Bank of America 2006 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

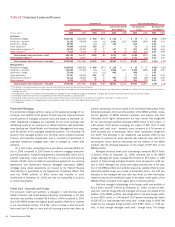

At December 31, 2006 and 2005, we had net notional credit default

protection purchased in our credit derivatives portfolio of $8.3 billion and

$14.7 billion. The net cost of credit default protection, including

mark-to-market impacts, resulted in net losses of $241 million in 2006

compared to net gains of $49 million in 2005. Losses in 2006 primarily

reflected the impact of credit spreads tightening across most of our hedge

positions. The average Value-at-Risk (VAR) for these credit derivative

hedges was $54 million and $69 million for the twelve months ended

December 31, 2006 and 2005. The decrease in VAR was driven by a

decrease in the average amount of credit protection outstanding during the

period. There is a diversification effect between the credit derivative

hedges and the market-based trading portfolio such that their combined

average VAR was $57 million and $62 million for the twelve months ended

December 31, 2006 and 2005. Refer to the discussion on page 76 for a

description of our VAR calculation for the market-based trading portfolio.

Table 20 Commercial Credit Exposure and Net Credit Default Protection by Industry (1)

December 31

Commercial Utilized

Total Commercial

Committed

Net Credit Default

Protection

(2)

(Dollars in millions) 2006 2005 2006 2005 2006 2005

Real estate (3)

$ 49,208

$ 47,580

$ 73,493

$ 70,373

$ (704)

$ (1,305)

Diversified financials

24,802

24,975

67,027

64,073

(121)

(250)

Retailing

27,226

25,189

44,064

41,967

(581)

(1,134)

Government and public education

22,495

19,041

39,254

33,350

(25)

–

Capital goods

16,804

15,337

37,337

33,004

(402)

(741)

Banks

26,405

21,755

36,735

30,811

(409)

(315)

Consumer services

19,108

17,481

32,651

29,495

(433)

(788)

Healthcare equipment and services

15,787

13,455

31,095

25,494

(249)

(709)

Individuals and trusts

18,792

16,754

29,167

24,348

3

(30)

Materials

15,882

16,754

28,693

28,893

(630)

(1,119)

Commercial services and supplies

15,204

13,038

23,512

21,152

(372)

(472)

Food, beverage and tobacco

11,341

11,194

21,081

20,590

(319)

(580)

Media

8,659

6,701

19,056

15,250

(871)

(1,790)

Energy

9,350

9,061

18,405

17,099

(236)

(589)

Utilities

4,951

5,507

17,221

15,182

(362)

(899)

Transportation

11,451

11,297

17,189

16,980

(219)

(323)

Insurance

6,573

4,745

14,121

13,868

(446)

(1,493)

Religious and social organizations

7,840

7,426

10,507

10,022

–

–

Consumer durables and apparel

4,820

5,142

9,117

9,318

(170)

(475)

Technology hardware and equipment

3,279

3,116

8,046

7,171

(38)

(402)

Telecommunication services

3,513

3,520

7,929

9,193

(1,104)

(1,205)

Pharmaceuticals and biotechnology

2,530

1,675

6,289

4,906

(181)

(470)

Software and services

2,757

2,573

6,206

5,708

(126)

(299)

Automobiles and components

1,529

1,602

5,098

5,878

(483)

(679)

Food and staples retailing

2,153

2,258

4,222

4,241

(116)

(324)

Household and personal products

720

536

2,205

1,669

50

75

Semiconductors and semiconductor equipment

802

536

1,364

1,119

(18)

(54)

Other

6,396

2,503

6,825

2,926

302

(4)

1,677

(4)

Total

$340,377

$310,751

$617,909

$564,080

$(8,260)

$(14,693)

(1) December 31, 2005 industry balances have been reclassified to reflect the realignment of industry codes utilizing Standard & Poor’s industry classifications and internal industry management.

(2) Net notional credit default protection purchased is shown as negative amounts and the net notional credit protection sold is shown as positive amounts.

(3) Industries are viewed from a variety of perspectives to best isolate the perceived risks. For purposes of this table, the real estate industry is defined based upon the borrowers’ or counterparties’ primary business activity using

operating cash flow and primary source of repayment as key factors.

(4) Represents net credit default swaps index positions, including tranched index exposure, which were principally investment grade. Indices are comprised of corporate credit derivatives that trade as an aggregate index value.

Generally, they are grouped into portfolios based on specific ratings of credit quality or global geographic location. As of December 31, 2006 and 2005, credit default swap index positions were sold to reflect our view of the

credit markets.

Tables 21 and 22 present the maturity profiles and the credit

exposure debt ratings of the net credit default protection portfolio at

December 31, 2006 and 2005.

Table 21 Net Credit Default Protection by Maturity

Profile

December 31

2006 2005

Less than or equal to one year

7%

–%

Greater than one year and less than or equal to five years

46

65

Greater than five years

47

35

Total

100%

100%

Table 22 Net Credit Default Protection by Credit

Exposure Debt Rating (1)

(Dollars in millions) December 31, 2006 December 31, 2005

Ratings Net Notional Percent Net Notional Percent

AAA

$ (23)

0.3% $ (22) 0.2%

AA

(237)

2.9 (523) 3.6

A

(2,598)

31.5 (4,861) 33.1

BBB

(3,968)

48.0 (8,572) 58.2

BB

(1,341)

16.2 (1,792) 12.2

B

(334)

4.0 (424) 2.9

CCC and below

(50)

0.6 (149) 1.0

NR

(2)

291

(3.5) 1,650 (11.2)

Total

$(8,260)

100.0% $(14,693) 100.0%

(1) In order to mitigate the cost of purchasing credit protection, credit exposure can be added by selling

credit protection. The distribution of debt rating for net notional credit default protection purchased is

shown as negative amounts and the net notional credit protection sold is shown as positive amounts.

(2) In addition to unrated names, “NR” includes $302 million and $1.7 billion in net credit default swaps

index positions at December 31, 2006 and 2005. While index positions are principally investment grade,

credit default swaps indices include names in and across each of the ratings categories.

70

Bank of America 2006