Bank of America 2006 Annual Report Download - page 123

Download and view the complete annual report

Please find page 123 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

The sensitivities in the preceding table are hypothetical and should

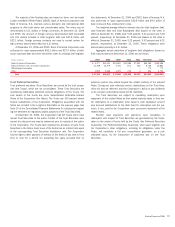

be used with caution. As the amounts indicate, changes in fair value

based on variations in assumptions generally cannot be extrapolated

because the relationship of the change in assumption to the change in fair

value may not be linear. Also, the effect of a variation in a particular

assumption on the fair value of an interest that continues to be held by

the Corporation is calculated without changing any other assumption. In

reality, changes in one factor may result in changes in another, which

might magnify or counteract the sensitivities. Additionally, the Corporation

has the ability to hedge interest rate risk associated with retained residual

positions. The above sensitivities do not reflect any hedge strategies that

may be undertaken to mitigate such risk.

Static pool net credit losses are considered in determining the value

of the retained interests of the consumer finance securitization. Static

pool net credit losses include actual losses incurred plus projected credit

losses divided by the original balance of each securitization pool. For

consumer finance securitizations entered into in 2006, weighted average

static pool net credit losses were 5.00 percent for the year ended

December 31, 2006. For consumer finance securitizations entered into in

2001, weighted average static pool net credit losses were 5.29 percent

for the year ended December 31, 2006, and 5.50 percent for the year

ended December 31, 2005.

Principal proceeds from collections reinvested in revolving credit card

securitizations were $163.4 billion and $4.5 billion in 2006 and 2005.

Contractual credit card servicing fee income totaled $1.9 billion and $97

million in 2006 and 2005. Other cash flows received on retained inter-

ests, such as cash flow from interest-only strips, were $6.7 billion and

$183 million in 2006 and 2005, for credit card securitizations. Proceeds

from collections reinvested in revolving commercial loan securitizations

were $4.6 billion and $8.7 billion in 2006 and 2005. Servicing fees and

other cash flows received on retained interests, such as cash flows from

interest-only strips, were $2 million and $15 million in 2006, and $3 mil-

lion and $34 million in 2005 for commercial loan securitizations.

The Corporation also reviews its loans and leases portfolio on a

managed basis. Managed loans and leases are defined as on-balance

sheet Loans and Leases as well as those loans in revolving securitizations

and other securitizations where servicing is retained that are undertaken

for corporate management purposes, which include credit card, commer-

cial loans, automobile and certain mortgage securitizations. Managed

loans and leases exclude originate-to-distribute loans and other loans in

securitizations where the Corporation has not retained servicing. New

advances on accounts for which previous loan balances were sold to the

securitization trusts will be recorded on the Corporation’s Consolidated

Balance Sheet after the revolving period of the securitization, which has

the effect of increasing Loans and Leases on the Corporation’s Con-

solidated Balance Sheet and increasing Net Interest Income and charge-

offs, with a related reduction in Noninterest Income.

Portfolio balances, delinquency and historical loss amounts of the

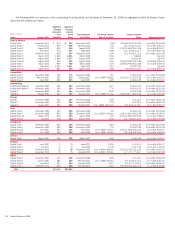

managed loans and leases portfolio for 2006 and 2005 are presented in

the following table.

Bank of America 2006

121