paid on January 1, 2006 combined with an increase in share

repurchases.

The primary sources of funding for our banking subsidiaries include

customer deposits and wholesale market–based funding. Primary uses of

funds for the banking subsidiaries include growth in the core asset portfo-

lios, including loan demand, and in the ALM portfolio. We use the ALM

portfolio primarily to manage interest rate risk and liquidity risk.

One ratio that can be used to monitor the stability of funding composi-

tion is the “loan to domestic deposit” ratio. This ratio reflects the percent

of Loans and Leases that are funded by domestic core deposits, a rela-

tively stable funding source. A ratio below 100 percent indicates that our

loan portfolio is completely funded by domestic core deposits. The ratio

was 118 percent at December 31, 2006 compared to 102 percent at

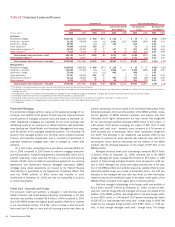

Table 10 Credit Ratings

December 31, 2006

Bank of America Corporation Bank of America, N.A.

Senior

Debt

Subordinated

Debt

Commercial

Paper

Short-term

Borrowings

Long-term

Debt

Moody’s

Aa2 Aa3 P-1 P-1 Aa1

Standard & Poor’s

(1)

AA- A+ A-1+ A-1+ AA

Fitch, Inc.

(2)

AA- A+ F1+ F1+ AA-

(1) On February 14, 2007, Standard & Poor’s Rating Services raised their ratings on Bank of America Corporation’s Senior Debt to AA and Subordinated Debt to AA- while Bank of America, N. A.’s Long-term Debt rating was raised

to AA+.

(2) On February 15, 2007, Fitch, Inc. raised their ratings on Bank of America Corporation’s Senior Debt to AA and Subordinated Debt to AA- while Bank of America, N. A.’s Long-term Debt rating was raised to AA.

60

Bank of America 2006