Bank of America 2006 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

December 31, 2005. The increase was primarily attributable to the addi-

tion of MBNA, organic growth in the loan and lease portfolio, and a deci-

sion to retain a larger share of mortgage production on the Corporation’s

balance sheet.

The strength of our balance sheet is a result of rigorous financial and

risk discipline. Our core deposit base, which is a low cost funding source,

is often used to fund the purchase of incremental assets (primarily loans

and securities), the composition of which impacts our loan to deposit

ratio. Mortgage-backed securities and mortgage loans have prepayment

risk which must be managed. Repricing of deposits is a key variable in this

process. The capital generated in excess of capital adequacy targets and

to support business growth, is available for the payment of dividends and

share repurchases.

ALCO determines prudent parameters for wholesale market-based

borrowing and regularly reviews the funding plan for the bank subsidiaries

to ensure compliance with these parameters. The contingency funding

plan for the banking subsidiaries evaluates liquidity over a 12-month

period in a variety of business environment scenarios assuming different

levels of earnings performance and credit ratings as well as public and

investor relations factors. Funding exposure related to our role as liquidity

provider to certain off-balance sheet financing entities is also measured

under a stress scenario. In this analysis, ratings are downgraded such that

the off-balance sheet financing entities are not able to issue commercial

paper and backup facilities that we provide are drawn upon. In addition,

potential draws on credit facilities to issuers with ratings below a certain

level are analyzed to assess potential funding exposure.

We originate loans for retention on our balance sheet and for dis-

tribution. As part of our “originate to distribute” strategy, commercial loan

originations are distributed through syndication structures, and residential

mortgages originated by Mortgage and Home Equity are frequently dis-

tributed in the secondary market. In connection with our balance sheet

management activities, we may retain mortgage loans originated as well

as purchase and sell loans based on our assessment of market

conditions.

Regulatory Capital

At December 31, 2006, the Corporation operated its banking activities

primarily under two charters: Bank of America, N.A. and FIA Card Services,

N.A. (the surviving entity of the MBNA America Bank N.A. and the Bank of

America, N.A. (USA) merger). As a regulated financial services company,

we are governed by certain regulatory capital requirements. At

December 31, 2006, the Corporation, Bank of America, N.A. and FIA Card

Services, N.A. were classified as “well-capitalized” for regulatory purposes,

the highest classification. At December 31, 2005, the Corporation, Bank

of America, N.A. and Bank of America, N.A. (USA) were also classified as

“well-capitalized” for regulatory purposes. There have been no conditions

or events since December 31, 2006 that management believes have

changed the Corporation’s, Bank of America, N.A.’s and FIA Card Services,

N.A.’s capital classifications.

Certain corporate sponsored trust companies which issue trust pre-

ferred securities (Trust Securities) are deconsolidated under FIN 46R. As a

result, the Trust Securities are not included on our Consolidated Balance

Sheets. On March 1, 2005, the FRB issued Risk-Based Capital Standards:

Trust Preferred Securities and the Definition of Capital (the Final Rule)

which allows Trust Securities to continue to qualify as Tier 1 Capital with

revised quantitative limits that would be effective after a five-year tran-

sition period. As a result, we continue to include Trust Securities in Tier 1

Capital.

The Final Rule limits restricted core capital elements to 15 percent

for internationally active bank holding companies. In addition, the FRB

revised the qualitative standards for capital instruments included in regu-

latory capital. Internationally active bank holding companies are those with

consolidated assets greater than $250 billion or on-balance sheet

exposure greater than $10 billion. At December 31, 2006, our restricted

core capital elements comprised 17.3 percent of total core capital ele-

ments. We expect to be fully compliant with the revised limits prior to the

implementation date of March 31, 2009.

Table 11 reconciles the Corporation’s Total Shareholders’ Equity to

Tier 1 and Total Capital as defined by the regulations issued by the FRB,

the FDIC, and the OCC at December 31, 2006 and 2005.

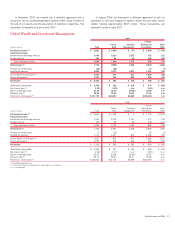

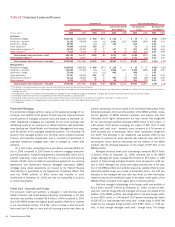

Table 11 Reconciliation of Tier 1 and Total Capital

December 31

(Dollars in millions) 2006 2005

Tier 1 Capital

Total Shareholders’ equity

$135,272

$101,533

Goodwill

(65,662)

(45,354)

Nonqualifying intangible assets

(1)

(3,782)

(2,642)

Effect of net unrealized losses on AFS debt and marketable equity securities and net losses on derivatives recorded in

Accumulated OCI, net of tax

6,430

7,316

Accounting change for implementation of FASB Statement No. 158

1,428

–

Trust securities

(2)

15,942

12,446

Other

1,436

1,076

Tier 1 Capital

91,064

74,375

Long-term debt qualifying as Tier 2 Capital

24,546

16,848

Allowance for loan and lease losses

9,016

8,045

Reserve for unfunded lending commitments

397

395

Other

203

238

Total Capital

$125,226

$ 99,901

(1) Nonqualifying intangible assets of the Corporation are comprised of certain core deposit intangibles, affinity relationships, and other intangibles.

(2) Trust Securities are net of unamortized discounts.

Bank of America 2006

61