Bank of America 2006 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

In 2006 and 2005, the Corporation purchased $17.4 billion and

$19.6 billion of mortgage-backed securities from third parties and

resecuritized them. Net gains, which include Net Interest Income earned

during the holding period, totaled $25 million and $13 million. The Corpo-

ration did not retain any of the securities issued in these transactions.

In 2006 and 2005, the Corporation also purchased an additional

$4.9 billion and $7.2 billion of mortgage loans from third parties and

securitized them. In 2006, the Corporation retained residual interests in

these transactions which totaled $224 million at December 31, 2006 and

are classified in Trading Account Assets, with changes in fair value

recorded in earnings. These residual interests are included in the sensi-

tivity table below which sets forth the sensitivity of the fair value of

residual interests to changes in key assumptions. In 2005, the Corpo-

ration resecuritized the residual interests and did not retain a significant

interest in the securitization trusts. The Corporation reported $16 million

and $4 million in gains on these transactions in 2006 and 2005.

The Corporation has retained MSRs from the sale or securitization of

mortgage loans. Servicing fee and ancillary fee income on all mortgage

loans serviced, including securitizations, was $775 million and $789 mil-

lion in 2006 and 2005. For more information on MSRs, see Note 8 of the

Consolidated Financial Statements.

Credit Card and Other Securitizations

As a result of the MBNA merger, the Corporation acquired interests in

credit card, other consumer, and commercial loan securitization vehicles.

These acquired interests include interest-only strips, subordinated tranch-

es, cash reserve accounts, and subordinated interests in accrued interest

and fees on the securitized receivables. During 2006, the Corporation

securitized $23.7 billion of credit card receivables resulting in $104 mil-

lion in gains (net of securitization transaction costs of $28 million) which

was recorded in Card Income. Aggregate debt securities outstanding for

the MBNA credit card securitization trusts as of December 31, 2006 and

January 1, 2006, were $96.0 billion and $81.6 billion. As of

December 31, 2006 and January 1, 2006, the aggregate debt securities

outstanding for the Corporation’s credit card securitization trusts, including

MBNA, were $96.8 billion and $83.8 billion. The other consumer and

commercial loan securitization vehicles acquired with MBNA were not

material to the Corporation.

The Corporation also securitized $3.3 billion and $3.8 billion of

automobile loans and recorded losses of $6 million and $17 million in

2006 and 2005. At December 31, 2006 and 2005, aggregate debt secu-

rities outstanding for the Corporation’s automobile securitization vehicles

were $5.2 billion and $4.0 billion, and the Corporation held residual inter-

ests which totaled $130 million and $93 million.

At December 31, 2006 and 2005, the Corporation held investment

grade securities issued by its securitization vehicles of $3.5 billion (none

of which were issued in 2006) and $4.4 billion (including $2.6 billion

issued in 2005), which are valued using quoted market prices, in the AFS

securities portfolio. At December 31, 2006 and 2005, there were no

recognized servicing assets or liabilities associated with any of these

securitization transactions.

The Corporation has provided protection on a subset of one

consumer finance securitization in the form of a guarantee with a max-

imum payment of $220 million that will only be paid if over-collateralization

is not sufficient to absorb losses and certain other conditions are met.

The Corporation projects no payments will be due over the remaining life of

the contract, which is less than one year.

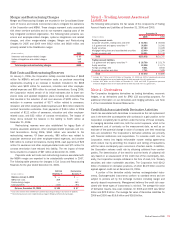

Key economic assumptions used in measuring the fair value of cer-

tain residual interests that continue to be held by the Corporation

(included in Other Assets) in securitizations and the sensitivity of the cur-

rent fair value of residual cash flows to changes in those assumptions are

disclosed in the following table.

Credit Card Consumer Finance

(1)

(Dollars in millions) 2006 2005 2006 2005

Carrying amount of residual interests (2)

$ 2,929

$ 203

$ 811

$ 290

Balance of unamortized securitized loans

98,295

2,237

6,153

2,667

Weighted average life to call or maturity (in years)

0.3

0.5

0.3-2.7

0.8

Revolving structures – monthly payment rate

11.2 - 19.8%

12.1%

Amortizing structures – annual constant prepayment rate:

Fixed rate loans

20.0 - 25.9%

26.3 - 28.9%

Adjustable rate loans

32.8 - 37.1

37.6

Impact on fair value of 10% favorable change

$43

$2

$7

$8

Impact on fair value of 25% favorable change

133

3

12

17

Impact on fair value of 10% adverse change

(38)

(2)

(15)

(16)

Impact on fair value of 25% adverse change

(82)

(3)

(23)

(39)

Expected credit losses (3)

3.8 - 5.8%

4.0 - 4.3%

4.4 - 5.9%

3.9 - 5.6%

Impact on fair value of 10% favorable change

$86

$3

$16

$7

Impact on fair value of 25% favorable change

218

8

42

18

Impact on fair value of 10% adverse change

(85)

(3)

(15)

(7)

Impact on fair value of 25% adverse change

(211)

(8)

(36)

(18)

Residual cash flows discount rate (annual rate)

12.5%

12.0%

16.0 - 30.0%

30.0%

Impact on fair value of 100 bps favorable change

$12

$–

$5

$5

Impact on fair value of 200 bps favorable change

17

–

11

11

Impact on fair value of 100 bps adverse change

(14)

–

(5)

(5)

Impact on fair value of 200 bps adverse change

(27)

–

(10)

(10)

(1) Consumer finance includes mortgage loans purchased and securitized in 2006 and originated consumer finance loans that were securitized in 2001, all of which are serviced by third parties.

(2) Residual interests include interest-only strips, subordinated tranches, subordinated interests in accrued interest and fees on the securitized receivables and cash reserve accounts which are carried at fair value or amounts

that approximate fair value. Residual interests in purchased mortgage loans totaling $224 million at December 31, 2006 are classified in Trading Account Assets. Other residual interests are classified in Other Assets.

(3) Annual rates of expected credit losses are presented for credit card securitizations. Cumulative lifetime rates of expected credit losses (incurred plus projected) are presented for consumer finance securitizations.

120

Bank of America 2006