Bank of America 2006 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

The normalization of credit costs has long been anticipated.

Credit costs have remained historically low across most seg-

ments of the economy during the recent years of economic

expansion. As net charge-offs and provision expense normalize,

bank earnings will be pressured.

We believe we are in a good position to weather any cred-

it issues we currently see on the horizon. The breadth of our

franchise across geographies, market segments, industries

and asset classes makes our credit portfolio inherently diverse

and granular. Our ability to distribute credit risk through the

securitization of various asset classes adds further stabil-

ity. And as our risk managers analyze information about our

customers in ever more sophisticated ways, we can grow our

portfolio without significantly increasing our risk profile. In

fact, in some parts of our business we are actually saying

“yes” to more customers while at the same time improving the

average quality of our loans.

Operating leverage is perhaps our most important answer

to both the yield curve and credit costs. We have consistently

demonstrated our ability to manage expenses and produce

positive operating leverage — the difference between the rate

of revenue growth and the rate of expense growth. This per-

formance enables us to invest in our businesses even when

revenue is under pressure.

The company we’re building. At the beginning of this letter

I described our vision for Bank of America. Investors tend to

ask tough questions about our strategy that deserve answers:

First: Is Bank of America too big to grow at attractive

rates? Our answer: Absolutely not.

While Bank of America is large in the aggregate, we com-

pete in markets — defined by geography, product or market

segment — in which our current share of the market is much

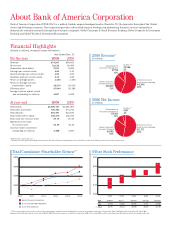

This strong financial performance has enabled us to

continue our record of returning capital to shareholders.

2006 was our 29th consecutive year of raising our quarterly

dividend, which increased by 12 percent to $0.56. Over that

time, our dividend has increased at a compound annual growth

rate of 13 percent. We also returned $9.5 billion to shareholders

in 2006 by repurchasing shares.

Last year’s financial results were gratifying, given external

headwinds our industry faced in 2006 in the form of a flat-to-

inverted yield curve and rising credit costs, which we will most

likely continue to face in 2007.

The yield curve continues to be flat to inverted. The curve

represents the spread between short- and long-term interest

rates and is an indicator of the opportunity that banks have to

generate net interest income.

We believe we are better positioned than many of our com-

petitors in this environment. Our revenue mix is now more

than 50 percent fee income, and this change in mix has allowed

us to continue to operate within our long-term target of 6 to

9 percent annual revenue growth even as net interest income

growth has been reduced to low single digits.

We have consistently

demonstrated our ability to manage

expenses and produce

positive operating leverage.

4 Bank of America 2006