Bank of America 2006 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

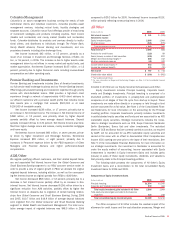

Balance Sheet

Average Balance

(Dollars in millions) 2006 2005

Total loans and leases

$192,072

$144,027

Total earning assets

(1)

328,528

298,904

Total assets

(1)

390,257

326,243

Total deposits

330,072

306,098

Allocated equity

63,121

29,581

December 31

2006 2005

Total loans and leases

$206,040

$151,657

Total earning assets

(1)

319,552

302,619

Total assets

(1)

382,392

331,259

Total deposits

327,236

306,101

Allocated equity

60,373

36,861

(1) Total earning assets and Total Assets include asset allocations to match liabilities (i.e., deposits).

The strategy of Global Consumer and Small Business Banking is to attract,

retain and deepen customer relationships. We achieve this strategy

through our ability to offer a wide range of products and services through a

franchise that stretches coast to coast through 30 states and the District

of Columbia. With the recent merger with MBNA, we also provide credit

card products to customers in Canada, Ireland, Spain and the United

Kingdom. In the U.S., we serve more than 55 million consumer and small

business relationships utilizing our network of 5,747 banking centers,

17,079 domestic branded ATMs, and telephone and Internet channels.

Within Global Consumer and Small Business Banking, there are four pri-

mary businesses: Deposits,Card Services,Mortgage and Home Equity.In

addition, ALM/Other includes the results of ALM activities and other

consumer-related businesses (e.g., insurance).

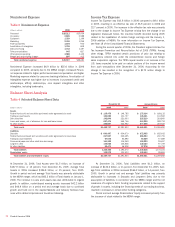

Net Income increased $4.2 billion, or 59 percent, to $11.2 billion

and Net Interest Income increased $4.2 billion, or 25 percent in 2006

compared to 2005. These increases were primarily due to the MBNA

merger and organic growth which increased Average Loans and Leases.

Noninterest Income increased $9.2 billion, or 80 percent, mainly due

to increases of $8.4 billion in Card Income, $534 million in all other

income and $347 million in Service Charges. Card Income was higher

mainly due to increases in excess servicing income, cash advance fees,

interchange income and late fees due primarily to the impact of the MBNA

merger. All other income increased primarily as a result of the MBNA

merger. Service Charges increased due to new account growth and

increased usage.

The Provision for Credit Losses increased $929 million, or 22 per-

cent, to $5.2 billion in 2006 compared to 2005 primarily resulting from a

$728 million increase in Card Services mainly driven by the MBNA merger.

For further discussion of this increase in the Provision for Credit Losses

related to Card Services, see the Card Services discussion.

Noninterest Expense increased $5.7 billion, or 43 percent, in 2006

compared to 2005. The primary driver of the increase was the MBNA

merger, which increased most expense items including Personnel, Market-

ing and Amortization of Intangibles. Amortization of Intangibles expense

was higher due to increases in purchased credit card relationships, affinity

relationships, core deposit intangibles and other intangibles, including

trademarks related to the MBNA merger.

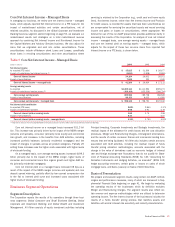

Deposits

Deposits provides a comprehensive range of products to consumers and

small businesses. Our products include traditional savings accounts,

money market savings accounts, CDs and IRAs, and regular and interest-

checking accounts. Debit card results are also included in Deposits.

Deposit products provide a relatively stable source of funding and

liquidity. We earn net interest spread revenues from investing this liquidity

in earning assets through client facing lending activity and our ALM activ-

ities. The revenue is attributed to the deposit products using our funds

transfer pricing process which takes into account the interest rates and

maturity characteristics of the deposits. Deposits also generate various

account fees such as non-sufficient fund fees, overdraft charges and

account service fees while debit cards generate interchange fees. Inter-

change fees are volume based and paid by merchants to have the debit

transactions processed.

We added approximately 2.4 million net new retail checking accounts

and 1.2 million net new retail savings accounts during 2006. These addi-

tions resulted from continued improvement in sales and service results in

the Banking Center Channel, the introduction of products such as Keep

the Change

TM

as well as eCommerce accessibility and customer referrals.

The Corporation migrates qualifying affluent customers, and their

related deposit balances and associated Net Interest Income from the

Global Consumer and Small Business Banking segment to Global Wealth

and Investment Management.

Net Income increased $496 million, or 11 percent, in 2006 com-

pared to 2005. The increase in Net Income was driven by an increase in

Total Revenue of $1.9 billion, or 13 percent compared to 2005. Driving

this growth was an increase of $1.2 billion, or 14 percent, in Net Interest

Income resulting from higher average deposit levels and an increase in

deposit spreads. Average deposits increased $24.0 billion, or eight per-

cent, compared to 2005, primarily due to the MBNA merger. Deposit

spreads increased 17 bps to 3.00 percent, compared to 2005 as we

effectively managed pricing in a rising interest rate environment. The

increase in deposits was partially offset by the migration of deposit balan-

ces to Global Wealth and Investment Management. Noninterest Income

increased $698 million, or 11 percent, driven by higher debit card inter-

change income and higher Service Charges. The increase in debit card

interchange income was primarily due to a higher number of active debit

cards, increased usage, and continued improvements in penetration and

activation rates. Service Charges were higher due to increased

non-sufficient funds fees and overdraft charges, account service charges

and ATM fees resulting from new account growth and increased usage.

Total Noninterest Expense increased $974 million, or 12 percent, in

2006 compared to 2005, primarily driven by costs associated with

increased account volume.

Card Services

Card Services, which excludes the results of debit cards (included in

Deposits), provides a broad offering of products, including U.S. Consumer

and Business Card, Unsecured Lending, Merchant Services and Interna-

tional Card Businesses. As a result of the MBNA merger, we offer a variety

of co-branded and affinity credit card products and have become the lead-

ing issuer of credit cards through endorsed marketing. Prior to the merger

with MBNA, Card Services included U.S. Consumer Card, U.S. Business

Card, and Merchant Services.

We present our Card Services business on both a held and managed

basis (a non-GAAP measure). The performance of the managed portfolio is

important to understanding Card Services’ results as it demonstrates the

results of the entire portfolio serviced by the business, as the receivables

that have been securitized are subject to the same underwriting standards

and ongoing monitoring as the held loans. For assets that have been

securitized, interest income, fee revenue and recoveries in excess of

interest paid to the investors, gross credit losses and other trust

expenses related to the securitized receivables are all reclassified into

46

Bank of America 2006